Happy New Year!! Every year I review my current watchlist, to ensure that the businesses that I decided to partner with still meet my goals. This exercise has nothing to do with stock price performance. A decision to invest in these businesses (buy at sound valuation) or to wait and let important scenarios unfold before the next decision (hold) or to decide to cease the partnership (sell) should be solely considering the business itself, by evaluating if it still possess the ability to meet my original goals – and that’s based on the company’s operating performance, not on how the stock has performed.

My dividend growth investing portfolio has a mix of companies with a history of growing dividends mixed with companies that don’t grow dividends (but it pays one) which then I expect a decent capital appreciation, mixed with companies with a higher yield, which many times carries more risk than a conservative portfolio. Therefore, it’s expected that some of these companies might not perform well overtime or might come to a point that it won’t meet my goals any longer. At the same time, my complete portfolio also contains short term investing / trading strategies, which drives returns based on growth or income and have been able to nicely complement the dividend portfolio for the long run. Therefore, I believe that I can now improve the portfolio overall by reducing the exposure of the companies that are carrying more risk.

What about the recent volatility?

I care more about how my income will grow a year from now, not what my account balance will be. My primary goal is to build and grow my income by 6-8% a year so I don’t really care about the portfolio balance. In all fairness, a lower market actually helps me buy more shares and increase income even more.

Focus on dividend quality and growth of that dividend. When asked recently about how I was “holding up” given the moves in the market, I answered my portfolio income will increase year over year by 8.5%.

What happened to capital gains these recent months? It made a lot of people worried because they are thinking as sellers, not buyers. That worry is either emotional or rational, and it’s important to determine which one is the truth. If it’s emotional, (they know their investments is for the long term, they just don’t like seeing being down or they don’t like the volatility), then their portfolio is behaving as expected, and therefore, it’s just a matter of temperament (easier said than done), and that’s why I think it’s a lot easier to have the proper temperament as a dividend growth investor: those of us who think in terms of our investments providing cash flow (“organic income”) tend to worry less about issues like stock price decline. Cash flow is more predictable than stock prices because it’s heavily tied to operating performance of the businesses that we invest on. The fact is, your income from investments probably didn’t change a bit (or it went up) through the volatility of the past couple weeks – and that focus really help to stay on course.

Now, if someone is worried about the recent losses as a true rational concern, then they need to evaluate if they are either taking more risk than they should or if they are not considering the right time frame – because in the long term, their portfolio will be higher than today or 6 months ago or a year ago. Recessions and the economy is cyclical, they always come, get addressed, and prosperity continue for many years until the next one shows up – meanwhile, good quality businesses react, adapt and always emerge stronger producing higher earnings and cash flow – stock price follows that, so it’s only a matter of time for the whole portfolio to be making new highs again. The beauty of a portfolio focused on the growing stream of income is that it can endure these cyclical periods without being affected much – a diversified portfolio exposed to recession proof companies and sectors will continue to maintain and grow dividends while other sectors / companies might be more unstable – and that’s why the whole portfolio overall is still solid.

The key is the business cash flow (operating cash flow or adjusted funds from operations) for those of us who rely on dividends to replace or supplement our other sources of income.

Companies that no longer meet my goals for 2019:

No companies on my Canadian DGI Portfolio were removed for 2019. One company was acquired, so this was just a cleanup item for my watch list.

REITs:

REF.UN: More of a cleanup item here, Canadian Real Estate Investment Trust was acquired by Choice Properties (CHP.UN), so REF.UN was removed from my list. I continue to hold CHP.UN and I will wait a few more years to evaluate their operating results after the acquisition before I consider it to be part of my watchlist. I expect them to continue to perform well, given that Choice management kept most of CREIT management in place.

.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.

Companies that I decided to partner with:

Besides deciding on the companies that no longer meet my goals, I also evaluate once a year which new companies I should partner with. In order to facilitate this process, I decided to further automate the screening process so it does most of the quality screening work for me, allowing me to evaluate further on a smaller list for the companies that was suggested through my initial automated quantitative analysis.

