Following my monthly posts on what dividend stocks to buy for both Canadian and US Exchanges, below are the rationale to what stocks got added to my portfolio this month, and why.

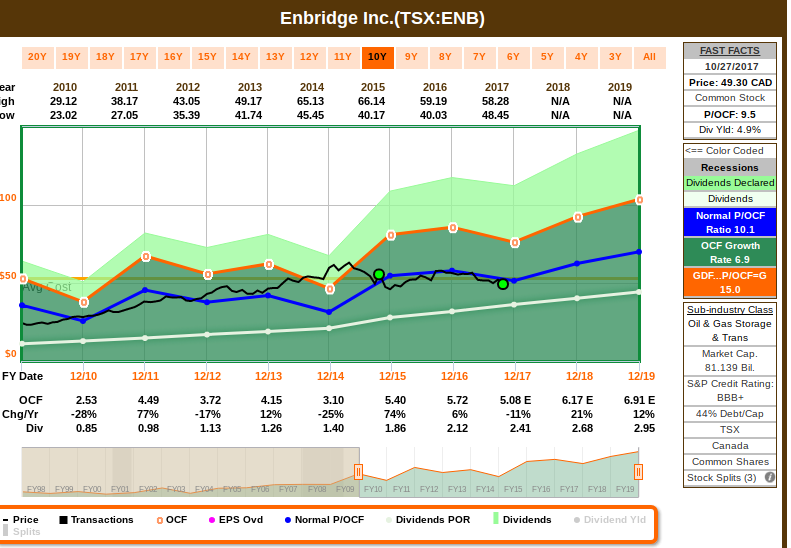

The first addition is regarding Enbridge, and the current valuation is a good opportunity to average down my cost. Enbridge stock price typically follows cash flow, and I believe at this point it’s fairly valued and estimated to grow – the lower price gives a decent 4.9% yield:

Enbridge will be reporting results on November 2nd, and their Annual Investment Community Conference is on December 12, which will have more information regarding revising guidance and results. Enbridge (and Michigan’s DTE Energy Co) recently announced their plan to complete their $2 billion Nexus natural gas pipeline from Ohio to Ontario late in the third quarter of 2018, as they just got approval from the U.S. Federal Energy Regulatory Commission to start construction. Once complete, it will move up to 1.5 billion cubic feet per day of gas from the Marcellus and Utica shale formation in Ohio, Pennsylvania and West Virginia to the U.S. Midwest and eastern Canada (for reference, one bcfd is enough gas to supply about 5 million U.S. homes). The approval keeps the project on track to meet its targeted in-service late in the third quarter of 2018, which is likely to be highlighted on the next earnings call. Enbridge said the pipeline would support growing demand for gas in the U.S. Midwest and eastern Canada and help offset the decline in traditional western Canadian supplies available to service the markets.

