Hello folks, and welcome to the annual review of the dividend growth companies from my watchlist! I have been busy with other projects, which is why I haven’t posted updates on when I add positions to my portfolio, but the method hasn’t changed. I continue to use the methods documented in previous posts to determine valuation and I continue to add the quality companies on my watchlist when valuation re-appears.

You will notice that many of the companies that I decided to no longer partner with continue to have good fundamentals. The reasoning was about concentrating the portfolio on companies that have better predictable earnings / cash flow history and growth, since I have been investing in other assets when it comes to volatility and added risks.

For this year, on the Canadian portfolio, I decided to sell 4 companies (besides MIC.TO, which was acquired by Brookfields and had the common shares delisted as it issued Sagen’s preferred shares). On the US portfolio, I decided to sell 1 company. No companies were added for this year.

Canadian Portfolio:

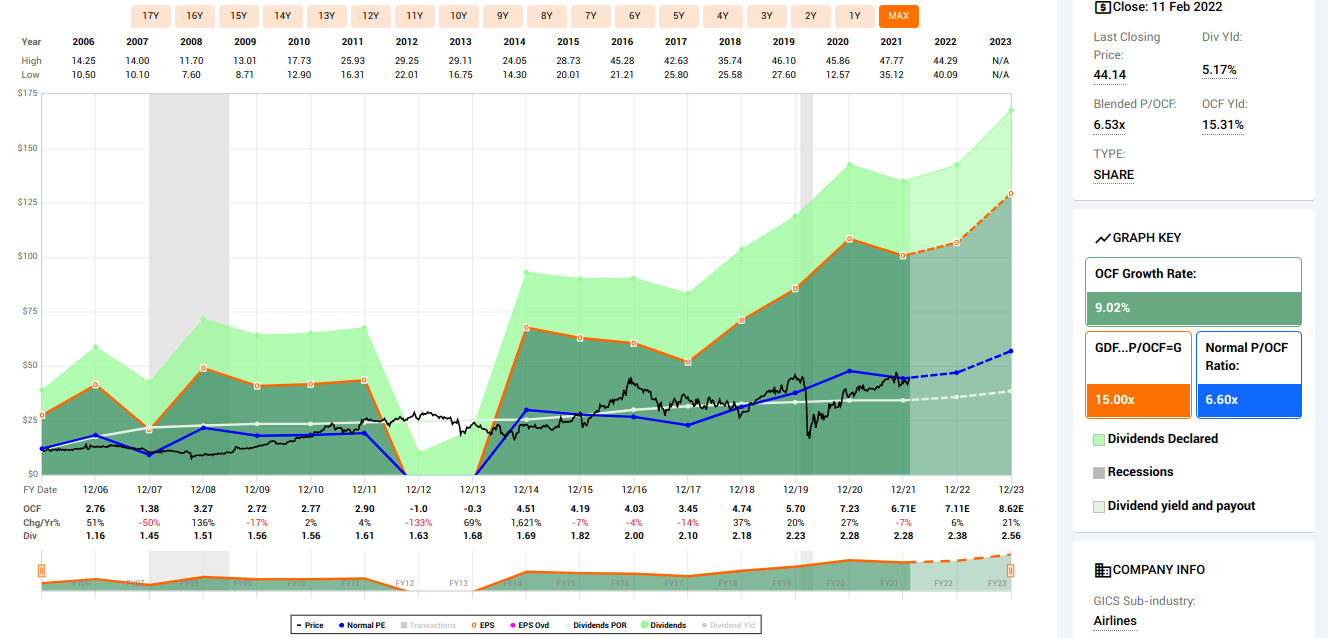

Sold: Airboss of America Corp (BOS.TO).

I am reducing my risks in equities to be exposed in other assets, so I will lock my profits here and deploy funds on other companies. Nothing wrong with BOS, earnings are estimated to drop a bit in the next short term, after the massive growth they had recently. Earnings are too cyclical given their sector exposure, so dividend growth is not always consistent. I will deploy funds to other companies that are better predictable to continue growing dividends.