Remember that this process solely speaks to what to buy, but it doesn’t determine when to buy (which needs to take valuation into account). Let’s go through the “what” now, and I’ll later elaborate some of the “when”. I decided to partner with the following business:

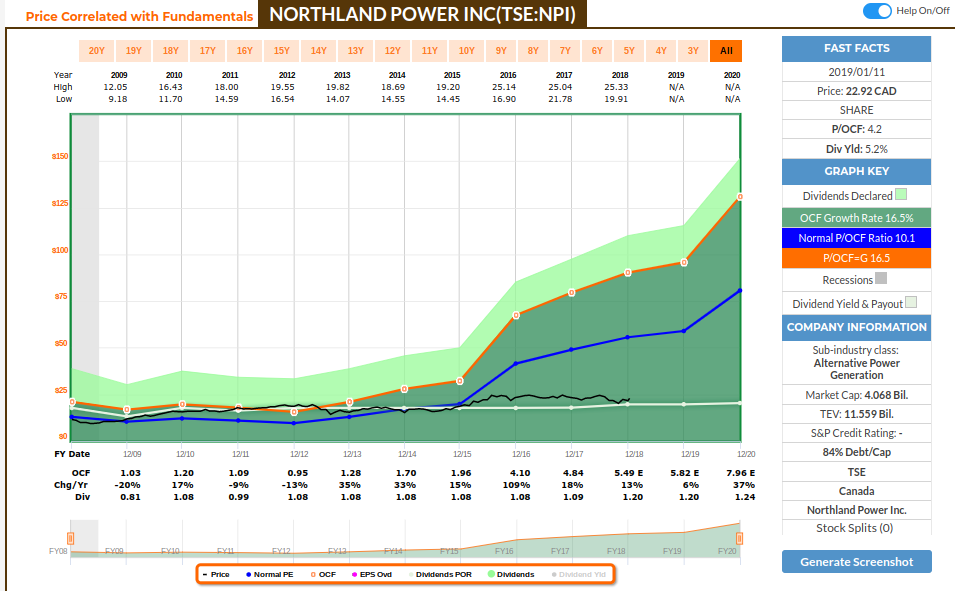

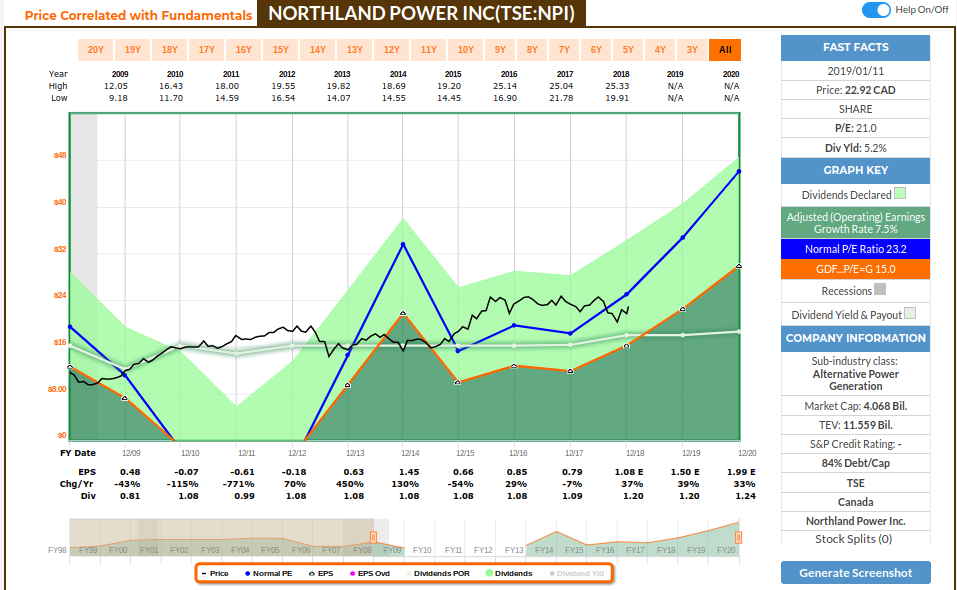

NPI: Northland Power Inc. develops, builds, owns, and operates green power projects primarily in Canada and Europe. It generates electricity from thermal, wind, solar, hydro, and biomass power plants. As of September 24, 2018, the company owned or had a net economic interest in power producing facilities with a total capacity of approximately 2,029 megawatts. The company was founded in 1987 and is headquartered in Toronto, Canada.

Operating Cash flow:

Adjusted Operating Earnings:

The companies that I bought this month:

The companies from my watchlist should be purchased when price is attractive, which is a process taking valuation (not price alone) into account. The watchlist speaks to “what” to buy. The valuation process speaks to “when” to buy.

For this month, I purchased the following companies. My last purchase was in October, and I typically save $2,000 per month, so that allowed me to save $6,000. Plus, I will be reinvesting the dividends from 2018 ($3,473.43), which will give me a total of $9,473.43 to be invested this month.

