On the Canadian side, in order to average down and get juicer dividends, I’m adding more Enbridge and Enbridge Income Fund.

Enbridge Inc. (ENB.TO) is a leading North American oil and gas pipeline, gas processing and natural gas distribution company.

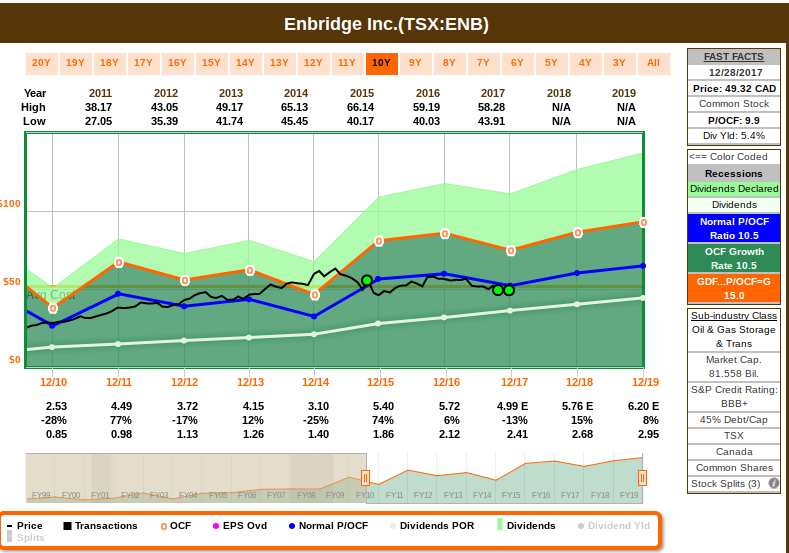

I believe ENB is fairly valued, see how price (black line) tracks with its typical price to operating cash flow ratio (blue line):

For midstream / pipeline companies (like ENB, ENF, PPL, IPL), you want to evaluate price to cash flow. Dividends are typically higher, but how do you know they are sustainable? By comparing it to cash flow (white line above), which clearly shows that it’s sustainable – the white line would have to be the same or higher than the orange line (operating cash flow) to be in danger, since the company would pay more than its cash flow. If you compare the dividend payout ratio to earnings, it always look like that dividend payout ratio is dangerously high. That’s because earnings / EPS is a poor measure to evaluate these type of companies, due to high non-cash depreciation expenses, such as the capital intensity of building and maintaining all of its pipelines and terminals. Look how DD&A metric (depreciation, depletion and amortization expenses) impact earnings. Hence a better valuation metric for midstream companies are cash flow, precisely available cash flow from operations (ACFFO). It measures how much net cash the company is bringing in, minus any preferred dividends and maintenance capital. Therefore, it is a solid measure of how much cash flow the company has remaining to pay its dividend and to invest in growth projects.

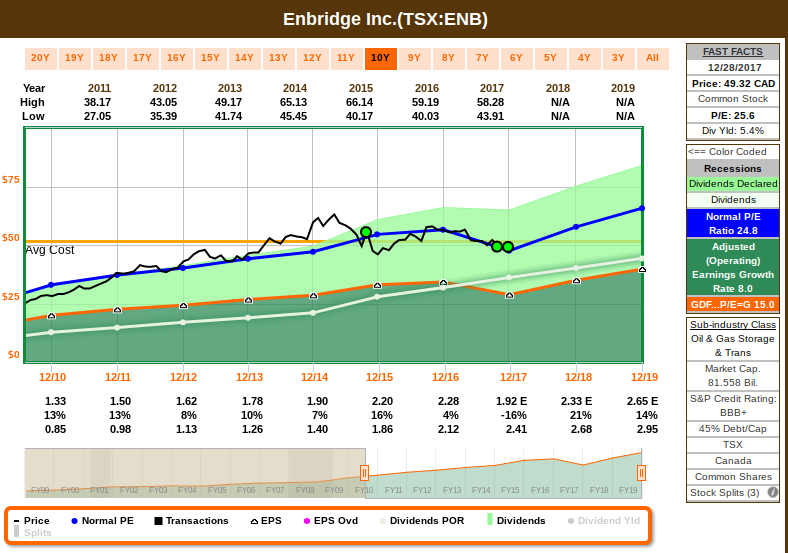

Below is Enbridge’s valuation graph using P/E instead of P/OCF. See how stock price follows earnings, and how dividends (white line) can be mis-interpreted to not be sustainable:

Enbridge just had their Investors Day on December 13th, and in that presentation they provided detail about deleveraging (by switching to a pre-financing / funding program instead of keep borrowing, which in turn will ensure their credit metrics); this gives room for Enbridge to pursue small to medium initiatives and when it comes to large ones, funding will be procured first; 2018 guidance for EBITDA and ACFFO was confirmed, which details that included a $3B asset sales and synergies on Spectra acquisition. The solid outlook for the Liquids Pipelines segment shows how strong the Canadian Mainline and Lakehead systems are, which together contribute to approximately 60% of EBITDA segment.

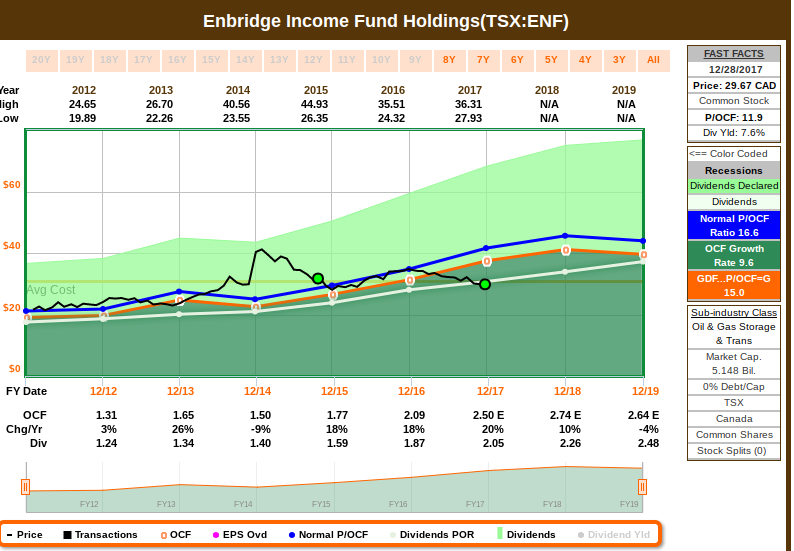

Enbridge Income Fund (ENF.TO) is a holding company for an approximate 10% economic interest in Enbridge Income Fund (the Fund), with the remainder owned by Enbridge Inc. The Fund’s assets include: liquids pipelines and storage assets, gas transportation assets (50% of Alliance), and renewable power assets.

I believe ENF is fairly valued, given how price is tracking to cash flow and growth estimates improved after last Investor’s Day last week:

Earnings are estimated to grow, which also makes this a case of stock price disconnected from fundamentals:

During last Investor’s Day presentation (Dec 13), management improved ACFFO guidance ($2.45B to $2.65B), which is higher than prior market consensus ($2.1B). This is mainly due to the Canadian Mainline, which will benefit from higher volumes and tolls. A flat rate base on the Lakehead system combined with higher volumes reduce its toll, resulting in a greater portion of the International Joint toll being attributed to the Canadian residual toll. Volumes are also expected to be strong, aided by demand and system optimizations.

On the US side, I’m starting a position with Chevron (CVX) and Disney (DIS):

