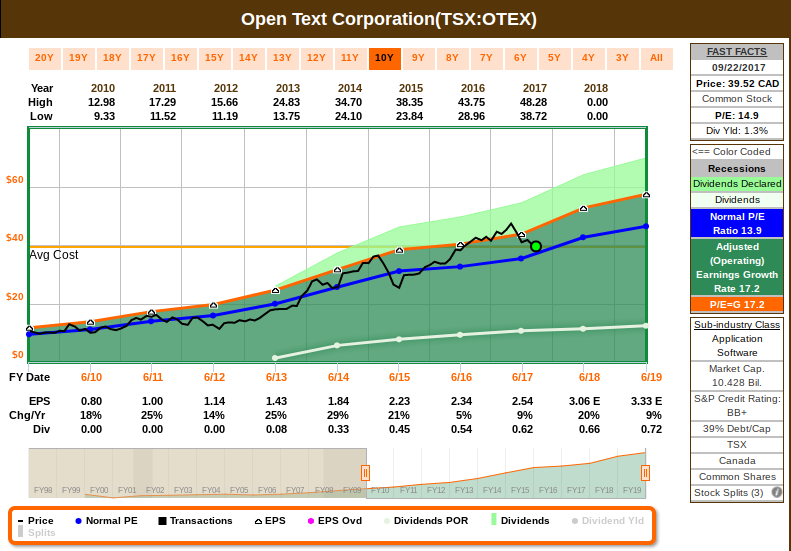

On the Canadian side, I’ll be adding more OpenText. The stock is trading is what I believe to be fair valuation, and earnings and dividend growth estimates are looking decent:

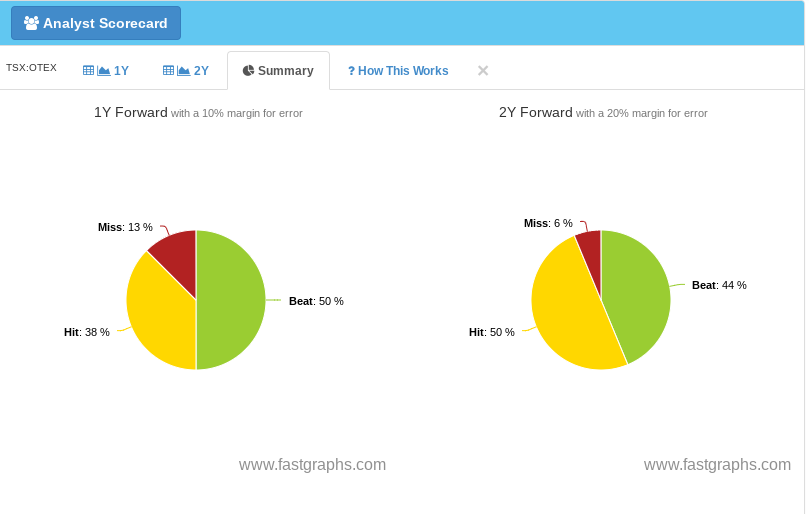

There is little institutional coverage, so not much of market consensus, but the firms covering this company seems to have a good understanding of their business:

OTEX’s FY17 Annual Report just came out, and the results were very good. Total annual recurring revenue has been growing steady and they will continue to deploy their excess free cash flow to make acquisitions. OTEX has a successful track record of 57 closed acquisitions. In FY17, OTEX focused on integrating five acquisitions, ANX, HP CEM, Recommind, HP CCM, and the enterprise content division of Dell-EMC (ECD). The acquisition of ECD was the largest in OpenText’s history, transforming the Company into being the #1 in the ECM space, with a strengthened competitive position in a number of markets (healthcare, life sciences and public sector). More acquisitions will continue in FY18. This goes on top of generating crossselling opportunities (managed services, analytics, etc.), like OTEX’s predictive analytics / AI product, Magellan, which is now shipping. OTEX is already the largest independent EIM software vendor. OTEX has a broad range of EIM solutions which it sells both directly and through a number of partnership arrangements, including a global reseller agreement with SAP.