I chose 7 companies to either average down or start new positions, so I’ll be allocating $1,353.34 for each company. The investing performance spreadsheet has been updated accordingly, including the information related to the companies that increased dividends this year so far.

I’ve added positions / initiated new positions on the following stocks, allocating the amount specified above:

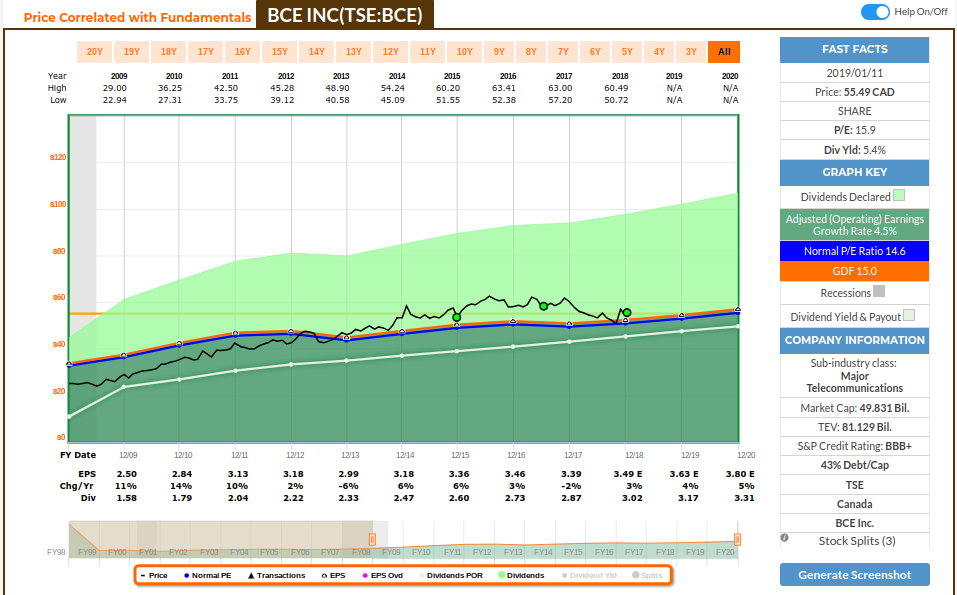

BCE Inc: I really like how stable, reliable and consistent is BCE operating cash flow and their dividend growth. They have a nice starting yield, a reasonable growth of that yield and a low and steady earnings growth rate. BCE is well position to continue growing its earnings and cash flow, having a solid and growing presence in the wireless space and aggressive plans on the wired space with their Fibre To The Premises offering, which should compete well with Rogers cable offerings. The recent price decline driven by market uncertainties and rise of interest rates presents a nice opportunity to add more of a solid company at a great valuation.

