Public Model

Based on Graham (Canada)Benjamin Graham is the father of value investing, and the success of his strategy was based on value and company fundamental strength with an emphasis on survivability and stability. The approach was initially created over 80 years ago when the Graham and Dodd’s college textbook “Security Analysis” was published.

Graham’s approach focuses on the idea of an intrinsic value which is justified by a firm’s assets, earnings, dividends, and financial robustness. Focusing on this value, he felt, would prevent an investor from being misled by the misjudgement frequently made by the market in times of deep pessimism or euphoria.

This strategy is well described on his book “The Intelligent Investor,” first written in 1947.

First, it’s important to note that this is not an optimized model – it simply screens stocks as per Graham’s rules and have them ranked in a more optimal level. Therefore, I view this public model as an active investing model, rather than a more elaborated trading one.

This is a low-turnover model; although purchased stocks are hold for at least 4 weeks, the model is rebalanced weekly (screening for additional stocks to buy as per the published rules).

This model is based mostly on fundamentals, and it has been revised in December 2020 to not use any market timing rules – the model only uses the buy and sell rules, besides momentum criteria for the ranking. According to backtests, the model might not avoid major drawdowns, however the model only buys when all buy rules are met and it sells when the stocks falls under the top quintile. The decision to remove market timing rules on this model was based on the underlying factors for earnings calculation, which are done differently and no longer represent the original timer created for this model. The ETF model has been revised and it contains portfolios solely based on market timing, which can be used as a hedge (for all models).

This model has been revised to not include companies that have been subject of a recent acquisition or merge, since acquired companies have a defined shared price for the acquisition and in many cases shares would be delisted shortly after the acquisition complete.

In March 2022 the model was adjusted due to the new taxonomy series from portfolio123 to integrate US and Canada as one North America region as per plan to expand and integrate with Asia and Europe data. This affected how the ranking is constructed, so instead of selling when rank < 80, the model now sells when rank < 75 to maintain similar performance and adjusted risk return ratio as before.

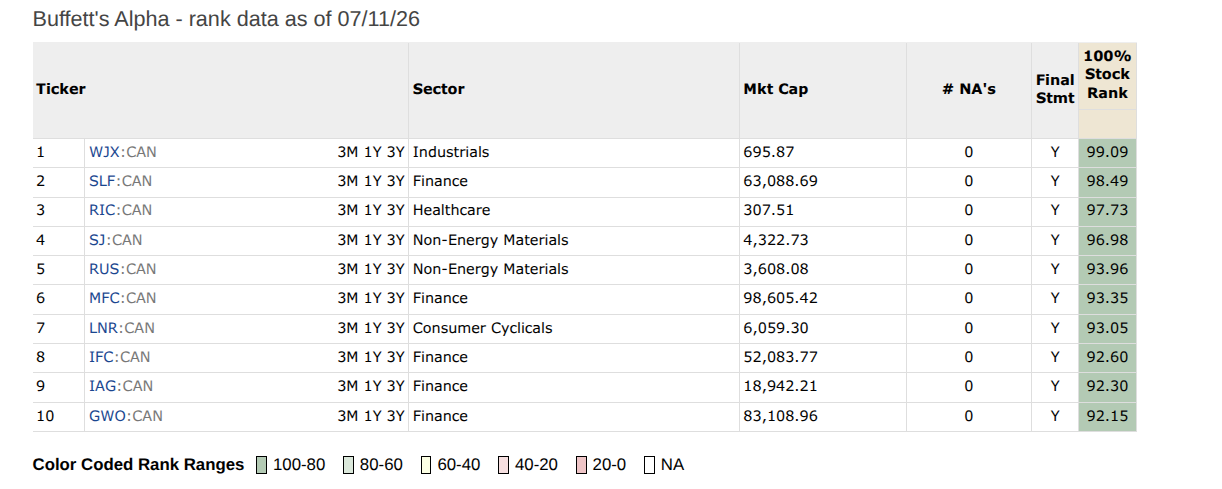

In January 2025 the ranking of the model was adjusted to incorporate the same approach used by Buffett’s when valuing a business, ranking stocks by strong fundamentals, replacing a more generic ranking system based on value, growth, sentiment and quality, with details explained on the rules tab. In August 2025 the model was optimized to sell at a stricter ranking decile.

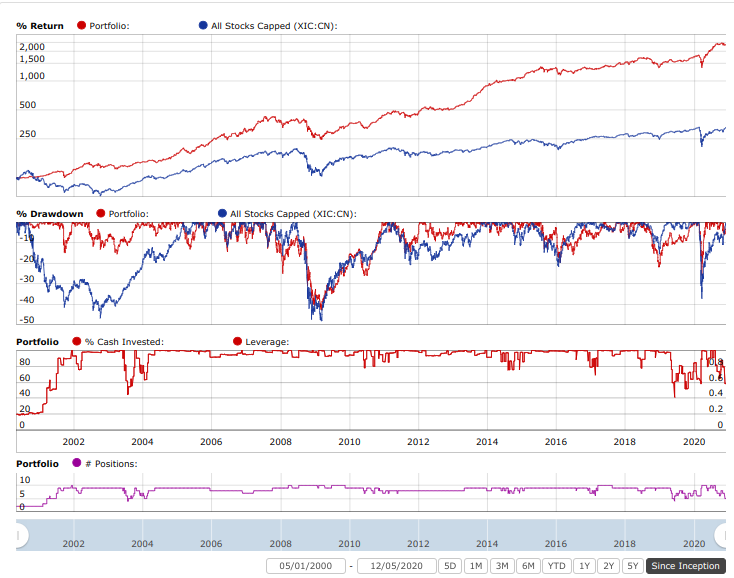

Backtest summary performance with current market timing rules applied (updated as December 2020 with no market timing):

