Common mistakes when trading

“The stock market is a mechanism for transferring wealth from the impatient to the patient.” - Warren BuffettMost traders and investors can’t help the temptation of chasing performance. They tend to be interested in a model only if it had performed really well in the past, often overlooking what were the components driving the performance or evaluating if performance can continue in the future. The other temptation factor are emotions – fear (of a model temporarily underperforming to be labeled as a weak or broken model) or greed (seeking an infallible way to be rich in a very short period of time, without understanding that this is a process with ups and downs that takes time to materialize). There’s nothing wrong with seeking superior performance or building ways to achieve superior performance. But it should be done in a disciplined and systematic way. Performance chasing should not be due to myopia, irrational loss aversion, or other psychological biases.

Behavioral Challenges

It is not always easy adhering to a disciplined approach. If you are not vigilant, emotions can get the better of you. Even Daniel Kahneman, the father of behavioral economics, admits to being influenced by behavioral heuristics.

We may forget our strategy’s long-term expected outperformance when we experience uncomfortable drawdowns. The survival instinct kicks in strongly then. Recency bias can make us feel the drawdown will never end.

We may also have to deal with regret aversion when our portfolio underperforms. This will happen sooner or later. No strategy outperforms all the time. Occasional benchmark underperformance is the price we pay for possible protection from severe bear markets. Hence it’s so important to understand what is under the hood of a model or strategy, and why constructing a portfolio with low correlation between different strategies, tailored for short and long term goals, are paramount for a superior portfolio.

Myopia

Those who look at performance frequently do not do as well as those who are less concerned with short-term performance. First, it’s important to understand if the premises of a trading model are working as designed. A model focused on growth and momentum won’t have the same driving factors than a model focused on income and quality or a model focused on value. Price can be disconnected from fundamentals in many ways, and there’s no way to predict a defined outcome in a short-term period – models are designed to identify when criteria are met for events that have a high probability of expected outcome – so although a certain outcome is likely or probable, it’s not guaranteed. Evaluating a strategy (any strategy) during a short period of time is myopic, and that goes in both ways – one cannot conclude that a model is really good just because it’s doing great in a short period of time, the same way that one cannot conclude that a model is weak or broken because it’s doing poorly in a short period of time. Once a strategy and rules are understood, one need to conceive that the market not always follows the expected outcome for these strategies, but that’s usually temporary. Also, a bear market would make any strategy look like a losing one.

It is important to keep the big picture in mind. Understand that technical analysis is based on what we see (after the fact), and that’s probability based. Understand that fundamentals (what determines price to move the way they move in the long term) can be disconnected some times, and that’s slow to develop – companies report results only 4 times a year, and a business cycle typically lasts 5 to 7 years. So, do your homework so you understand whatever investment approach you select. Then relax, and enjoy the journey.

Accepting Lower Risk Premia

The other serious mistake that traders and investors make is not understanding the real goal of trading (or investing). We should trade (or invest, depending on the goal) in a way that offers us the highest expected return while limiting our risk exposure. Limiting downside exposure, specially when trading, is important so we do not panic under stress and do stupid things.