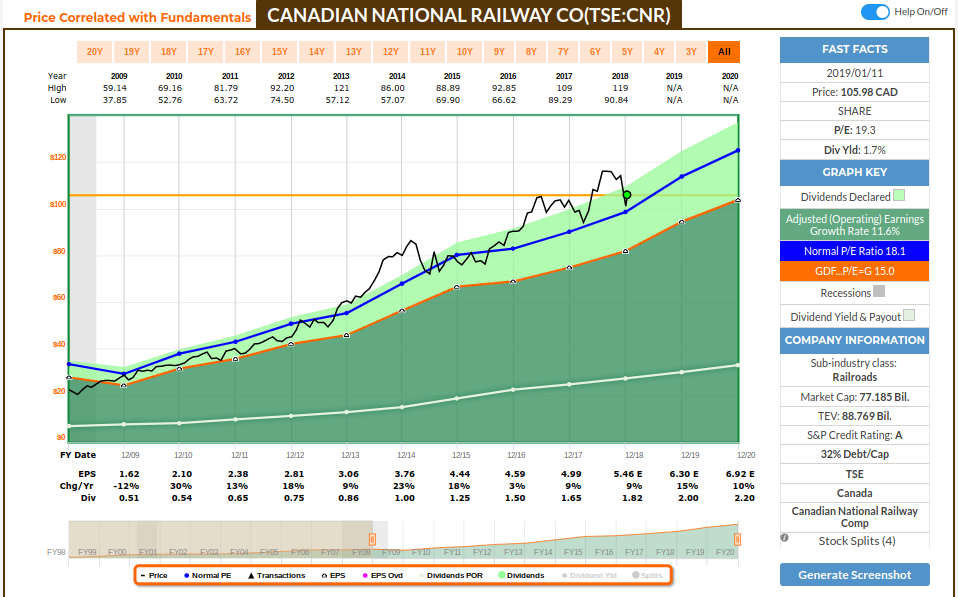

Canadian National Railway Co: This is one of the best managed company in Canada, great earnings track record, and very difficult to find it at a decent valuation. I missed an opportunity to buy last year, so I’m glad I could catch another one now. We can see, through the graph below, how price follows earnings, and how letting our emotions (greed or FOMO, how many calls it now) can turn a great company into a poor investment. Never overpaying is as important as finding good quality companies, and that’s what margin of safety is all about. Now, we can only work with the data that is in front of us. If CNR earnings declines from what it’s currently projected, this will look overbought in hindsight, but we’re making our decisions with the information that we have today to determine what the intrinsic value is today and what we expect to be a few years from now. Canada has only 2 major companies in the railway space, and volume rail is cyclical, with grains, fertilizer, coal and chemicals to grow and offset lower volumes by auto and lumber. CNR initial yield is low, but the growth of that income is decent, averaging 15% dividend increase in the last 10 years. Plus, CNR grows earnings at a much higher pace than other high yield companies, which helps to push the portfolio’s total return higher, if something needs to be liquidated in case of an unplanned big spend.

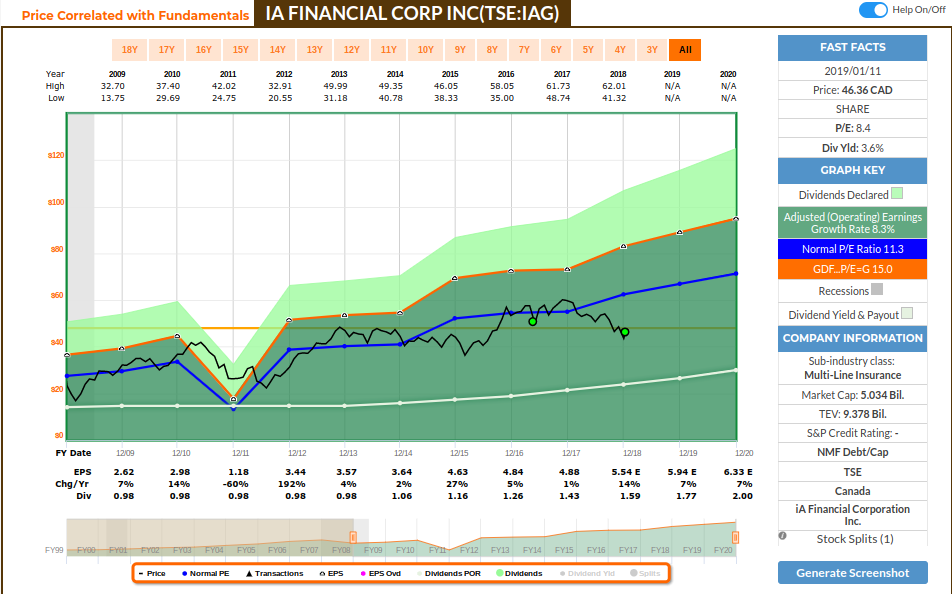

IA Financial Corp: I’m taking the opportunity of lower prices to average down my current position. Considering how IAG earnings are estimated to grow, the current price decline provides a decent yield. I believe that another factor that reinforces the present valuation is the recent announcement from IAG that it has entered into an automatic share repurchase plan under which its designated broker will repurchase the Corporation’s common shares pursuant to its previously announced normal-course issuer bid, commenced on November 12, 2018. The automatic plan, which has been pre-cleared by the TSX, will provide for the potential repurchase of common shares at any time, including when the Corporation ordinarily would not be active in the market due to its self-imposed trading blackout periods, insider trading rules, or otherwise. The NCIB is for 5% of the shares, and management stated that it’s a buyer at the current levels. The recent acquisitions should provide business synergies and reflect on earnings in the future.