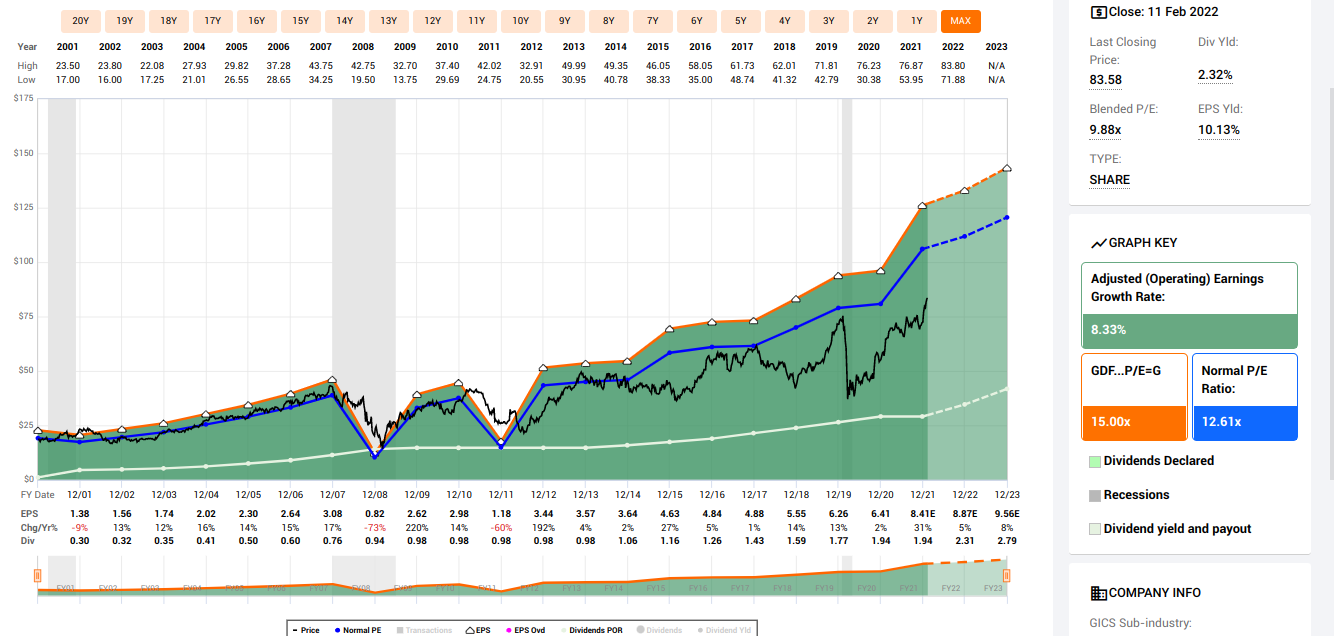

Sold: CAE Inc (CAE.TO)

They suspended dividends when the pandemic started and they have been overvalued according to the metrics that they typically trade on. I will also lock my profits here and deploy funds on other companies. I am confident that CAE will recover and eventually reinstate dividends, but I would rather have my funds deployed with other companies. As the years go by, dividend investing becomes more about reliability of growth of the income, so I will trim companies that haven’t been able to endure that consistency in difficult times.