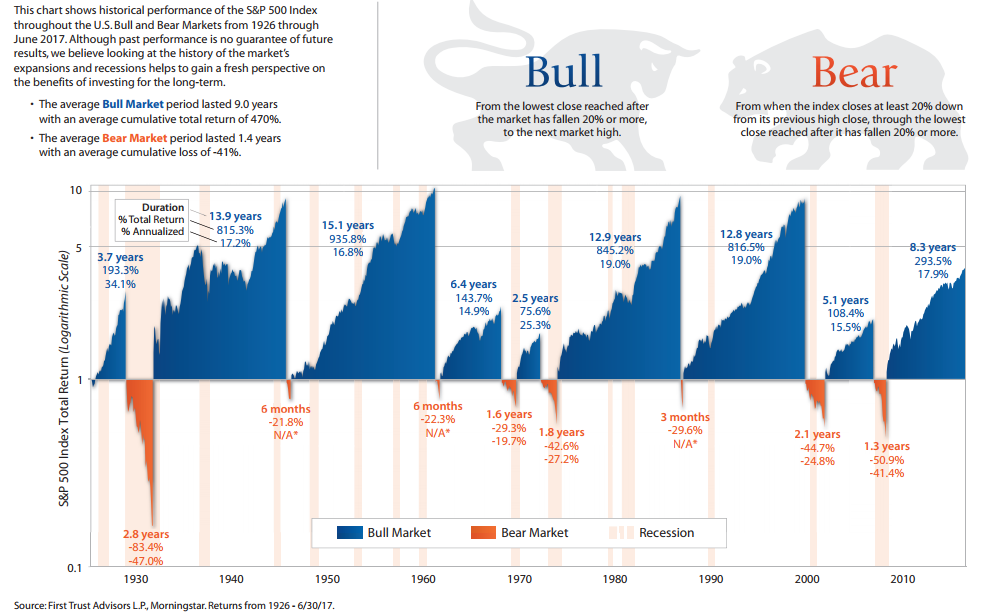

The following chart shows the SP500 bull and bear markets from 1926 to June 2017:

The stock market has had two bear markets over the past 20 years. Each time stocks lost more than half their value. Because of this, investors have been extra cautious. Many have tried to use broad diversification to reduce their portfolios’ drawdown exposure.

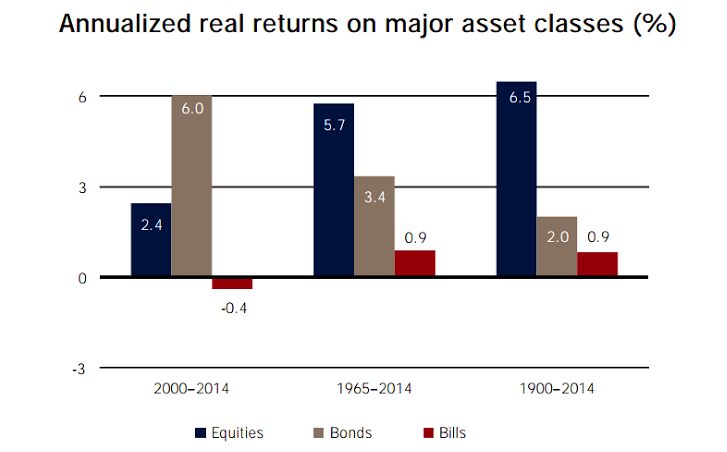

If you select non-correlated assets, you can achieve some reduction in volatility and drawdown. But your expected return is the weighted average return of all your assets. That is where the problem lies. Assets with lower expected returns will reduce your portfolio’s return.

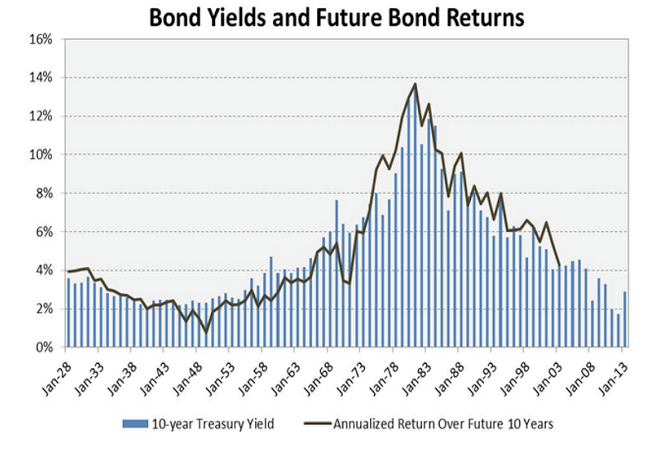

Bonds have done well over the past 15 years. But longer term, their real return is less than one-third the real return of stocks. Given how low interest rates are now, there is not much room for bonds to appreciate further. In fact, current interest rates predict low bond returns in the years ahead.