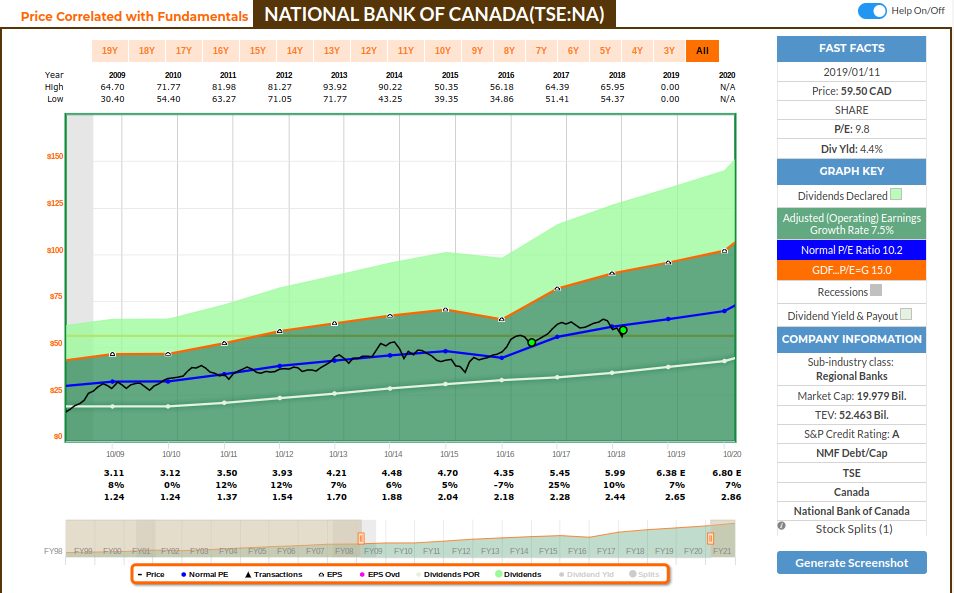

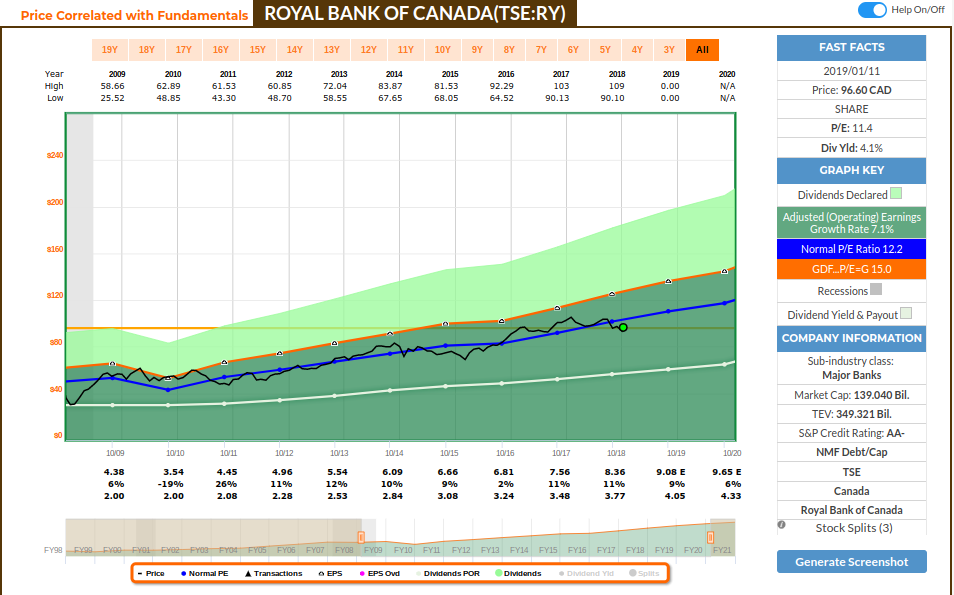

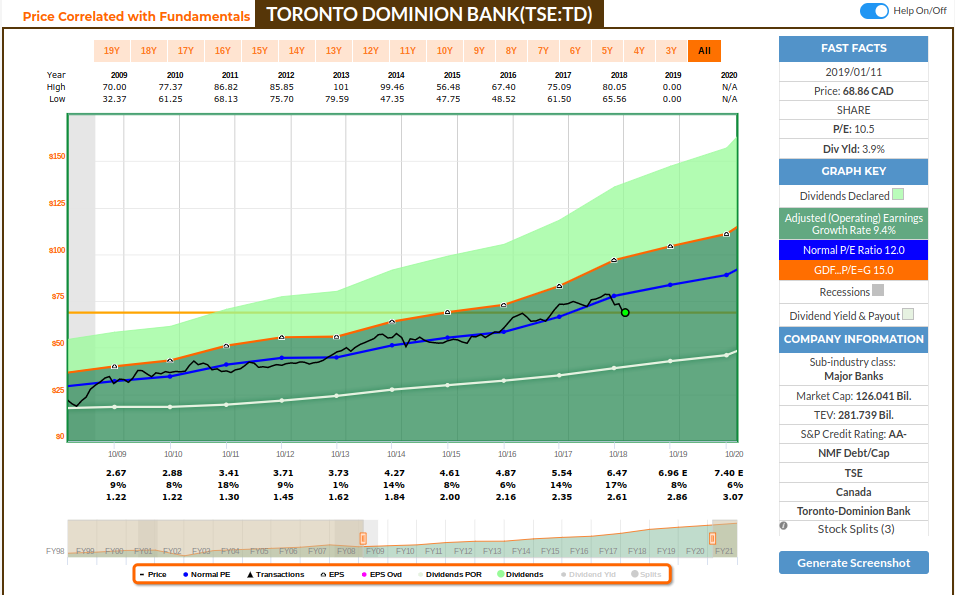

The following research shows how banks should be part of a core portfolio for anyone interested in Canadian equities. Bank moats are derived primarily from two sources: cost advantages and switching costs. Costs in the Canadian system is driven by a tightly regulated oligopolistic market structure that limits excess competition, thereby stabilizing product pricing and giving customers less incentive to switch banks. Cost advantages drive from three primary factors: a low-cost deposit base, excellent operating efficiency, and conservative underwriting, with regulatory costs being a final factor that must also be considered. The Canadian banking system allows lower operating costs, lower credit costs, lower regulatory costs, and better diversification of risks, all of which allow Canadian banks to achieve greater risk-adjusted returns.

Barriers to entry for the Canadian banking system are very high. Existing regulations prevent foreign competition, as non-Canadian residents may not own more than 25% of the shares of a bank unless approved by the government (preventing foreign takeover), and foreign banks can only operate in Canada under certain restrictions (preventing significant direct foreign competition). Domestic competition is also controlled, as Canada’s banking system historically developed to favor a few large banks controlling the majority of the domestic market, and this is actively enforced through the handling of chartering by the federal government exclusively. Additionally, the rejection of merger proposals in 1998 between Royal Bank of Canada and BMO and between Toronto Dominion and Canadian Imperial Bank of Commerce created a precedent where the regulators will accept no further consolidation between the main Canadian banks. Having larger banks helps to spread out fixed costs across a larger operating base, increasing operating efficiency, as the four largest Canadian banks are all bigger than the largest U.S. regional bank. Because their branch networks spread out through all of Canada, the Canadian banks arguably have some of the most powerful distribution networks in Canada. This offers cost advantages via lower customer acquisition costs. In addition, the banks are involved in nearly every major financial product, including asset management, wealth management, insurance, investment banking, and a variety of other consumer and commercial banking products and services. Bigger scale, powerful distribution networks, a multitude of products, and diversification of business lines lead to economies of scope in addition to the economies of scale already achieved.