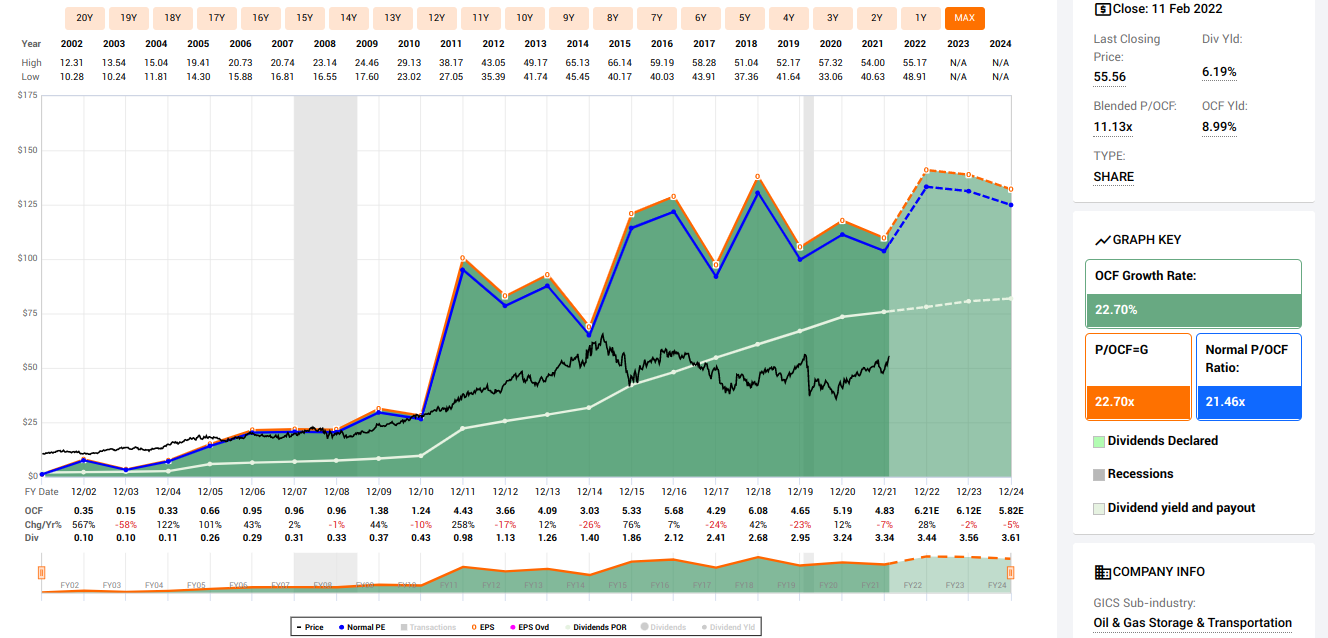

Sold: Shaw Communications Inc (SJR.B)

They haven’t growing dividends for a while, so I rather lock profits here and deploy funds on other companies. Earnings are estimated to be flat, which increases my perception that dividends won’t be raised anytime soon. Their cash flow is more than enough to cover dividends, so my take is simply to focus on companies with dividend growth or companies with a higher growth potential based on earnings and cash flow growth estimates.

Sold: Andrew Peller Ltd (ADW.A)

Andrew Peller is a small cap company, so it’s difficult to get consistent data for historical earnings, cash flow and accurate estimates. I will be deploying funds to larger companies since I have other mechanisms to invest and trade on small cap sectors, through my trading models.

US Portfolio:

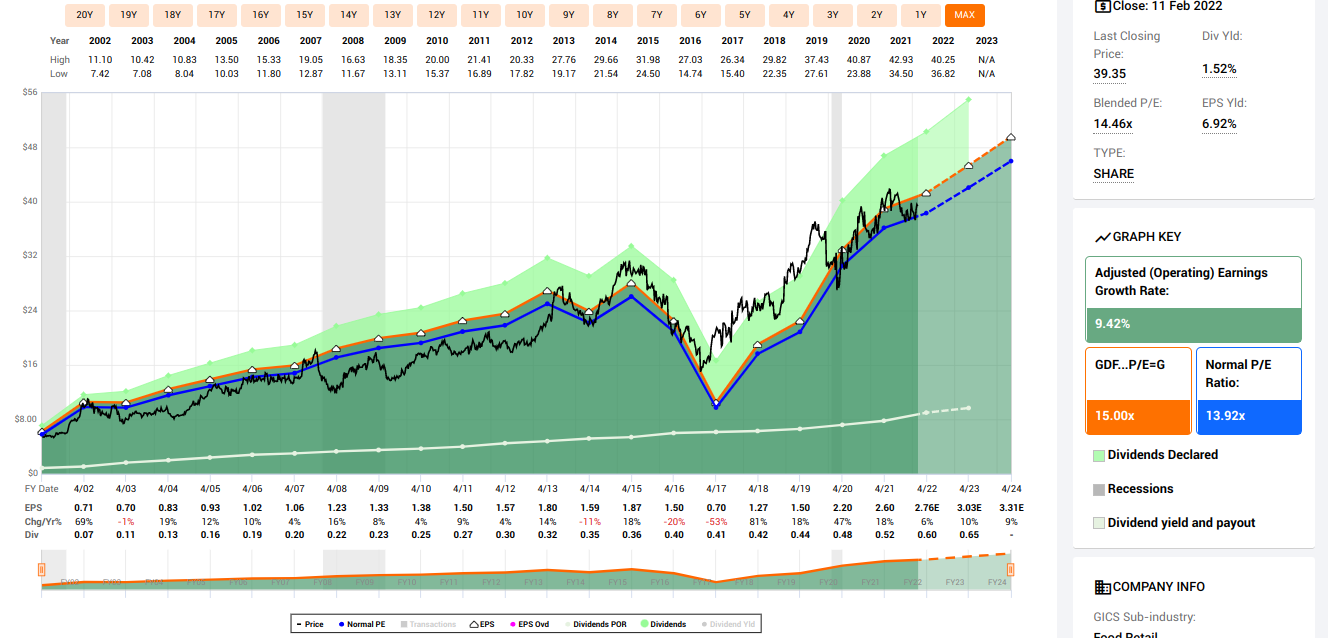

Sold: Walt Disney Co (DIS)

The pandemic affected the reliability of DIS to continue producing dividends, so I will be locking profits here and deploying funds to other companies with a better consistency of paying and growing income in difficult times.