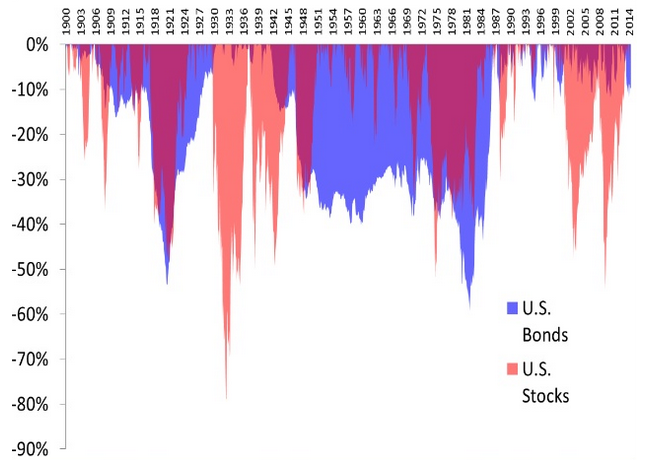

Bonds are also not as low-risk as you might think. Since 1900, the worst real return drawdown was 73% for stocks and 68% for bonds. As we see below, stocks and bonds can sometimes have severe drawdowns simultaneously:

Bonds not only create a drag on our performance. They also may not reduce our risk exposure when we most need them to do so. The same can be said for alternative assets, like commodities, where there is no guarantee that they will curb volatility. In my opinion, these are expensive solutions for the wrong problem: volatility is not risk and it’s not an issue; it’s part of trading and investing; it’s much more constructive to understand why a portfolio is volatile, why that will continue to happen and develop the temperament to not let emotions making a decision for you, rather trying to minimize it or eliminate it. Successful trading and investing is achieved by managing volatility, not eliminating it. Therefore, it all comes to what kind of trader / investor you want to be. Is your goal to limit the losses or to maximize the gains? You cannot have it both ways. Higher gains come with higher risk and inevitably will produce some big losers.

In the end, I believe this can be achieved by constructing a diversified portfolio, tailored for short term and long term gains (trading and investing), driven by different factors that have low correlation to each other, with assets focused in equities where we can receive more risk-premium, complemented by strategies with market timing that attempt to identify better asset classes according to economic factors and sector rotation.

Impatience

It is important to remain focused on what is important – accumulating wealth while managing risks. Once you have a defined trading (or investment) strategy, you need to be patient so it can do its work for you. It requires temperament to ignore the price gyrations which many times are illogical by being disconnected from fundamentals and it requires discipline to stick with the original plan and goal – even though at times it might feel that there’s little headway being made. On these cases, I always like to zoom out and see how that looks like in the grand scheme. “Every investor should be prepared financially and psychologically for the possibility of poor short-term results” – Benjamin Graham

Lack of confidence

Nowadays, saving is not enough to accumulate wealth. It’s important to invest (and / or trade) to grow the little that we can save. But we are constantly bombarded that this is usually difficult or impossible to do it, and that we shouldn’t bother with it. First, “In any sort of a contest – financial, mental, or physical – it’s an enormous advantage to have opponents who have been taught that it’s useless to even try.” – Warren Buffett. And second, companies that sell investment products and insurance products provide data, charts, graphs, and examples to support what they are selling. They understand how uninformed people are, how uncommitted to investing they are, and how easily that they are frightened by loss of their life savings, so they capitalize on it to market and sell their products during the accumulation phase and distribution phase (annuities, target date funds, indexes, funds, mutual funds, etc.). That’s why it’s so important to understand what a model or strategy is about, what are the concepts that explains why price should move and why temperament is paramount, since no one rings a bell before the market crashes (or when it starts to recover).

Expectations need to be set accordingly. Unfortunately, we are still very much exposed to big drawdowns (> 50%) even with market timing. Remember, these are backward-looking tests that address one particular type of market disaster. They cannot protect us from other kinds. The important point is that we can NEVER assume, based on a simulation, that we can be protected. This is not engineering. This is not physics. This is not medical research. Test results drawn from one group (for example, 1999-2017) do not tell us anything about what we can expect in a different group (2017 and beyond). That’s why it’s so important to learn and understand financial theory. Models need to be designed based on principles that transcend specific sample periods. The more you understand the rationale of a model, the more confidence and patience you’ll have to let it do its work – which is a lot easier to cope with if it’s part of a diversified portfolio, made of several strategies that are low correlated between each other.