Detailed backtest performance shows maximum drawdown as well as % of invested stocks across different periods (log scale and revised as December 2020 with no market timing):

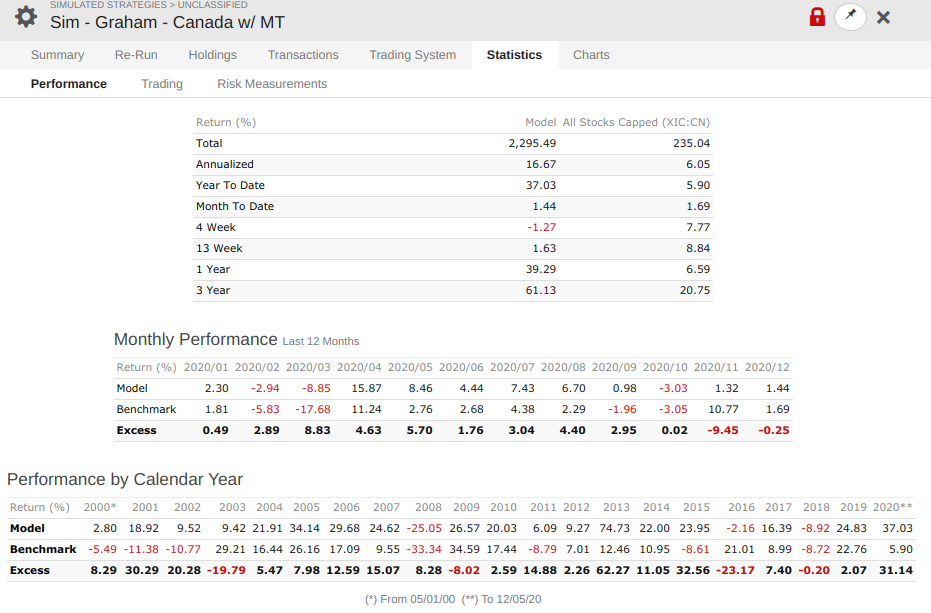

Backtest performance info (revised as December 2020 with no market timing):

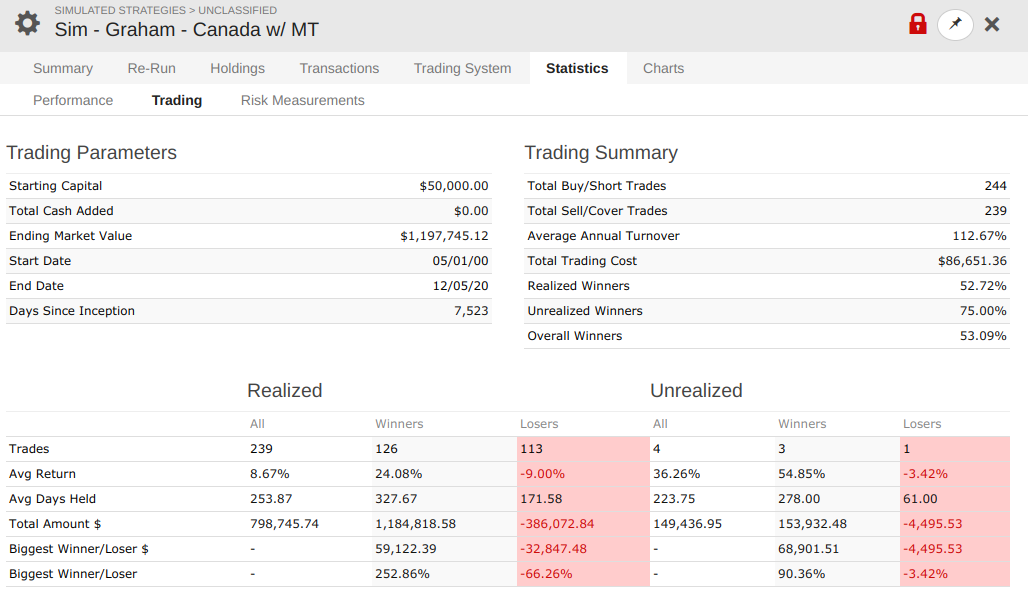

Backtest stats info (revised as December 2020 with no market timing):