The Canadian banking system enjoys a more protective and efficient regulatory system, which leads to cost advantages, primarily through risk reduction. Less fragmented and well-integrated banking systems, like the Canadian system, have tended

to be more stable over time, reducing risk. Also, the Canadian regulators must only primarily monitor and develop relationships with the Big Six Canadian banks, which is much easier than trying to monitor the thousands of banks that exist in the U.S., for example. This leads to more collaboration and cooperation between regulators and banks as well as greater institutional memory and better-coordinated and more easily implemented responses if strains begin to appear in the system. Regulators also help to control pricing in the market at times, such as with mortgage products, helping to reduce the potential for pricing wars to gain market share at the expense of underwriting standards. Canadian regulation also makes it more difficult for bad credit to be issued in many ways, including mandatory insurance and standards on riskier mortgage loans, not having a government-sponsored enterprise like the government-subsidized mortgage securitization market, and forcing banks to hold more of the risk on their own balance sheets. These factors help contribute to better absolute risk reduction in the system

as well as regulatory economies of scale.

The Canadian banks are also more geographically diversified on average than, for example, the majority of U.S. regional banks, which often have concentrations in individual states or local economies. This diversifies credit risk, lowering the overall risk for each individual bank. Canada’s system of higher taxes, social safety nets, and other complex factors have also led to a more robust and stable middle class, which contributes to economic and political stability, further reducing systemic risk.

With all of these factors combined, along with explicit government subsidies on deposit insurance and mortgage insurance, as well as the implicit subsidy of being too big to fail domestically (all of the Big Six Canadian banks are labeled as domestic systematically important banks), Canadian banks have a good environment to continue growing earnings and dividends.

