I typically review my dividend portfolio at the beginning of the year, so while this is in progress, I thought about posting my views on some of the growth stocks that I own or plan to own. My long term investment strategy always has a mix of dividend companies that typically grow their dividends, with some growth companies.

I firmly believe that a comprehensive investing portfolio should be diversified through different drivers of returns: Long term investing based on dividend growth to build wealth overtime (and produce a growing income), and short term investing based on different techniques focused on growth and income (which I implement via my trading model). On top of that, I believe that every investor should have some long term growth stocks, specially if one is on wealth accumulation phase. I personally find extremely hard to evaluate growth stocks (and a lot easier to evaluate mature, dividend growing stocks), so perhaps the post below (and some others that will follow) can inspire you on the approach that I’ve taken to evaluate these businesses.

Not every growth company carries the same risks. Some growth stocks have been around for over a decade, so it’s easier to understand their pattern and how the market is comfortably evaluating them. It’s a lot harder to evaluate new companies, that are still growing and don’t present yet the expected metrics from a mature company, so I believe these offer a higher risk / reward case. A complete growth portfolio should have a mix of different risk / reward exposure in my opinion. Shopify falls on my higher risk / reward bucket, so I think it’s worth the consideration to partner with them.

Shopify Inc. provides a cloud-based multi-channel commerce platform for small and medium-sized businesses in Canada, the United States, the United Kingdom, Australia, and internationally. Its platform provides merchants with a single view of their business and customers in various sales channels, including Web and mobile storefronts, physical retail locations, social media storefronts, and marketplaces; and enables them to manage products and inventory, process orders and payments, ship orders, build customer relationships, and leverage analytics and reporting. The company was formerly known as Jaded Pixel Technologies Inc. and changed its name to Shopify Inc. in November 2011. Shopify Inc. was founded in 2004 and is headquartered in Ottawa, Canada, and its IPO completed on May 2015.

I believe that we shouldn’t evaluate Shopify the same way that we evaluate a traditional company through value investing (which is typically how I cover most stocks on this blog). Tech growth companies are typically valued by revenue, and the fact that a company has no or low earnings, matter little for valuation, at least during the growth and expansion phase. For most quality growth tech companies, what keeps the company growing is cash flow. Amazon and Salesforce.com have their stock prices typically tied to cash flow, not earnings (they always look ridiculously expensive if you go by price to earnings).

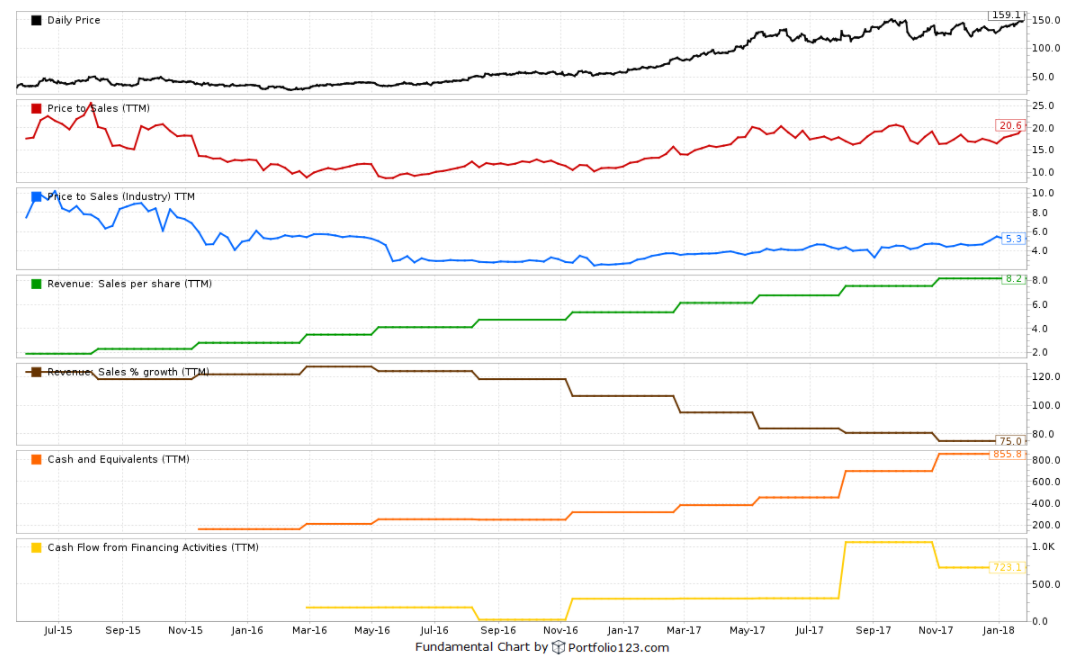

For tech companies that are more mature, cash flow from Operations is a good sounding board for valuation. However, for growth tech companies, that might be a poor way to evaluate it: although earnings and cash flow from operations are negative, Shopify has a positive and strong cash flow from financing, which is typically used for to provide long-term funds to the company and repay investors, changing or adding loans or issuing stocks. Cash flow from financing activities measures the movement of cash between a firm and its owners and creditors. It indicates the means by which a company raises cash to maintain or grow its operations. A company’s source of capital can be from either debt or equity. When a company takes on debt, it typically does so by either issuing bonds or taking a loan from the bank. Either way, it must make interest payments to its bondholders and creditors to compensate them for loaning their money. When a company goes through the equity route, it issues stock to investors who purchase the stock for a share in the company. A positive number for cash flow from financing activities means more money is flowing into the company than flowing out, which increases the company’s assets. Shopify have over $1B in assets ($927 million in cash) and less than $100 million in liabilities, which puts them in a comfortable position to endure challenging times and make further acquisitions to grow further market share.