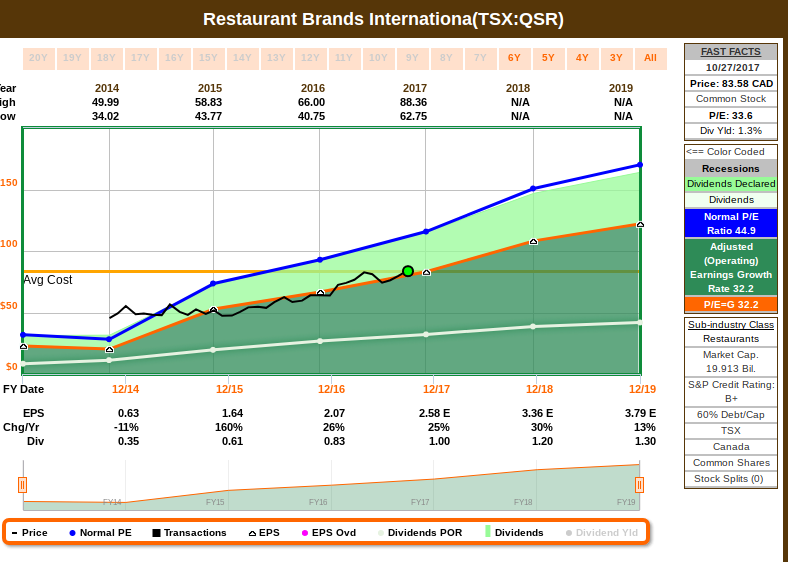

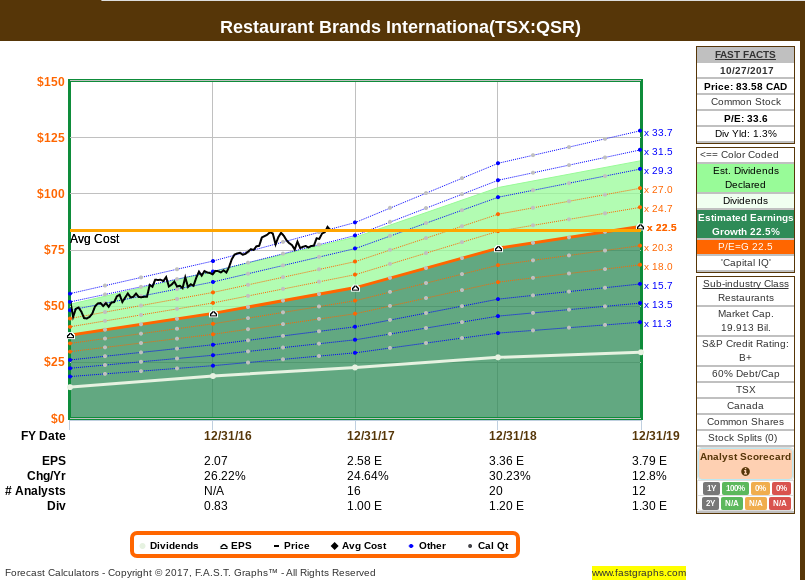

I’m also initiating a new position with Restaurant Brands International. Since Burger King bought them, I’m seeing them as a growth stock, with the added benefit of growing dividends. The reason I consider it a growth stock is the high estimated earnings growth rate:

Market consensus is reliable with a high number of analysts covering this company, and beating expectations since it was acquired by Burger King recently:

The downside is obviously the risks associated with any growth stocks that are highly antecipated to continue to grow aggressively: as soon as the growth slows down, it tends to be harshly penalized by having the stock price dropping way more than it should. However, I see that as an opportunity to get more provided that fundamentals are in place. We always need to determine if the issue is about this company having a growth problem (weak fundamentals) or if the issue is analysts disappointed that the company didn’t grow as much as they thought it should (unrelated to fundamentals, just a mis-alignment on sentiment). However, last quarter results were excellent, showing the synergy benefits of BK acquisition on cost control and great growth tracking record.

QSR is much more than Burger King managing Tim Hortons – Restaurant Brands International is one of the world’s largest quick-service restaurant companies with over 23,000 restaurants (under the Burger King, Tim Hortons and Popeyes brands) in aproximately 100 countries. From a business model perspective, RBI collects rent and royalties from Burger King, Tim Hortons and Popeyes franchisees, essentially taking a cut of sales, without having to manage operations.

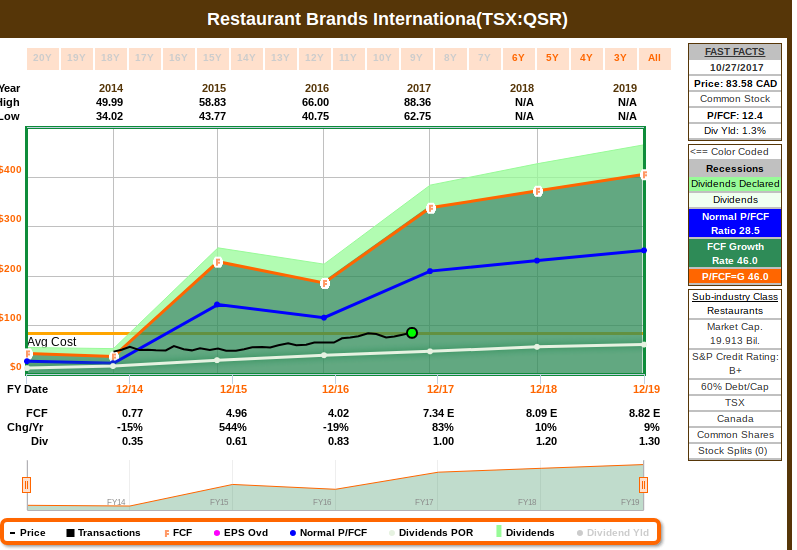

Furthermore, the growing free cash flow is a healthy indication that they can continue raising dividends steady while growing the business under the royalty model:

On the US side, I’m taking a similar approach than the Canadian side: Averaging down an existing position that is even better from a valuation perspective, and initiating a new position.