Obviously every investment comes with risks. In case of banks, they are mostly exposed to credit and debt cycles, and 2008 is good example of what the damage that the cycle can make. We can’t do anything about that, hence my approach to track operating results as management is well paid to deal with that. A lot of macroeconomic factors is beyond control of management, so temperament is also required to wait that down cycle to finish to see how management reacts and adapts.

I purchased the following banks:

National Bank: National Bank is positioned for a decent growth moving forward, has a decent initial yield and it’s presently at an attractive valuation. I like NA compared to the other banks given its core exposure on the Canadian market (mostly a niche in Quebec) and how it provides a natural hedge compared to other banks by having the lower exposure to the housing market. NA has a decent tracking record of earnings on tangible equity, which is estimated to continue strong.

Royal Bank of Canada: Royal Bank, the biggest Canadian bank, is also trading at a good valuation, offering a decent initial yield, with earnings and dividends estimated to continue to grow. Royal Bank is well diversified and their line of businesses are well managed and position to grow and deliver solid results.

Toronto Dominion Bank: TD Bank has great exposure to the US environment, which continues to enjoy solid economic growth. The recent price decline also provides a good starting yield, and with earnings and dividends estimated to continue to grow, it provides a good valuation at this point.

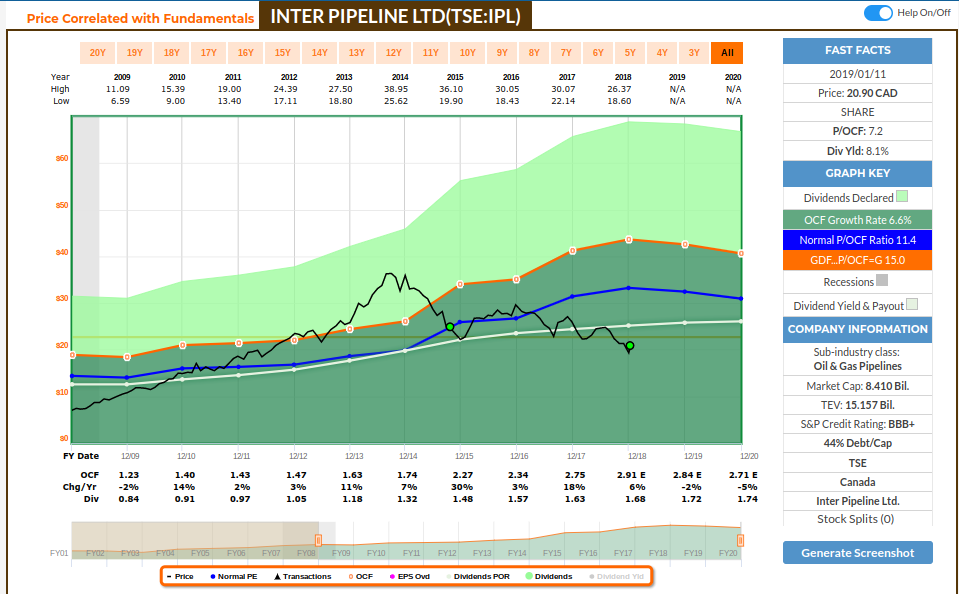

Inter Pipeline: I took the recent price decline to average down on my current position. IPL enjoys stable cash flows

regardless of the commodity price environment due to the long-term cost-of-service contracts on the oil sands

infrastructure, and IPL’s overbuild strategy for its oil sands pipeline infrastructure allows them to benefit from projected oil sands production growth with minimal capital investments. The present high yield is a great advantage, while IPL maintains a

comfortable distributable cash coverage ratio that averages 1.8 times. The graph below shows how dividends can continue to increase in a sustainable way, as operating cash flow is more than enough to cover it. Cash flow is estimated to decline in the short future due to the planned investments on what drives about 30% of their earnings: approximately CAD 3.5 billion on the chemical facilities over the next three years. IPL will have 70% of earnings coming from growth of their main portfolio, which focus on the increase of the guaranteed long-term contracts, and about 30% of earnings focused to expanding its NGL

infrastructure and venturing into chemical operations, which exposes them to volumetric and commodity price oscillation and risk.

On my next post, I’ll elaborate on the review of my DGI Portfolio for US companies.

Happy Investing!

Rod, thanks for update and especially the FastGraphs.

Did you partner with/buy NPI and can you help me understand the difference between Operating Cash Flow & Adjusted Operating Earnings?

Also I thought for Utilities, DCF was the best indicator?

Thanks and also bought IAG on Feb 3 based on your work.