The proceeds will be allocated to companies that I consider fairly valued right now, and estimated to grow. Below are a few examples of some companies on my watchlist meeting this criteria, in which I will add exposure:

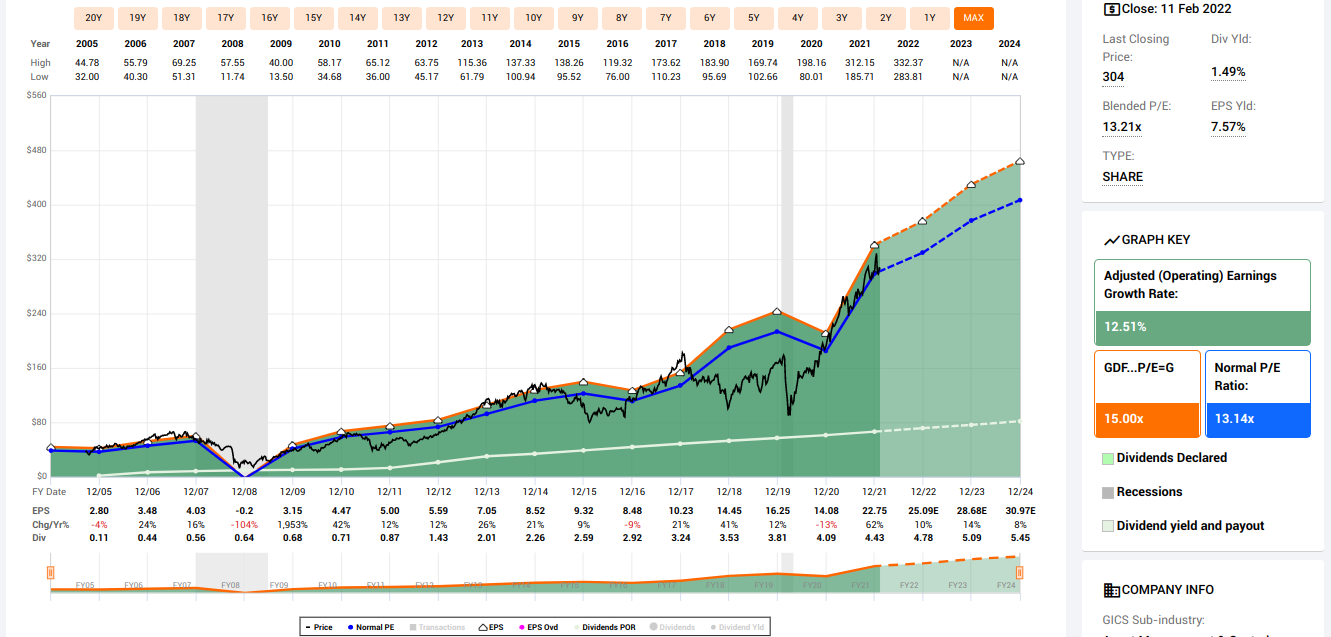