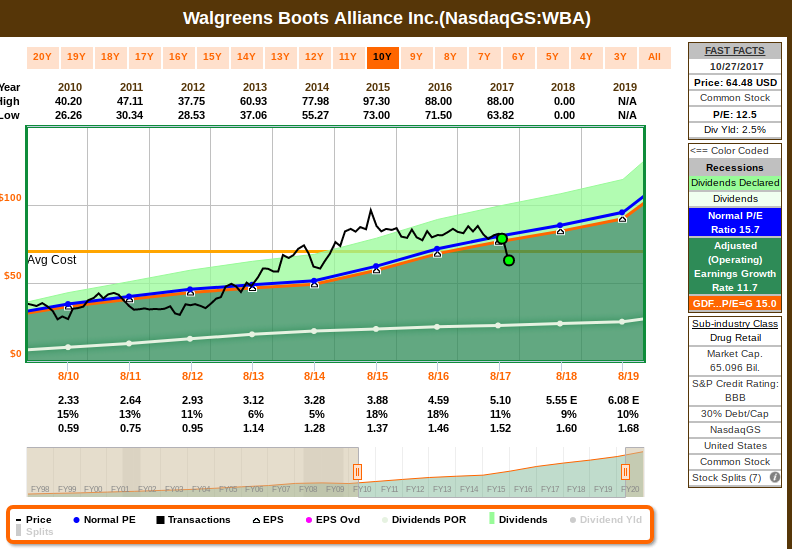

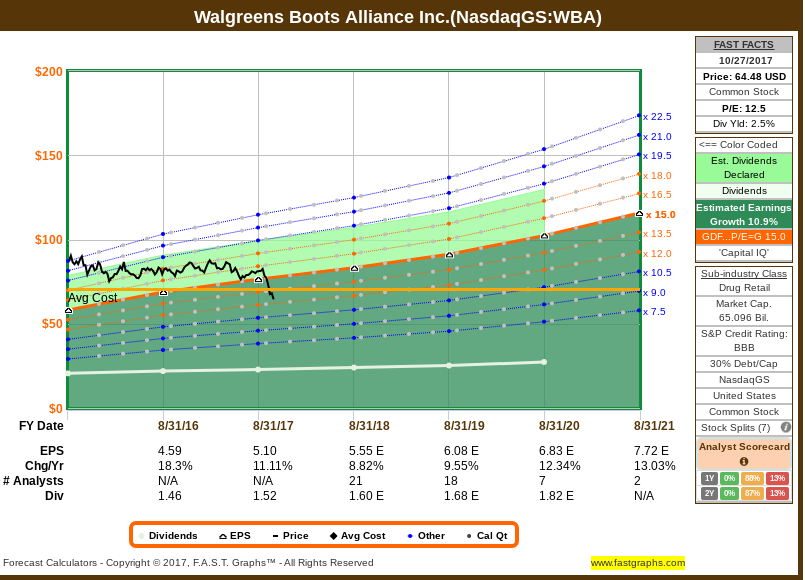

I’m adding more Wallgreens, which in my opinion had an over-reaction in stock price decline that is disconnected from fundamentals:

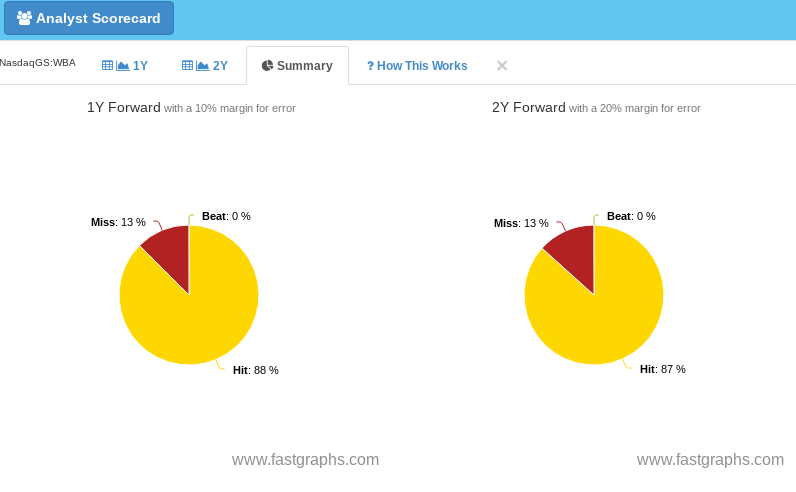

Earnings and cash flow have been growing and are estimated to grow, despite Amazon’s intention to enter at this space. There is a healthy market consensus with a broad number of firms covering this business, and a very good understanding of their business model given the tracking record on analyst results, which makes me think that WBA has the ability to react and adapt to competition:

WBA recently reported great results, beating earnings and revenue estimates, as the company filled millions of more drug prescriptions thanks to newly won contracts from pharmacy benefit managers. Walgreens, which in June scrapped plans to buy fellow pharmacy company Rite Aid Corp after a two-year long wait for regulatory approval, has been under pressure from investors to grow drugstore sales faster. Big contracts from pharmacy benefit managers have helped allay some of those concerns and helped Walgreens boost revenue in its latest quarter. WBA last year snatched a contract from larger rival CVS Health Corp to fill prescriptions for Tricare, a Department of Defense healthcare program, and for customers of Prime Therapeutics, a Minnesota-based pharmacy benefit manager. Tricare brought about 9.7 million new members to Walgreens, while Prime Therapeutics added 22 million. Walgreens also formed a venture with Prime, called AllianceRX Walgreens Prime, to handle mail orders and specialty prescriptions for their combined customers – and this formation was the main driver for prescription volume results.

Walgreens also said it would review its U.S. stores network, following its acquisition of nearly 2,000 Rite Aid Corp drugstores. The company expects the review to bring savings of about $300 million each year through 2020. Still, Walgreens also expects to spend $750 million on acquisition costs and another $500 million on store conversions and refurbishing. The impact of Hurricane Maria in Puerto Rico, where Walgreens is the largest drugstore chain, would reduce current-quarter profit by $90 million, as per statement during the earnings call.

Walgreens also said it expects 2018 adjusted earnings of $5.40 to $5.70 per share (which is above analyst expectations). Revenue rose 5.3 percent to $30.15 billion in the fourth quarter, topping analysts’ expectations of $29.93 billion. Net income attributable to Walgreens fell 22 percent to $802 million, hurt mainly by the $325 million termination fee it paid Rite Aid after their failed merger. Excluding one-time items, the company earned $1.31 per share, beating analysts’ expectations of $1.21. I believe Walgreens is nicely positioned to grow and the current price is a good opportunity to add more.