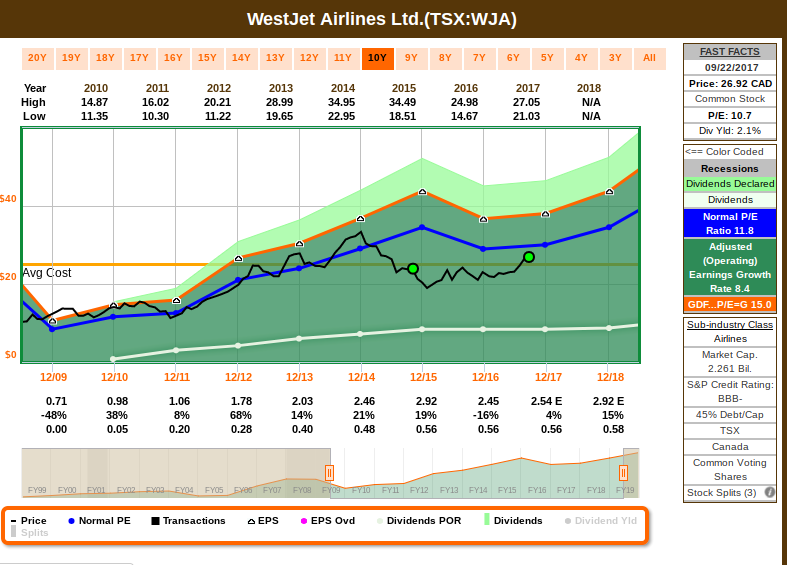

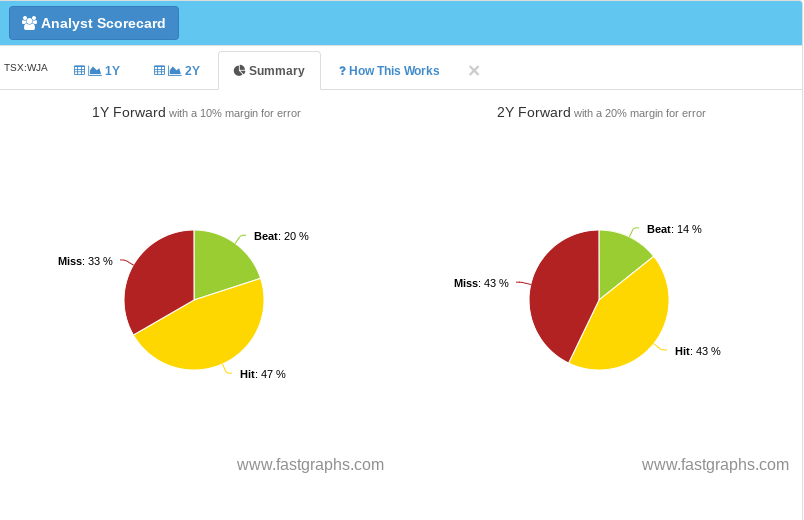

I will also be adding more Westjet. Considering how airlines can be volatile, I think WJA is handing it well and earnings and dividend growth estimates are also looking good:

Earnings were severely affected last year and somewhat this year due to the crisis in Alberta, and I like how WJA was able to keep dividends steady (supported by a healthy cash flow), and estimates are for a dividend growth next year:

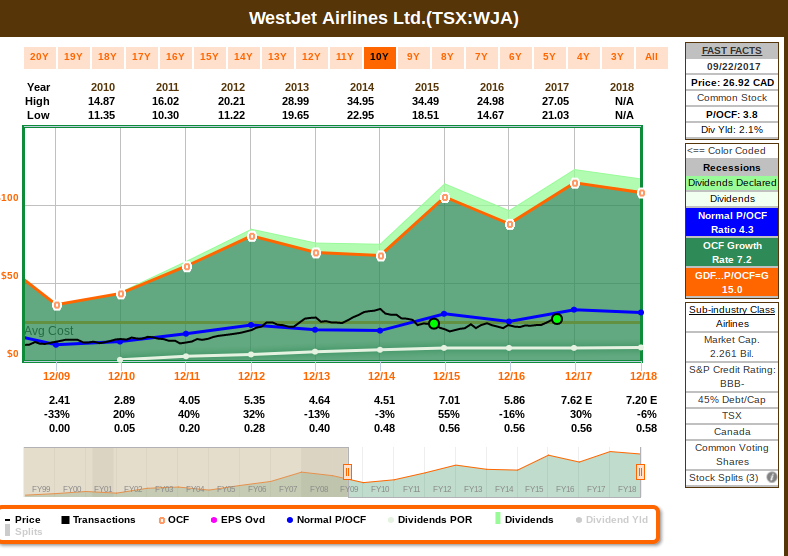

There is a large number of analysts covering WJA, so that forms a better market consensus – however, this is a very volatile industry, so the reliability on the results are not great:

WJA has been trying a number of growth initiatives, but the challenges caused some headwinds. Alberta recovery will eventually catch up, since that region has always brought above-average profit for WJA. Corporate guidance suggested that the weaker-than-normal (but still decent) 9.8% ROIC is a bottom, and the expectation is that it recovers to the historical range of 13% to 16%. Westjet expects growth through international expansion – their Boeing 767 is in service and they will purchase new Boeing 787 aircrafts. Meanwhile, WJA is expanding its regional arm, Encore, to obtain a presence on underserved routes – which has been very successful since introduced in 2013. Lastly, WJA is launching an ultra-low-cost arm that plans to begin operations by mid-2018, using 10 high-density Boeing 737-800s. WJA has an excellent tracking record of generating operating profits in such volatile industry, so I trust management that this execution level will continue. This might take time, as competition of Air Canada is increasing (as they’re getting better in improving their cost control), and these expansions are capital intensive, which affects ROIC. Nevertheless, I believe this is a solid company trading at a decent valuation, operating on a volatile industry that in the end is a duopoly in Canada.

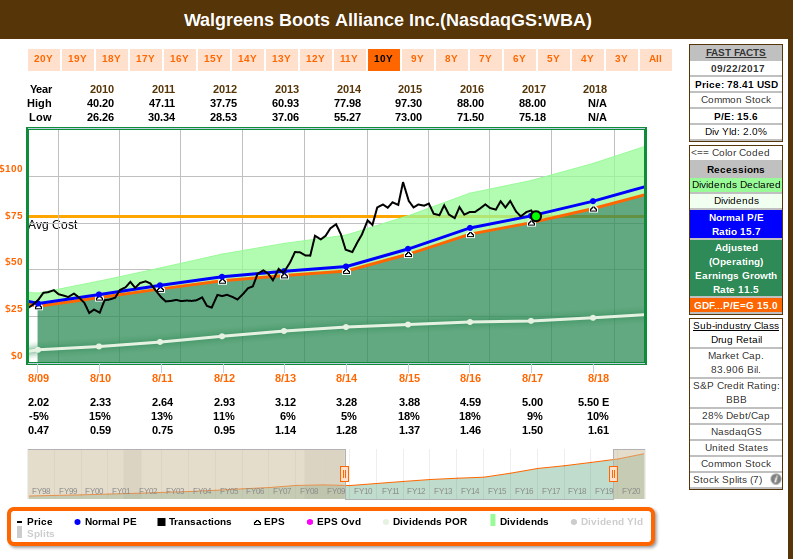

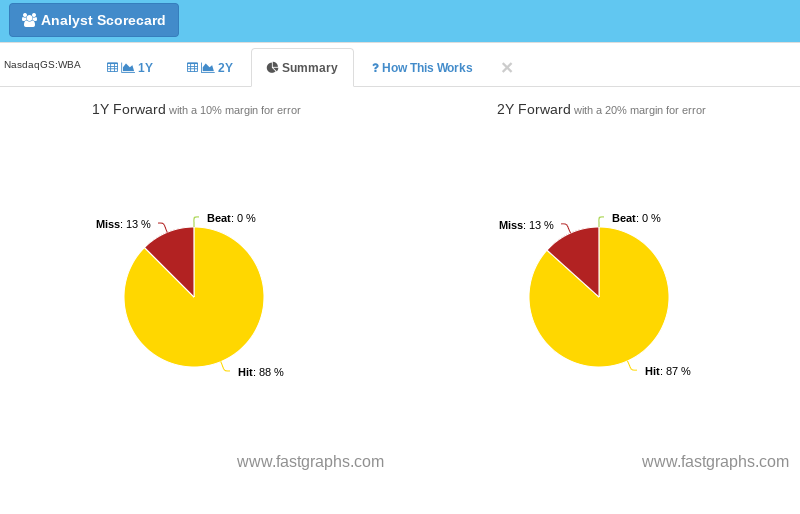

On the US side, I’ll be initiating a position with Walgreens. The company was overvalued, and since price follows earnings (and earnings and dividends are estimated to grow), I believe it’s currently trading at a fair valuation:

There is a high number of analysts covering this business, which gives me confidence for a reliable market consensus:

I know we keep hearing that “retail is dead”, but WBA has been one of the most successful retail operators since its founding in 1901 and has remained a major player within the pharmaceutical supply chain for many decades. The firm processed approximately 20% of total U.S. prescriptions during fiscal 2017, which makes it one of the largest retail pharmacies. With the acquisition of Europe-based Alliance Boots, the firm is now a premier global retail powerhouse. However, competition is fierce and heavy dependence on non-pharmaceutical products has hurt ROICs for some time. I like how management is reacting and adapting: WBA is in the process of closing the acquisition of half of Rite Aid’s store fleet, which will solidify it as the largest retail pharmacy chain in the U.S. This acquisition will not only increase its volume and geographic reach, but also materially augment its global generic purchasing volume. WBA will also be better-positioned to build on its preferred pharmacy strategy, although some analysts disagree with management direction of pushing the model to increase its nonpharmaceutical foot print. In the end, earnings and cash flow are the metrics that I’m looking for, and considering the strong market consensus, it brings me confidence to partner with them for the income growth journey.

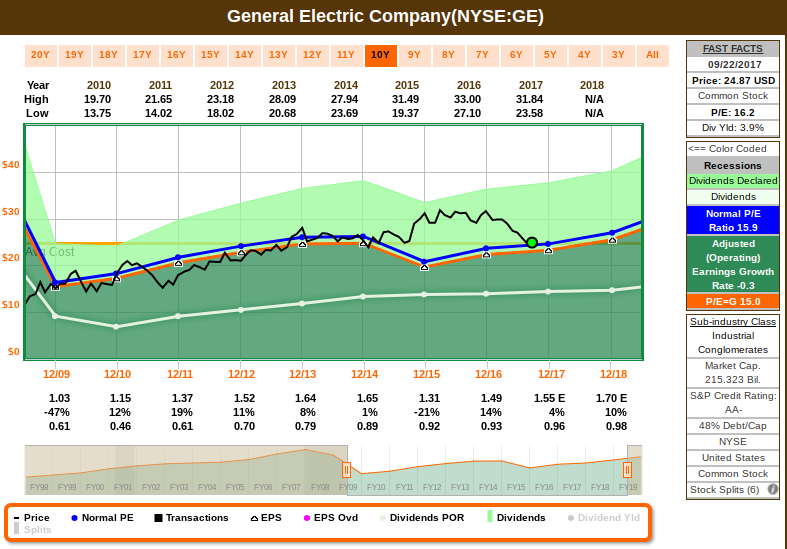

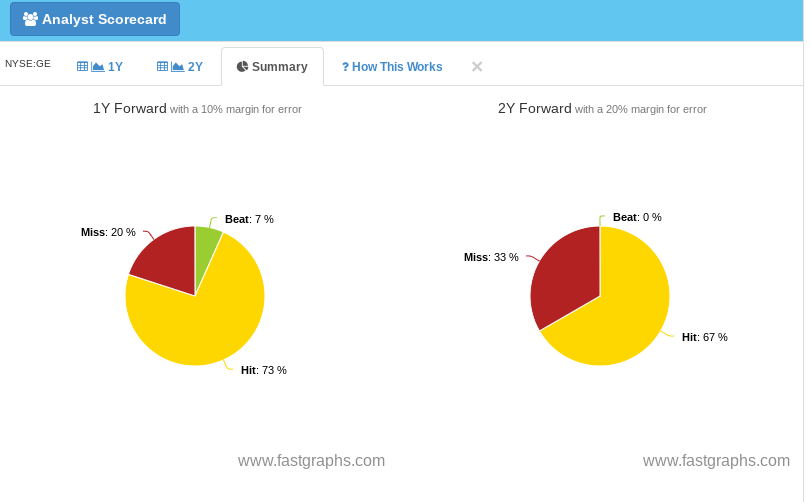

The other US company that I’ll be partnering with is GE. Their shares were also overvalued, and have recently come to a better valuation:

There is a decent market consensus, although the long term view has not always been aligned:

In order to keep competitive the industrial sector, GE now operates in 7 core industry segments to “lead a digital industry era”. GE keeps moving away from Finance with GE Capital, which I see as positive given the mess that it created in 2008; they are also stepping into the service world, which has been generating nice margins. Their push into predictive analytics will also generate synergies to fuel further growth.

I hope the research on some of these names inspire you to continue the journey to perpetual growth income.