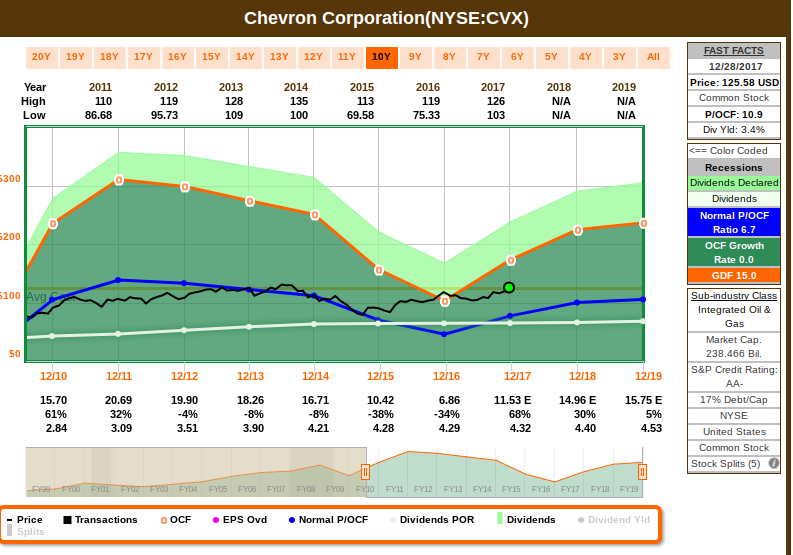

Chevron Corporation (CVX) manages its investments in subsidiaries and affiliates, and provides administrative, financial, management and technology support to the United States and international subsidiaries that engage in integrated energy and chemicals operations. The Company operates through two business segments: Upstream and Downstream. Upstream operations consist primarily of exploring for, developing and producing crude oil and natural gas; liquefaction, transportation and regasification associated with liquefied natural gas; transporting crude oil by international oil export pipelines; processing, transporting, storage and marketing of natural gas, and a gas-to-liquids plant. Downstream operations consist primarily of refining of crude oil into petroleum products; marketing of crude oil and refined products; transporting of crude oil and refined products, and manufacturing and marketing of commodity petrochemicals.

Chevron, like other companies on the upstream and downstream businesses, are cyclical and volatile, but I believe Chevron isn’t too stretched given the strong FCF recovery and the robust estimates for FY18:

My portfolio had XOM on the Energy sector so far, and I think this adds a nice competition within in that sector. Chevron reported decent results last quarter, with milestones like NG startup at Wheatstone and Gorgon at full economic capacity, and the focus now is to switch from construction to operation. Management also confirmed that they are able to grow production with lower oil prices, just from the shale, and that was positive.

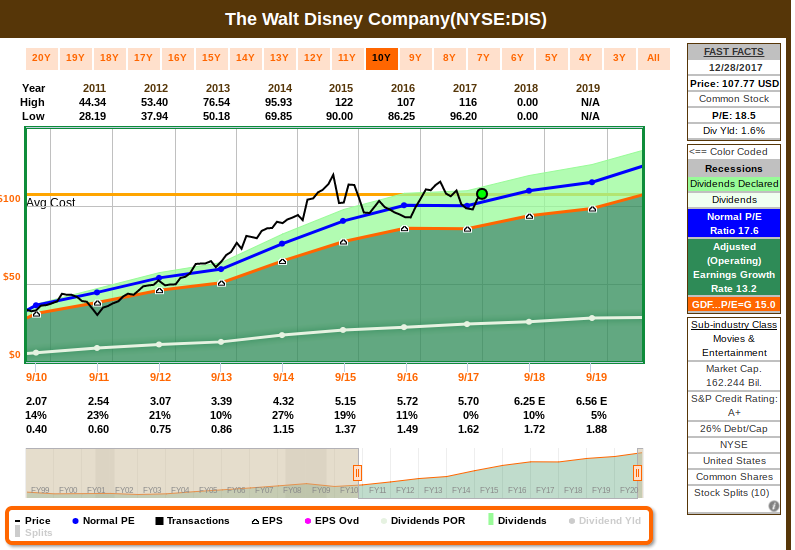

The Walt Disney Company (DIS) is an entertainment company. The Company operates in four business segments: Media Networks, Parks and Resorts, Studio Entertainment, and Consumer Products & Interactive Media. The media networks segment includes cable and broadcast television networks, television production and distribution operations, domestic television stations, and radio networks and stations. Under the Parks and Resorts segment, the Company’s Walt Disney Imagineering unit designs and develops new theme park concepts and attractions, as well as resort properties. The studio entertainment segment produces and acquires live-action and animated motion pictures, direct-to-video content, musical recordings and live stage plays. It also develops and publishes games, primarily for mobile platforms, books, magazines and comic books. The Company distributes merchandise directly through retail, online and wholesale businesses. Its cable networks consist of ESPN, the Disney Channels and Freeform.

I believe Disney is fairly valued:

Fox and Disney announced that Disney will purchase the entertainment assets of Fox for $52.4 billion in stock plus the assumption of $13.7 billion in net debt from Fox. Fox shareholders will receive 0.2745 Disney shares in exchange for these assets, and will retain their current shares of Fox and its remaining assets – the deal is pending regulatory approval. Disney is purchasing the Fox television and movie studios, cable entertainment networks including FX, regional sports networks, its 30% stake in Hulu, and the international assets including 39% of Sky. Fox would continue to own the broadcast network, Fox News, FS1, the Big 10 network, and its owned and operated local affiliates.