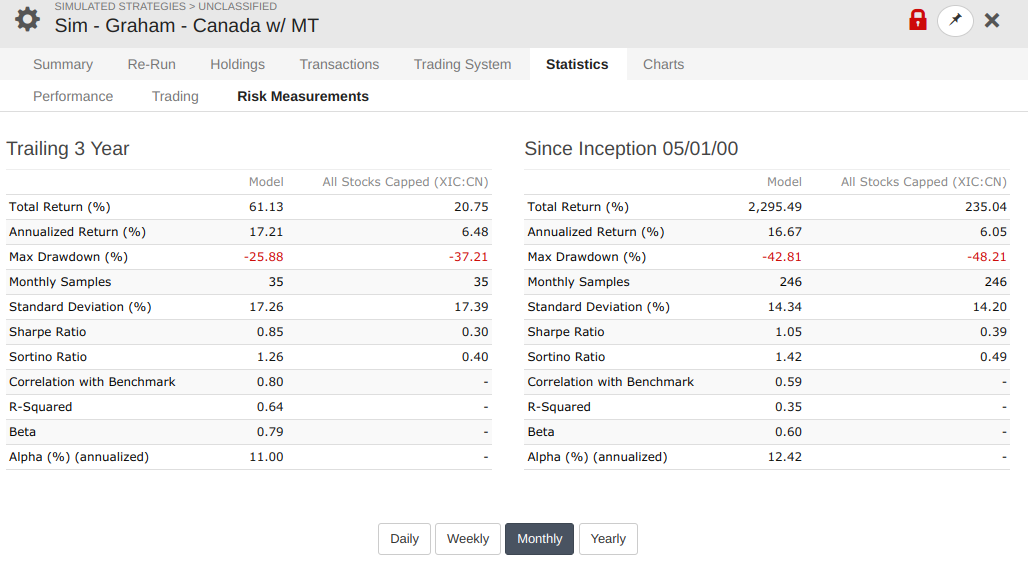

Backtest risk info (revised as December 2020 with no market timing):

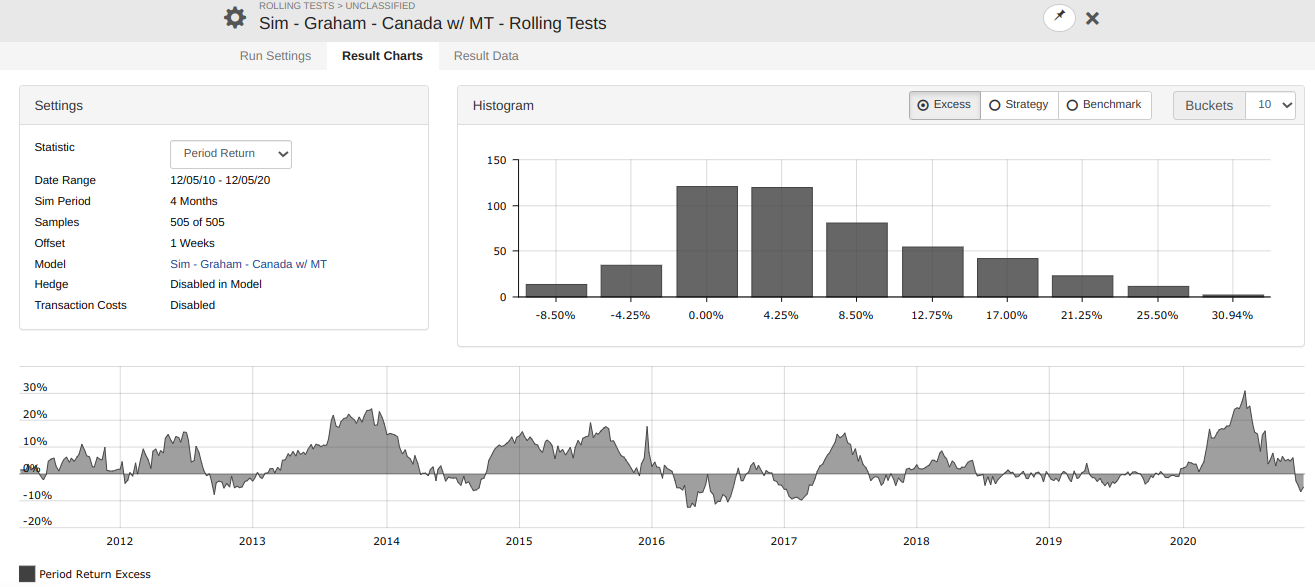

Backtest Histogram Excess performance (holding for 4 months, which is the average duration for the stocks sold for a loss, rotating it weekly, revised on December 2020 with no market timing):

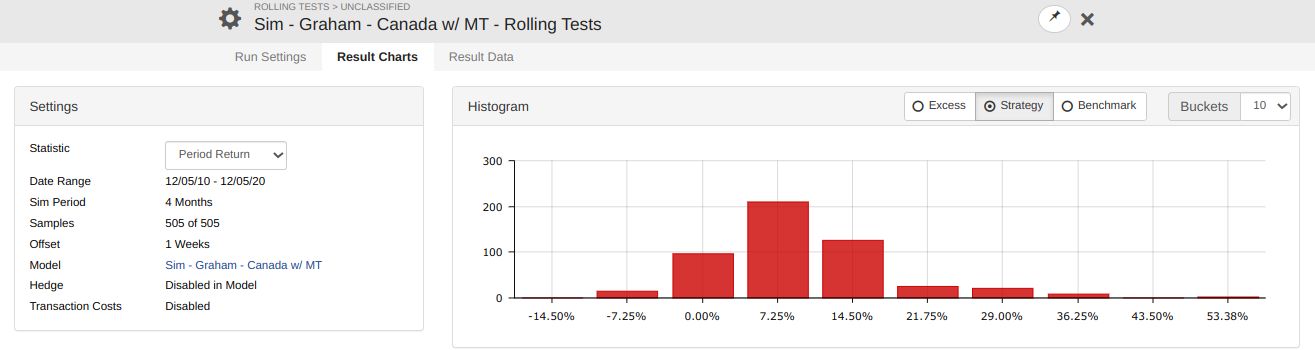

Backtest Histogram Portfolio performance (same period, revised on December 2020 with no market timing):

The universe for this model are the stocks in TSX only – so no Venture Exchange companies.