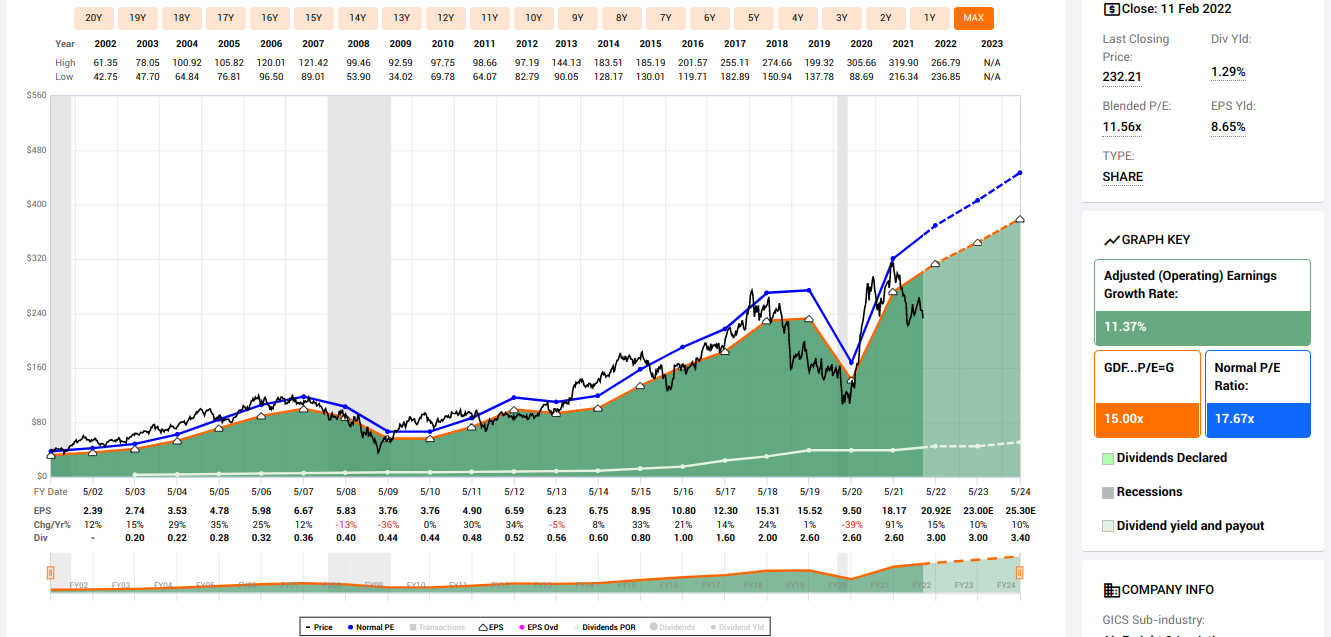

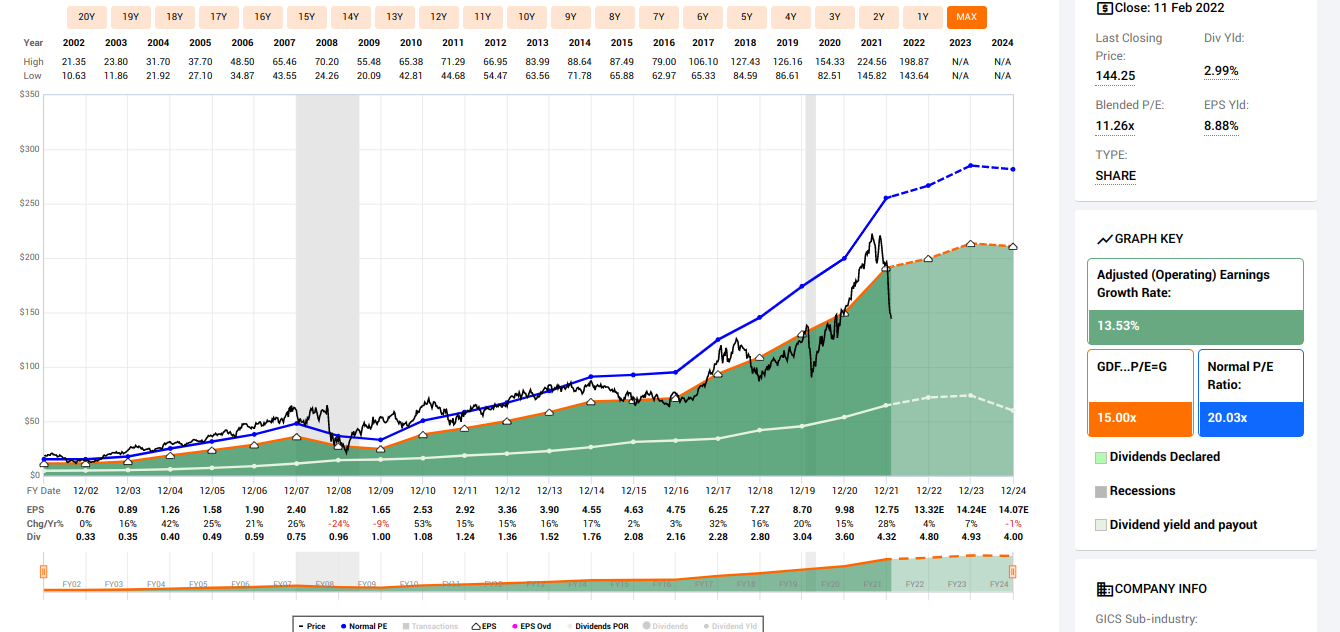

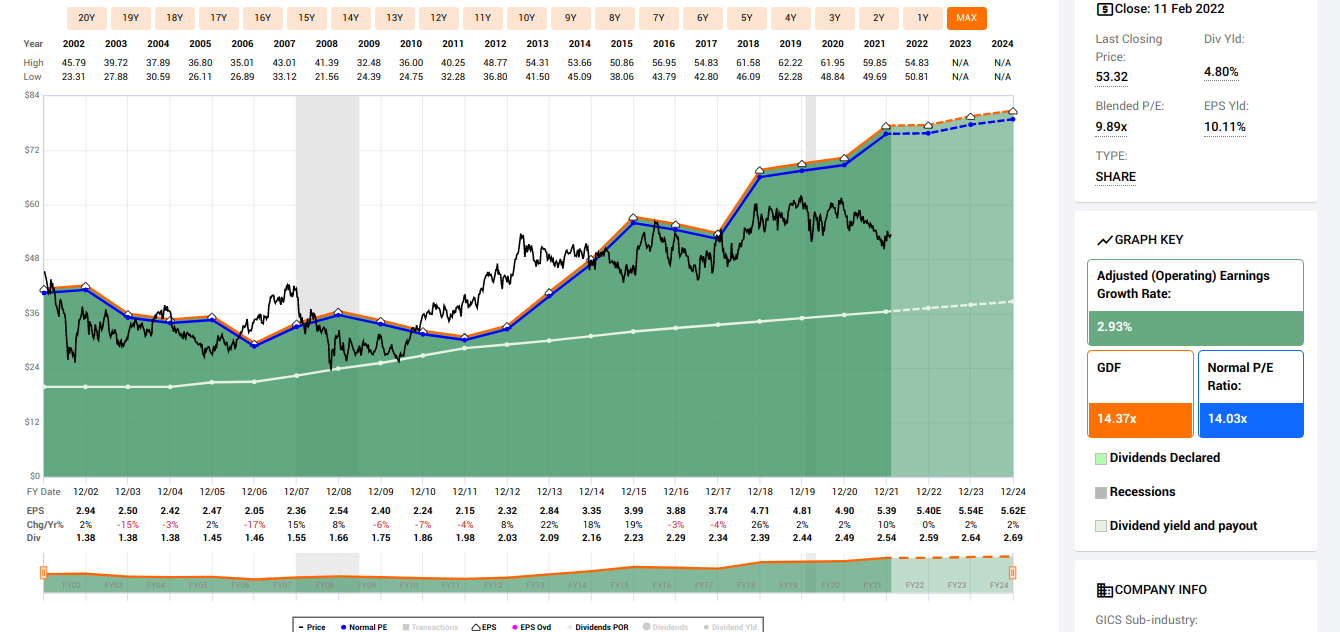

The Bank of Nova Scotia (BNS.TO):

Cogeco Communications Inc (CCA.TO):

Canadian Tire Corporation (CTC.A):

Dollarama Inc (DOL.TO):

Exchange Income Corporation (EIF.TO):

Empire Co (EMP.A):

Enbridge (ENB.TO):

IA Financial Corp (IAG.TO):

Open Text Corp (OTEX.TO):

Stella-Jones Inc (SJ.TO):

On the US side, there are some options as well:

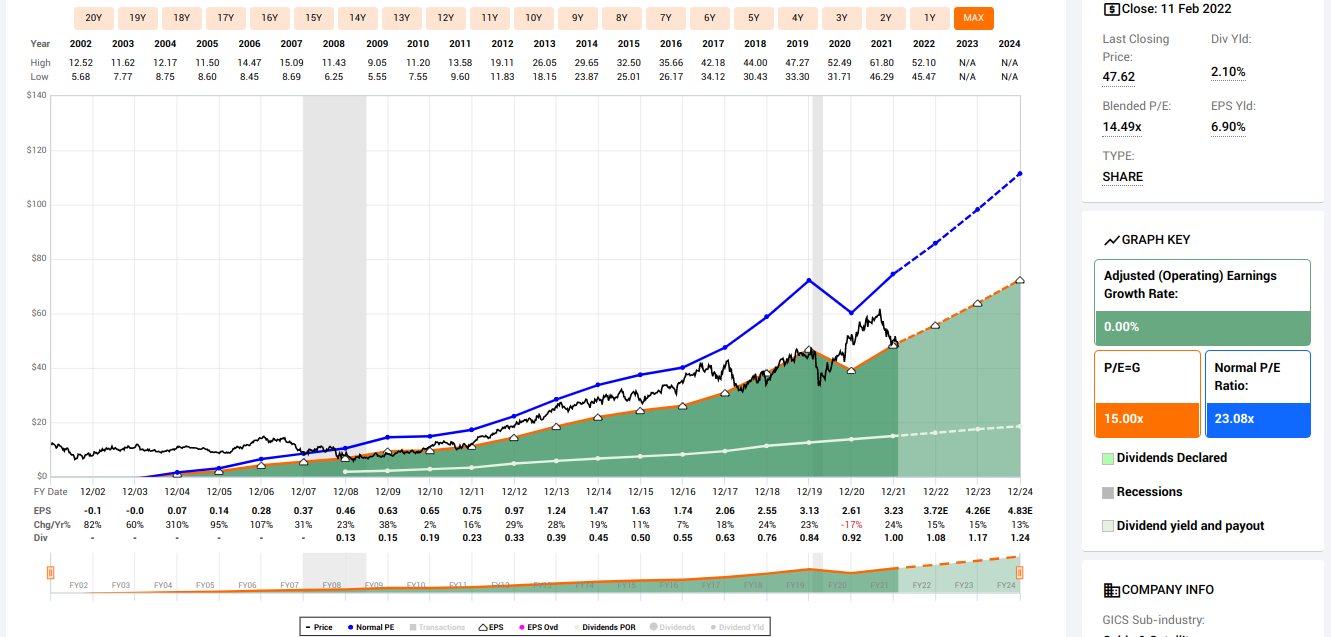

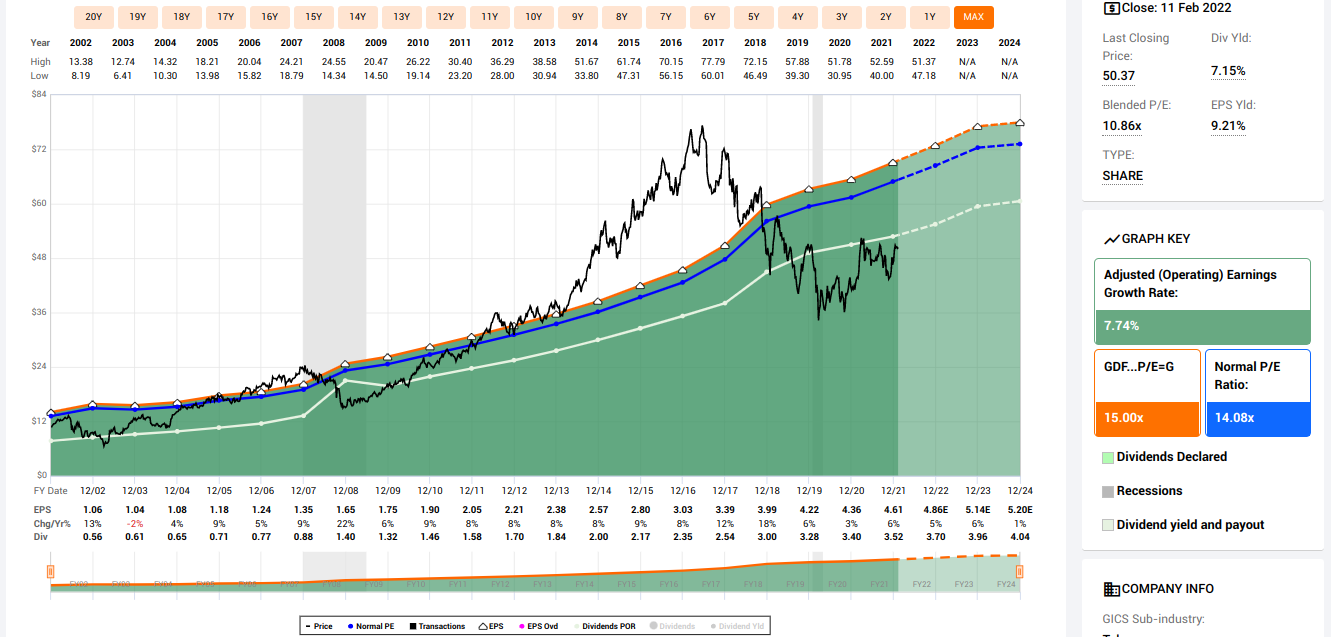

Amerisourcebergen Corp (ABC):

Aflac Inc (AFL):

Ameriprise Financial (AMP):

Cardinal Health (CAH):

Comcast Corp (CMCSA):

Fedex Corp (FDX):

3M Co (MMM):

Altria Group Inc (MO):

Northrop Grumman Corp (NOC):

Qualcomm Inc (QCOM):

Stanley Black & Decker Inc (SWK):

AT&T Inc (T):

T Rowe Price Group (TROW):

Verizon Communications Inc (VZ):

Walgreeens Boots Alliance Inc (WBA):

Lots of options to invest right now, since we can always find fairly valued companies in any market. Eventually, the portfolio performance will be a function of how these businesses perform. Stay consistent on the methods you employ to partner with these business or move on, always looking on the business behind the stock.

Please let me know if you have any questions or comments!

Happy Investing!!

Hey Rod, I follow you on RFD:

I am just wondering if you still share your full watchlist? Ie. companies that you watch and monitor and explain why you like them but it doesn’t necessarily mean you’re buying them

Also, great exit on TSX:BOS from Feb 2022. It seems like you got out just in time

Yes, the watchlist is updated every year, so I will be updating that in a few months. I have been busy with other projects and haven’t been able to post my purchases, but the watchlist is valid, as it’s reviewed annually.