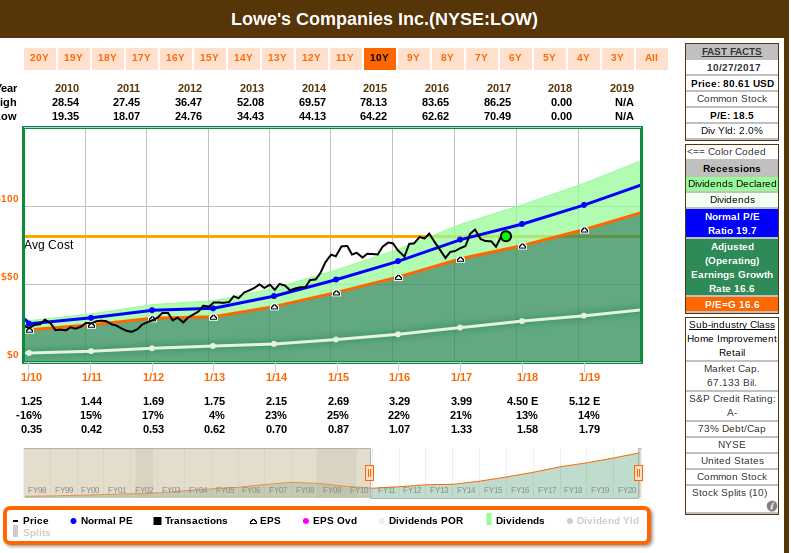

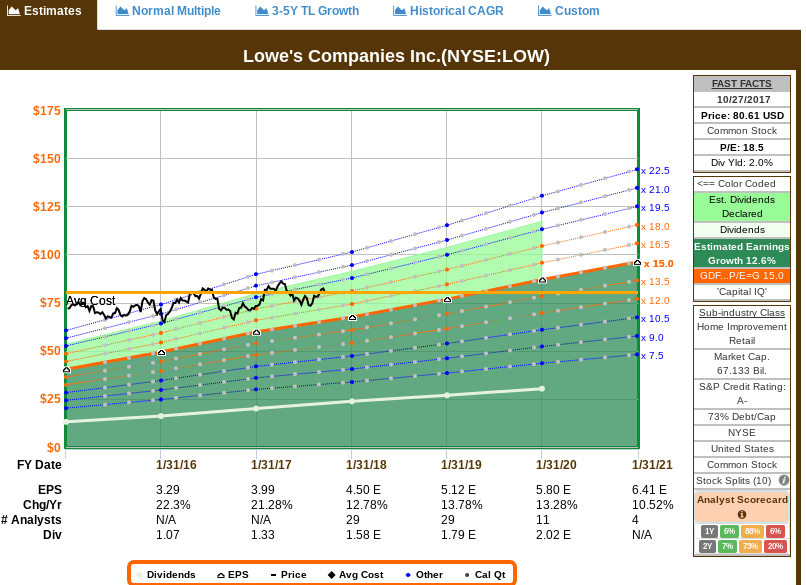

I’m also initiating a position with Lowe’s, as it’s positioned for decent growth of earnings and dividends, and it’s currently fairly valued:

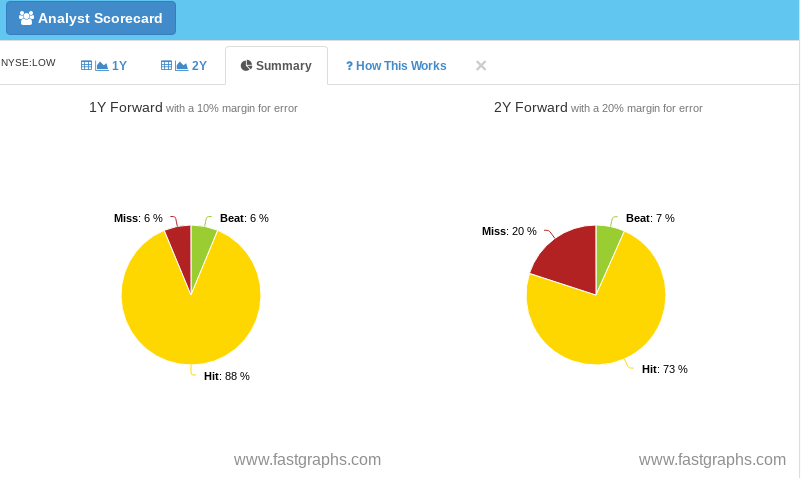

There is a good number of analysts covering this business, which provides a good market consensus on estimates, with a good understanding of how this business operates:

Lowe’s will report earnings on November 21 and the expectation is to maintain or improve 2019 guidance which has been provided last quarter. Lowe’s is the second-largest home-improvement retailer in the world, with annual revenue of $65 billion, and has established itself as a solid operator over time. Management has set detailed financial goals for 2019, including operating margins of 11.2% and returns on invested capital of 22%. This implies at least 50 basis points of operating margin expansion on average between

2017-2019, a pace Lowe’s has been able to more closely capture over the last five years through improving efficiencies. I believe that current valuation provides a nice entry opportunity in a sector where many quality holdings are overvalued.