Buy rules:

– Price > $5 (no penny stocks);

– Current ratio is at least 1.5;

– Long term debt is less than 110% of working capital;

– Last 4 quarters of EPS above breakeven;

– Last 5 years of EPS above breakeven;

– Annual EPS grew over past year and past 5 years;

– Company has paid dividends within past year.

– Rank >= 90

– Average daily total (price * volume) from last 60 days > 100,000

The top 10 companies of the ranking are selected.

Sell rule:

– Ranking < 90

The ranking is based on the following criteria to identify the strongest companies based on fundamentals:

– Highest ROE in a 5 year period: This value is calculated as the Net Income Before Extraordinary Items for the period divided by the Average Common Equity and is expressed as a percentage. Average Common Equity is the average of the Common Equity at the beginning and the end of the period.

– Stability of earnings (good management): Also known as the Coefficient of Variation. For companies that report earnings quarterly, this is calculated by taking the standard deviation of the 20 most recent quarterly EPS values and dividing by the absolute value of the mean. The absolute value is used because otherwise stocks with the highest volatility and a negative EPS mean would get the highest score since stability of earnings uses ‘lower is better’. The company must have at least 16 quarters of EPS values in order for this value to be calculated. If the are less than 16 (as would be the case of an IPO), the calculation is not performed since the resulting value would not be meaningful and will return N/A (reducing ranking score). For companies that report semi-annually, the calculation uses the 10 most recent semi-annual EPS values and the company must have at least 16 quarters of EPS values in order for this value to be calculated.

– Highest Sales to Enterprive Value ratio (Enterprise Value is an estimated measure of the total value of a corporation).

– Highest Free cashflow yield: Free cash flow yield is a return measurement that compares the free cash flow of a company to its market value. A high free cash flow yield result means a company is generating enough cash to satisfy its debt and other obligations, including dividend payouts. Free cash flow, which excludes capital expenditures but considers other ongoing costs a business incurs to keep itself running, is an alternative representation of the returns shareholders receive from owning a business, and may be preferred to net income because it is more difficult to manipulate by management.

Market Timing rules:

In December 2020 this model was revised to no longer use market timing rules, since the original formulas and calculation no longer works, given how estimated data and underlying data set is used by the new platform provider. Buy rules are always screening for new buys and sell rules will screen to meet selling conditions. The model is only in cash if all stocks were sold as per sell rules and no criteria was met on buy rules. It will keep screening every week until a stock meets all rules. If one wants to incorporate market timing, the ETF models have been revised to include portfolios solely based on market timing, which can be used as a hedge.

Next rebalance date:

July 19, 2026

Last signals (July 12, 2026):

No action required

Current holdings (July 12, 2026):

Below is how the holdings should look like AFTER the rebalance. This portfolio has an equal weight distribution, so you might want to consider buying / selling shares (where commissions make sense) to achieve the weight below, as a guideline. It’s ok if you cannot achieve the exact number. Weight below means how much of the portfolio is on that stock.

| Ticker | Weight | Return % | Avg Share Cost* | Days Held | Yield | Sector |

| GWO:CAN | 12.73% | 96.42% | 46.81 | 529 | 2.91% | Finance |

| IAG:CAN | 9.82% | 54.11% | 132.71 | 529 | 2.15% | Finance |

| IFC:CAN | 9.67% | 14.88% | 256.46 | 263 | 2.00% | Finance |

| LNR:CAN | 11.43% | 2.06% | 99.27 | 4 | 1.15% | Consumer Cyclicals |

| MFC:CAN | 8.62% | 33.66% | 43.78 | 529 | 3.32% | Finance |

| RIC:CAN | 5.73% | -12.94% | 32.24 | 529 | 4.70% | Healthcare |

| RUS:CAN | 9.75% | 53.00% | 42.11 | 529 | 2.73% |

Non-Energy Materials

|

| SJ:CAN | 7.58% | 3.16% | 76.51 | 333 | 1.72% |

Non-Energy Materials

|

| SLF:CAN | 9.06% | 32.93% | 85.14 | 599 | 3.39% | Finance |

| WJX:CAN | 9.10% | -2.23% | 32.58 | 116 | 4.40% | Industrials |

Performance Info:

(last updated on July 12, 2026)

Loading Viewer...

Ranking Information (before rebalance):

(last updated on July 12, 2026)

Market Timing indicator (oscillator based on earnings):

The underlying factors for the earnings timer have changed with the new platform provider and calculation, invalidating the original timer. This model has switched to not use any market timer (native as part of the model), and it’s always invested (unless all stocks were sold via sell rules and nothing could be found via buy rules OR the external macro model which tracks recession probabilities crosses the threshold for highest probability of recession confirmation). The ETF models have been revised to include portfolios solely based on market timer as a hedge.

looking at your holdings, you had a recent buy signal for 7 stocks, and they compose roughly 10% each of the portfolio. Am I correct in assuming that 30% is still in cash?