Happy to share my findings. NPI is now on my watchlist, and I’ll start a position as soon as I buy some other companies that are waiting on my queue, mostly railroads, which are trading at a nice valuation. But NPI is a buy for me now.

Regarding earnings and cash flow: It’s important to understand the metrics used for each sector and companies, and how the market price these companies according to these metrics. Simply stated, operating earnings refers to how much profit the business generated in a period. Operating cash flow measures the amount of cash generated by a company’s normal business operations. Earnings is about profitability, as typically stock price follows earnings in the long term. Operating cash flow indicates whether a company can generate sufficient positive cash flow to maintain and grow its operations. For capital intensive companies, it’s an important metric to determine liquidity.

DCF works well for most utility companies, but NPI is not a typical utility company. Most utility companies are setup as operators, which means they generate, transmit and distribute electricity. NPI is an independent power producer, so it develops, builds, owns and operates green power projects. I use operating cash flow to evaluate NPI because if you look at their income statement, there are several items that skews earnings compared to a regular utility company, given NPI’s capital structure. Also, management typically reports EBITDA and AFFO as the measures for growth and success. I find more reliable to determine valuation using operating cash flow.

NPI is growing nicely, they are currently expand their wind offering in Germany, and there’s a big project in progress in Taiwan. As new contracts are signed, since these are typically very long term contracts, it will produce additional cash flow, so I expect dividends to be increased as new contracts are signed off.

Are the returns posted somewhere? This portfolio/approach is going on its 5th year if I’m not mistaken. It would be helpful to see how it has performed over the years since inception.

Hi Walter,

That’s a fair comment, and I agree that it’s a bit confusing gathering that info because the initial portfolio was tracked on 2 different tools before getting tracked on the current spreadsheet. All the info is available via the posts and tons of discussions on RFD, but it’s not centralized anywhere.

I will write a new post with a review since the ports started 5 years ago and will consolidate all performance information in there.

Stay tuned!

Just wanted to chime in to say i’d very much interested in/looking forward to seeing this. While you stress your not seeking capital gains and prioritize income I still think its important/valid to compare total returns of any strategy against a benchmark.

Right, and this is why I’ll gather not only the dividend increases, but also the total return performance (which includes capital gains) per year since it started around 5 years ago. However, I’m not a fan of comparing to a benchmark, because I haven’t found an equivalent benchmark to compare with my strategy. Comparing to an index is misleading, because the companies that form the index enter and exit the index based on market cap (not on quality and valuation), and many companies from the index don’t pay dividends. A few factor-based ETFs might be closer to this strategy (and could be a better benchmark), but again, they don’t share the same goals as my strategy: they attempt to minimize drawdown (which is one of the factor-based components), and they are pressured to have some profits in the short term, while this strategy doesn’t care for drawdowns (time is on our side to let investments recover and grow) nor to lock profits in the short term (selling is not a goal, and to be fair, the goal is also to not lock any profit ever, and remain invested if the company behind the stock continues delivering the objectives of producing a perpetual growing income).

Nevertheless, it’s a fair ask and I will post that soon.

Rod

Any thoughts on Saputo and Suncor?

I used to hold Suncor, but I sold in 2018 as at that time dividends were not estimated to grow in 2019 (at that time), I had other companies exposed to that sector and capital could be deployed elsewhere. However, dividends are estimated to grow (as of today’s forecast), and operating cash flow is estimated to grow. They’ve endured the last crisis well, and have a decent history of resiliency regarding dividends and cash flow, although stock price is very cyclical. I’d say that Suncor is fairly valued today. I like Saputo, but it’s been very overvalued since 2016. Price is becoming more reasonable now, considering how earnings are estimated to grow, and I will probably add on my next purchase next month. They had a few setbacks this year and earnings are estimated to decline for FY19 (their fiscal year ends at end of March), but FY20 looks promising.

Thanks!

Thank you so much for posting this. Will you be reviewing your US portfolio too? Do you deal with international stocks (i.e. not Canadian or US)?

Yes, I will be posting a review for my US DGI Portfolio soon.

I only invest in companies listed on Canadian and US exchanges. There are a few companies that are from Europe in my portfolio, and I hold them because they are listed on US Exchanges. Reason being is the ability to get fundamentals data using the same method I apply for the other companies. Also, I’m not well versed on how other exchanges operate and if they are as strict as TSX or NYSE or Nasdaq. Lastly, companies from other exchanges would bring currency exposure risks. For these reasons, I’m comfortable staying with companies listed on Canadian and US exchanges, there are a lot of options to choose from these supermarket of stocks.