Disney posted a slightly weaker-than-expected fiscal fourth quarter due to the impact of the hurricanes and a valuation adjustment at BAMTech. The company’s strong fiscal 2018 film slate began with a bang as Thor: Ragnarok earned over $122 million in its opening weekend in the U.S. and has already grossed over $500 million globally. Management announced that there will be a new Star Wars movie trilogy, helmed by Episode VIII director Rian Johnson.

Revenue for the quarter fell 3% year on year to $12.8 billion. Media networks revenue dropped by 3% as the 11% decline at the broadcasting segment more than offset the flat quarter at cable networks. Affiliate fee revenue was up 4% in the quarter with growth at both cable and broadcasting. Disney has about 50% of its subscriber base up for renewal by the end of 2019. Parks and resorts growth of 6% reflected the growth at both Shanghai and Paris which more than offset the hurricane impact on domestic operations. Management disclosed that capital expenditures would be $1 billion higher in fiscal 2018 as company looks to complete the Toy Story Lands in Shanghai and Orlando as well as the buildouts of the two Star Wars Lands. The 21% revenue decline at the studio was due to the weaker performance of Cars 3 in the quarter versus Finding Dory last year. EBITDA for the firm fell 11% to $2.8 billion due in part to lower revenue along with increased marketing and programming costs.

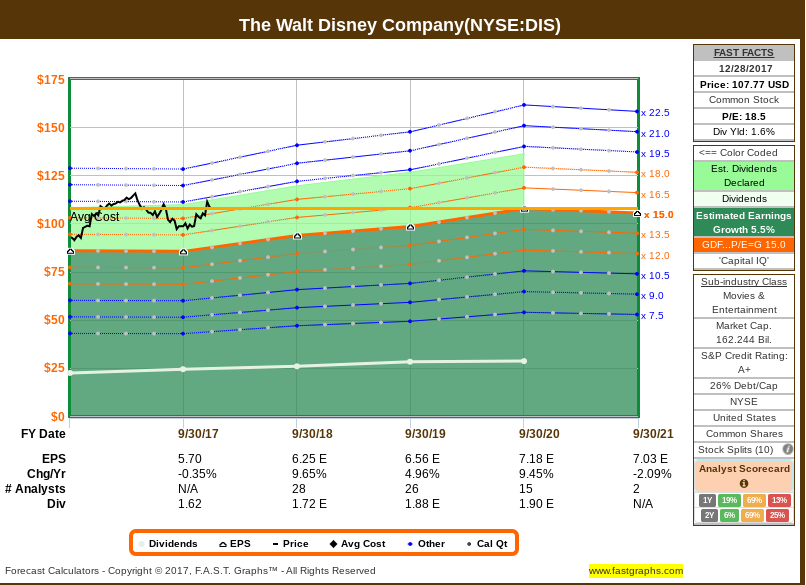

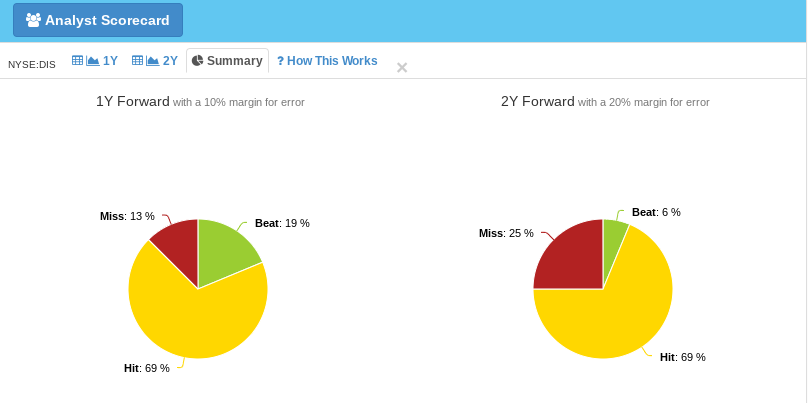

However, I believe Disney is setup for a decent growth, with several segments performing well, and the acquisition (largely expected by the street to go through) will provide further synergies for growth and cost savings. Dividends and earnings are estimated to grow by a large consensus, while keeping a decent tracking record on estimates vs results:

I will review my watchlist and post my comments in a few weeks. I wish you a happy, healthy and profitable 2018!