Hi Dan,

Correct, only 7 companies currently meet Graham rules and are ranked high to be a buy. Since this model uses an equal allocation per position, then it has about 30% in cash now.

Please let me know if you have any questions.

Rod

Hi Rod, On Feb 12 you gave a buy signal for GWO. Unless I missed it, I didnt see a sell signal for it yet it is not on your list of current holdings?

Hi Dan,

GWO was sold on June 19. It’s been off the current list since then.

Rod

WOW… Never expected SELL ALL… but interesting….

Looking at previous years, we had other instances where all holdings were sold due to market timing rules on macro conditions. The individual timer on the models have been removed (since it got too complex to bake into an existing trading model), and it was replaced with the ETF Monthly timer. However, if we have a strong recession signal, then all holdings on this model are sold since the probability points to lower prices ahead due to deteriorating macro conditions.

The model will resume the buying rules again once the metrics for recession timer shows improvement that leads to a high probability of growth and liquidity cycles resuming again – which allows quality and valuation to be better aigned with price.

Rod

Thanks…

The latest signal is Sell PSI, however in the ranking its at 86.24.

Is this a mistake?

Excellent observation. Not a mistake. This week, portfolio123 (the platform that is used for these algorithmic trading models) introduced new capabilities to support European and Asia data. This integration changed how the universe of stocks are made of, and changed the companies in present ranking composition. The changes are pertaining to rules for the calendar, taxonomy series, and industry-based scope parameters, which applies to all models. This means that this week had some different numbers for the functions used in the ranking. Now US stocks appends with :USA and Canadian stocks will append with :CAN. From an Universe perspective, it now differentiates stocks that are dual-listed on US and Canadian exchanges versus foreign single listing. For example, for the single listing SHOP:CAN and CNSWF:USA are foreign primary listings. The reason Shopify, which is headquartered in Ottawa, has its primary listing in the USA is that it went public on the US and Canadian exchanges on the same date and its US listing is more liquid. Similarly, Ovintiv, which is headquartered in the US, has its primary listing in Canada (OVV:CAN) because that listing goes back to 1983, while the US listing dates from 2001. Since the primary listing is determined by the history and liquidity of the various listings, it affects the companies in the Universe considering that integration. From a ranking perspective, the rank got adjusted to continue to meet the rules of the model, and a new re-run simulation doesn’t include these companies in the current portfolio that got the sell signal today, as it wouldn’t be a buy according to the new changed rules. Therefore, they are being removed without waiting for their ranking to drop because this company wouldn’t be a buy in first place. I didn’t want to leave it there and wait ranking to drop to eliminate because it wouldn’t match a recent simulation running the new companies. So it is being sold on Monday to match the recent backtests on the new revised parameters given this platform change. Please let me know if you have any questions.

Where do you see the ranking?

On the model webpage (for Graham model, where the info is public), go to Performance and Stats. Scroll down for the rank info. https://boostyourincome.ca/trading-strategies/based-on-graham-tsx/

Please let me know if you have any questions.

Thanks I see it now.

Being in CASH sure has helped the performance when compared to the index !! I too have felt things being overvalued.

Hi Rod,

I am new here. When you said buy for GWO, what’s the entry price? or I just buy it when the market opens on Monday?

Thanks

Hi William,

Correct, when a buy signal is issued, it uses Friday’s closing price, but it will be adjusted for the average of high and low on Monday to reflect the price that the model entered at. So on Monday it can be purchased at anytime to replicate the model signals.

Since AEM is buying KL and KL will be replaced by 0.8 of AEM, should we sell KL or wait for the replacement?

Hi Dee, apologies that I missed this message. We should mimic the same allocation suggested on the model to mimic the same performance. On this case, keep KL until the replacement takes place.

Hi Rod,

I noticed that your average days held for your stocks are around 200 days. I’m curious what you think about buying call options with a 200 day expiry with the same buy/sell signals as an aggressive strategy.

Interested in hearing your thoughts

It’s a risky approach because although the average is 200 days, not every trade holds for 200 days. Some hold for a week only. And some close at a loss. Options just amplifies return, good or bad. The other downside is the difficulty to control size. An options contract on a company like CNR will have a very different weight than a contract on EMP.A. A LEAP approach can work if you can manage to control weight equally, but that will require a lot of capital.

Rod

Hi Rod, I joined late and was wondering if I should still buy LIF given it’s high price compared to your price?

Your previous signal was Sell SJ, now today its buy SJ.

Any reasoning for this?

Yes, SJ was sold last week due to ranking rules. The rank score for every security is updated weekly, and SJ went below 80, so it triggered the sell rule. However, it continues to meet all buy rules and ranking has improved over 80 now, so it’s a buy again. It will be held for at least 4 weeks before evaluated to be sold again.

Lots of volatility in this market…… Sometimes big moves even in value stocks….

Dear Rod,

In the current holdings tab, the table has a heading that looks like this: “Avg Share Cost*”

But when I search for what the asterisk signifies, I can’t find it.

What does the asterisk mean?