I expect a recession for next year, so I am waiting for lower valuation to have a more aggressive buy. Meanwhile, I rely on my trading models to have a more active approach in the short term.

BOS is highly cyclical, so valuation wouldn’t be justified at those levels.

Rod

I’ve followed your Graham trading and Dividend threads from RFD in the early days, 2015. Led me to Graham’s book and Buffett’s essays.

Agree with you that the risks of recession are significant and am also more strongly on the sidelines, despite conventional wisdom against market timing.

Wishing you the best success as we continue to build our portfolios in the coming year.

Thank you, appreciate the kind words!

Looking forward to a 2023 full of opportunities to acquire more quality companies at a great valuation!

Rod

Thx Rod for your writeup and quick reply.

I noticed that MIC on your wishlist doesnt exist anymore. I think Brookfield bought them.

Correct, I mentioned MIC being delisted on my post and I thought I removed them from my watchlist, I check again andwill remove it from there.

oops. missed that

thx

Thx Rod.

You wrote that

The proceeds will be allocated to companies that I consider fairly valued right now, and estimated to grow. Below are a few examples of some companies on my watchlist meeting this criteria, in which I will add exposure:

Does this mean that the rest of your watchlist does not meet the fairly valued criteria? or the companies you posted were just some examples but there are others on your list that are fairly valued.

Thanks for all

Hi John,

The companies I mentioned are the ones I found most undervalued (or fairly valued) and estimated to grow. The rest of the companies either don’t have a great growth prospect for the short term (I rather add them when they are more undervalued than now) or they are not fairly valued (I rather wait to acquire them at lower prices, which will also provide an initial higher yield).

Rod

Thanks Rod.

Hopefully you can help me with an allocation question.

I remember reading somewhere (maybe on your website) how to initially deploy capital when only some of the companies are undervalued/fairly valued but cannot find it now.

I would like to partner with companies across the 10 sectors by generally following your wishlist and valuation process (using fastgraphs as an aid etc.) but whenever one decides to invest only some or most (but not all) of the companies are undervalued/fairly valued, so how to go about dividing the lump sum amount.

As I see it, the best way would be to to divide among the entire wishlist and place orders at the undervalued/fairly valued amount. Therefore companies which are presently undervalued/fairly valued will be purchased and the rest of the companies will be purchased once they are undervalued/fairly valued.

I will also have to review (and possible modify) the undervalued/fairly valued amounts when any of the input data changes (in both directions), dividends slashed, EPS increase, etc

Thanks Rod

There are different ways to go at this. My setup is to allocate somewhat equally to different sectors, so if I have $100k to deploy and 10 sectors, I want to have $10k per sector to start. Overtime this will skew as some sectors pick up more than others. A sector with 4 companies on your watchlist would have $2,500 per company, a sector with 20 companies would have $500 per company. Sectors tend to be cyclical, hence my preference to start equally distributed. Once you have an idea how to construct your portfolio based on that allocation, comes the decision to deploy all at once on what you think it’s fairly valued and estimated to grow versus deploying slowly. I prefer to deploy in a lump sum to everything I think can start working for me, but some people find it too risky. So my suggestion on these cases is to divide the funds in 4 parts and start with 25%. Then you deploy another 25% on whichever scenario happens first: a 10% drop in price or 3 months went by. This way, you will be fully invested when there’s a significant discount or in up to a year. Overtime, as dividends pile in and other funds become available to invest, you can increase exposure to the companies / sectors that you want, provided fundamentals are in place and valuation is sound.

Please let me know if you have any questions.

I noticed that you didn’t have any additions to your list. Just wondering if that’s because you weren’t actively looking to add to this portfolio, or you looked and didn’t find any new ones to add?

Also, if you have time, I’m curious on your thoughts on AQN, CPX and TRP

As always, thanks Rod

Nice write-up! I’ve been looking at many of the same and would include OLDE, BAH, CMI, BLK, and SWKS. Happy investing!

Thank you so much for such a great work.

I am not able to see your excel, can you please fix this?

The Excel spreadsheet that we used to have for the dividend portfolio is no longer being tracked on this website. I am busy with other projects so I am not posting when I enter each time. But I continue to use the same methods documented on other posts. The spreadsheet regarding the performance of the premium models should be available and working, please let me know if you can’t view it.

Glad you still have TROW… I bought some and was doing great.. Unfortunately, I added more near the high, but I’m still positive (but not by much). Still holding for I have seen other people recommending the stock as well.

Yes, TROW is a solid business and I expect it to continue to grow earnings and cash flow, which in turn will grow dividends for many years to come. Stocks are most attractive when they are not popular. That’s the opportunity to add more, as long as fundamentals remain robust (which is the case for TROW).