Great question, this is fed automatically by portfolio123 and it’s not part of the data collected and displayed on my website.

The asterisk means “Includes Commissions “, to reflect that the average price on the table includes a commission of $4.95 to simulate brokerage commissions, for a more accurate performance curve.

Missed it on the Monday.

So I missed the buy on Monday (browser cached previous week and I didnt refresh). It’s Wednesday now.

Should I still buy or wait until the following Monday?

Signal for this model last week was to sell LIF.TO, this week is to buy it back (at a higher price). I just wonder what prompted the 180 within the span of a week?

It sold last week because rank was less than 80. And it both this week because buy rules are all met and rank is higher than 80. Ranking is done by several rules, not just company guidance.

Ok read the article – they had some special div provision- creating confusion across. You can remove the previous comment

Correct, their special dividend was declared as a quarterly dividend, hence the high yield. It’s likely that future ones will be around previous yield, which is about 5%.

Hi Rod,

Any rationale not to use market timer any longer for this trading model? The S&P 500 earning guidance is not good any more for timing the market and estimate the risk?

The original market timer which was based on guidance for all companies of SP500 needs to be re-written, since the data on portfolio123 is now fed by FactSet (it used to be fed by Compustat). So some of the original functions and formula no longer work, they need to be re-written using different datasets that points to the same information as before. This Graham model is more of an investing model than a trading model and it wouldn’t make sense to halt this model in cash until this timer is ready. As an alternative, the ETF premium models have been revised to incorporate different market timing signals, which can be used as a hedge or decision factor to invest in this or other models. They use other factors, but not earnings estimate for all companies as this previous timer did. I might re-write this timer in the future, but I have other priorities at this moment – including updated blog posts, updates on my watchlist and refinement of a new US small cap trading model that I plan to launch.

I noticed the # of days is “negative” Is that because you plan on buying in a couple of days (Ie signal says buy, you tell everyone, and then you buy ?)

Correct. The buy signal is placed before the actual buy takes place, so it shows as negative days. On Monday that will be zero days and then it starts counting for how many days that stock is being held.

I see the model here – so it’s all cash. But do you have any recommendation for passive investor who is investing to use their TFSA and RSP allocations and not looking for magic return, once indicator changes? I tried TD mutual fund – they don’t move at all (with 3% MER expected).

Also just making sure – all cash does not mean selling income stocks like ENB etc.

Correct, all cash is for this specific trading model. My dividend investing model is always fully invested, as it uses no market timing. And my other models (which are both focused in trading and investing) are all fully invested as well.

It depends on your goals, risk tolerance and time horizon to define in what to invest, and your time and effort available to define how to invest. I am finishing my watchlist for 2021, and will post a few ideas soon. I also have a specific post ready to go on how to start, addressing your question (which I get asked from time to time). We can discuss future ideas then. Alternatively, feel free to follow this model, it’s low turnover and focused in finding good valuation according to the principles documented by Graham. Just one of many strategies available to invest.

How do assess which premium model is best suited to me? Is there an investor profile section based on Risk tolerance and type of investment (TFSa vs RRSP)?

The best way to evaluate any model is by understanding the underlying strategy (balanced, growth, income approach or based on ETFs) and then learning how the rules and principles to find stocks on a given model align with your goals and risk tolerance.

The different models are simply different screeners with different ranking systems and formulas tied to a financial idea. It’s always scanned and calculated the same way to ensure consistency. Not always those financial ideas translate to immediate returns, but overtime these ideas continue to drive growth since they are implementation from known investing books and research papers, performing the calculations that would take much longer if we had to do individually.

Also, market timing indicators have been revised and improved since the last crash in March proved to have a much higher velocity than found in previous recessions, so this will be taken into account in the future.

Some models are focused on investing: low turn-over models, focused more on fundamentals and less on price action. Examples include Business Expansion, Nasdaq and NYSE leaders, Consumer Staples Value, Seeking Income and Quality (all US stocks) and Earnings and Dividend Growth and Defensive Sector (Canadian stocks). Some of the ETF portfolios are also investing oriented / long term focused (US ETFs). Other models are focused on trading: higher turn-over models, focused more on price and momentum and less on fundamentals or valuation. Examples include Momentum of Fundamentals, Value, Sentiment and Momentum and Improved Dogs of TSX (Canadian stocks) and some of the ETF models (US ETFs).

Models are rebalanced weekly, they are not meant to daytrade, since there are fundamentals into consideration, just at a lower or higher scale depending if the model is focused on investing or trading.

The consideration on where to trade (TFSA, RRSP) is outside of the scope of these models. My setup, which makes sense to my circumstances, is to always maximize TFSA first, and then populate RRSP only if I will be on a lower tax bracket during retirement than compared to when I contribute. I trade the investing models on my TFSA, but I trade the trading models on a margin account, since CRA could argue that I have frequent trades on TFSA for the high turnover models. My TFSA typically hold US dividend stocks, since US stocks in RRSP are not subject to withhold tax, but you need to evaluate your own situation to determine if RRSP makes sense on your case.

Feel free to reach out directly at info@boostyourincome.ca if you have further questions.

Rod

I think in your last line you meant you hold US dividend stocks in RRSP account.

So currently it’s all cash. Do you leave the cash sitting in the brokerage account to wait for next week or move it to a savings account in the meantime?

I leave it in CSAV ETF to earn a little bit while waiting for the next signal. It takes several business days to move between savings and back, making it not ideal as we wouldn’t be able to buy when it gave the signal to do so.

A bit off topic.

It’s my first time with this model so I haven’t seen the prior prices of the companies and allocations.

What’s the suggested portfolio size for this model?

I was gonna start with one share each instead of cap weighted, but realized it won’t work well if later on a share is going to be $100+.

Hello,

The holdings tab has the suggested weight allocation. The model holds up to 10 stocks, and start with equal weight allocation, so 10 stocks mean 100% weight allocation. If you have $10,000 to allocate to this model, then you would allocate $1,000 to each position. Since this model presently has 3 positions, then it’s 30% allocated, and 70% in cash. Therefore, in this example, it would have $3,000 invested ($1,000 to each position) and $7,000 in cash.

Always think of the allocation (to any model) as dollar allocation, not number of shares (prices vary per company and can change within the same company with a stock split).

Please let me know if you have any questions.

Rod

Bold call to liquidate all…

But then again I’m not surprised. I’ve lightened up myself…..

The liquidation was based on the timer rule, which takes earnings guidance into account. Earnings guidance has deteriorated across all sectors, and it’s usually prudent to stay in cash during this situation. It doesn’t mean that the market will tank. In 2016 it continued grinding higher. But it carries more risks, and the point of these models is to reduce risk. The model will be back to equities once the earnings timer crosses the buy threshold.

When you post your weekly “current holdings”, is the weighting that is reported correct as of the date ? ie CGY:CN 13.26% on Aug 2nd, assuming CGY is priced at $59.25

Correct. This is because positions are not rebalanced until significantly in profit (or loss). This model is up 74% on CGY, so the weight is increased proportionally to the rest – it never rebalanced.

The model is meant to start with equal weight balance, so I typically allocate equal dollar amount to all positions when starting. Usually proceeds from a stock is used to buy another. If more than one stock is sold, the total is split equally for the next stocks to be purchased. Starting now with the suggested weight mimics the model the closest, but has added risk for weight inbalance. So a more conservative approach is to start equal weight.

This only applies to this model; the other trading models have a risk base weight rank, so it the portion allocated is based on specific rules and should always be followed accordingly.

Rod

Hi Rod,

Can you briefly explain the tax implications on the TFSA if we sell frequently by using this model?

Hi Vijay,

For tax advice you need to speak to a certified accountant, but what I can say is that this Graham model has a very low turnover, which means it doesn’t trade often. CRA says that TFSA is not meant to be used for day trading or frequent trading, and these models don’t trade frequently. If you look at the Stats tab, which is updated weekly, each position is held for an average of 176 days (almost 6 months) before it gets sold. The model checks weekly if there are new positions to be purchased (if it isn’t fully allocated), but each position is held for a minimum of 1 month. So some positions might be bought and sold in a month, others stay invested much longer, which gives that average of 6 months holding period. Looking further, the stats also shows that losing positions are typically held for 4.6 months, while winning positions are held for typically 7 months. Therefore, the model is designed to behave like a form of active investing, rather than quick trading.

Do you track the performance of he public model ?

Yes, performance info is updated every week. The tab “Performance and Stats” have the performance information for each model, as well as the spreadsheet under Trading Performance sub-menu (under Trading Strategies).

The performance of this portfolio when compared to the index is going to do extremely well given the amount it had in cash !!!

The model dictated that it should be cash, and good that it was !!

The portfolio is very much in Cash.. Do you envision this being the case for a while ?

Market is overvalued, so a value approach tends to underperform when it’s mostly driven by momentum. The portfolio is partially in cash because other stocks don’t meet the Graham buy rules or they meet but they are not ranked in the top quintile from a quality, value, growth and momentum perspective. The portfolio is uniquely designed according to these principles, so they shouldn’t be compared to the market, which is based on market cap. There’s no way to predict if the cash portion will increase or decrease, as the list of all TSX companies are evaluated on a weekly basis regarding to the buy and sell rules.

I created a this exact portfolio on TDWaterhouse platform… Even though its been roughly 30% in cash for 6 months, its still managing to keep up with the index..

Would you consider doing a Graham model on American stocks?

At this moment, I’m working to develop new models, and a new US Premium model based on Business Expansion will be launched very soon. I might consider doing a US-based Graham model one day, but it’s not in the short term horizon. Having said that, a lot of the US dividend growth purchases that I post on the blog follows Graham and Lynch principles, and can be used as further candidates for research and purchases.

LNR is taking a beating, would you consider selling and reinvesting the funds elsewhere?

No, that’s the whole point of trading a model that issues signals via an algorithm. If I lock my losses now, I’m deviating from the model, because it’s supposed to sell when rank falls from the top 20%, and it’s not there yet. This is a model oriented to value, and many times it will find stocks that keeps getting undervalued and hurting performance. So I rather wait for the combination of fundamentals that composes the rank to deteriorate first, before making a decision. Other models have sell rules based on momentum or price reversion, but this model focus mostly on fundamentals to issue a sell signal.

Having said that, it might continue making new lows until the rank falls enough to have a sell signal, to close lower than today. But it was the lower rank, not performance, that drove that decision. And by consistently following these rules, it allows to take emotions out of the equation.

Hi Rod,

Thank you so much for providing this info. I put my first orders for tomorrow based on your suggestions. I only see 8 picks now. Will there be more?

Hello,

The model rebalances weekly, so every week it will be scanning for more stocks that meet all buy rules and are ranked in the top first quintile. Until that happens, the model will continue to hold 8 stocks or less (if other stocks meet the rules to be sold and no other stocks were found to be purchased). For now, this model will have 20% of their allocation in cash.

Please let me know if you have any questions.

Rod

How do you use your market timing rule with your buy sell rule? It appears not part of your buy/sell rule

The market timing rule is the very first rule checked before it starts scanning for stocks. In Portfolio123, that’s configured under Hedge / Market Timing, where I specify to go to cash if earnings across the board drops according to Lambert’s indicator or switch to equities. Hedge / Market Timing supports formulas for this calculation. Once the model knows that it’s in equities, then it will screen the stocks specific in the Universe (TSX) and go by the rules in the Buy section. Now, it will only buy the stocks that meet these rules. Therefore, the model can hold only a few stocks or maybe nothing (100% cash) if nothing met their buy rules. Portfolio123 doesn’t support Canadian ETFs, so when the market timing flags to go to go to fixed income, the model switches to cash (performance listed in green background), but I personally switch to short term bonds ETF, until the model switches to equities again.

Please let me know if you have any questions.

Rod

Hey Rod – Are you manually entering these trades or if we buy a P123 subscription, the rules entered can connect with IB to algo trade the rules?

Thanks!

Hi Sam,

I enter my own trades in P123, as I have different accounts in IB meant for different purposes. P123 offers auto-trade with IB, to have your own models in auto-pilot. See more details here. However, P123 is expensive, and meant to be a platform to design models, so it’s usually recommended that one uses more features than simply their auto-trade feature. This Graham model is public, so any P123 member can copy the rules and ranking and trade themselves, including using auto-trading. It also gives the flexibility for one to modify / improve / optimize the model as well.

Hi Rod, thanks for creating this, really appreciate it. I was following your thread on RFD off and on previously and recently decided I’d like to try this. After the next re-balance, so Monday November 20th, would I buy all the listed stocks based on their weight after the re-balance? So if buying 50k worth, it would be 50k x weight of each stock?

Thanks

Hi Alex,

Correct, you distribute the weight equally, so you’d start with $5K for each stock. I personally rebalance th equal weight every time there’s $1,000 worth of rebalance to be made.

Please let me know if there are any other questions.

Rod

Hi Rod,

Sorry I’m confused by your reply. To follow the model now would i buy 5k of each stock or would it be 50k x the current weight of each stock?

Thanks,

Alex

Hi Alex,

There are 2 choices: allocate equal weight amount to the stocks ($5k each) or follow the suggested weight model ($50k times the current weight of each stock). Here are the differences:

When the model started, it had equal weight distribution, so 10% on each stock (if it started with $50k, it would have $5k on each stock). The weights are not perfectly equal now because rebalance happens only if there is a 10% weight deviation between stocks, and winners that have been held for a long time keep driving the weight up. When a sell signal is issued, the proceeds of that sell are used towards the buy of the next stock. If 2 stocks are sold, then I divide the proceeds by 2 and allocate that amount to each new purchase. So which method to use?

I prefer to start with equal weight, as it balances the risk of the initial stocks when you start, and then the weight will change eventually depending on stock performance. However, that won’t perfectly mimic the model, because the model started before you did. If you truly want to mimic the model performance, then you should have your total amount ($50k) times the current weight of each stock, exactly as the model is setup now. But that means allocating more weight to the winners of the model and less weight to the losers of the model, even though you were not invested on those winners. Hence my personal choice is always to start with equal weight and then go from there.

This only apply to this model, which doesn’t have rebalance and reconstruction done independently – Premium Models have specific weight allocation, and one should always follow those, as they are rebalanced / reconstructed at every rebalance.

Please let me know if there are any other questions.

Rod

Hi Rod,

Is it possible to post the strength oscillator (market timing rules) along with updates? Bi-weekly, or monthly seems sufficient.

Thank you for your continued work.

Absolutely, and that’s a great idea. I’ll soon post with the other performance stats.

Rod

Market timing oscillator posted under stats. I’ll update it on a weekly basis, along with other stats info. Thanks for that suggestion.

Rod, possible to set up a notification on each update? I’m often a few days delayed… sometimes a month delayed. Would love some sort of notification letting me know about an update!

Hi Adam,

Since subscription is not required for the public model, there is no way to send notifications. However, updates are done weekly, and it should be in place by Sunday night or Monday morning. This model employs market timing weekly, so it’s a good idea to have a reminder (it can be set on your phone) to check weekly. At this point, only premium models have email notifications.

What platform did you use to generate the above graphs?

Portfolio123. It’s a platform to design algo trading systems using fundamentals and technical analysis, and simulations are done with non-survivalship biased data. Data is provided by Compustat, which is fed by Standards & Poors Global database, CapitalIQ and Interactive Data. The backtest graph is the result of the buy and sell rules, combined with rebalance and ranking rules, applied to different time frames. The same rules are being used on the live model.