As of end of 2017 Q3, cash flows from financing activities have related to proceeds from private placements, Shopify’s initial public offering, follow-on public offerings, and exercises of stock options. Net cash provided by financing activities in the 9 months ended September 30, 2017 was $570.6 million driven mainly by the $560.1 million raised by Shopify Q2 2017 public offering, and $10.5 million in proceeds from the issuance of Class A subordinate voting shares and Class B multiple voting shares as a result of stock option exercises. This compares to $227.7 million for the same period in 2016 , which was primarily proceeds from a public offering where Shopify issued Class A subordinate voting shares and received net proceeds of $224.4 million.

Many argue that Shopify is overvalued, but that’s why it shouldn’t be valued like a typical value stock. The market values the stock based on revenue performance, and the stock has always being valued at a price to sales proportional to the industry – just at a higher rate, but same curve:

Shopify’s stock price has followed revenue, and FY17 sales estimates range between $656 and $658 million. Their fiscal quarter ends in December, so they will be reporting annual results soon (earnings are estimated to be released on Feb 14, 2018). Revenue is estimated to grow by 45% for FY18.

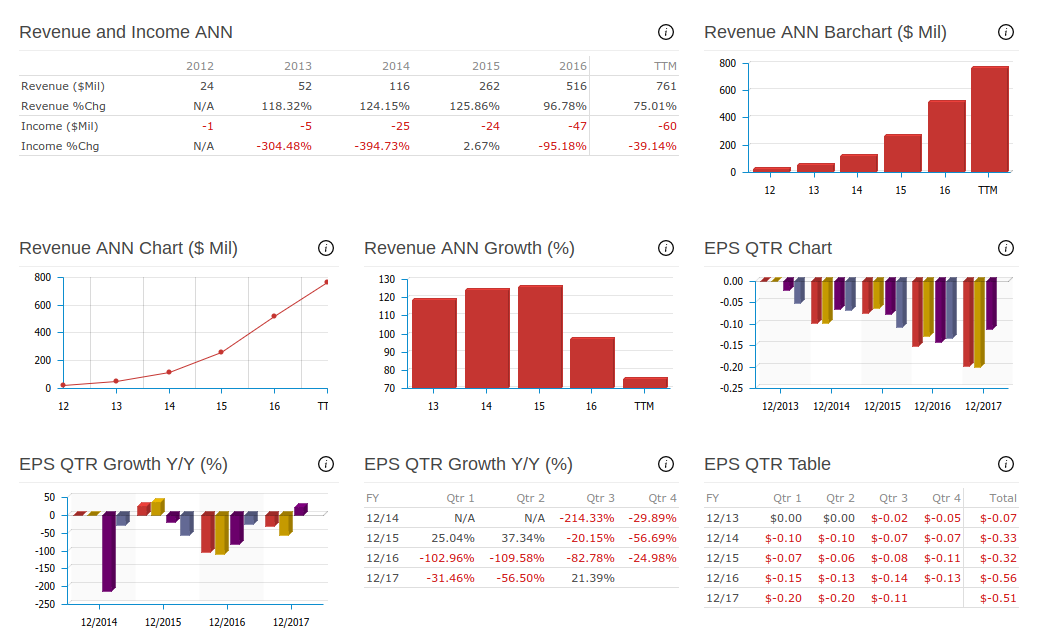

Below are more detailed metrics on how revenue has been increasing steady, while earnings remain negative:

The market has been evaluated Shopify to revenue and merchandise volume growth, so as long as these metrics keep improving, shares are likely to climb higher. SHOP has been trading at a much higher rate of price to revenue (around 8 times versus 6.3 times from peers), but that’s because they had a great revenue momentum. This higher premium rate will continue provided they meet the street estimates of 50% revenue growth, which is aggressive – you can only keep growing exponentially for so long. The current price to sales rate (18 times) is similar to what Amazon, Facebook, Salesforce.com and Google had when they started (15 times), where it later slowed down to a price to sales rate of 8 times to Salesforce.com, 3 times for Amazon and 15 times for Facebook. Shopify’s revenue growth is ~5x the e-commerce market and has averaged ~88% since Q1/15. Key platform advances that support this are mobile, addition of Apple Pay, apps, the Facebook Messenger buy button and integration with Amazon, Buzzfeed, eBay. In Q3, it added an Instagram channel and an augmented reality app.

Shopify’s platform is currently being deployed by over 500,000 merchants, which includes customers like the L.A. Lakers, Nescafe,Tesla, World Vision and Hootsuite. Partners include other web platforms (i.e. WordPress.com) and carriers (SingTel). Shopify’s largest competitor is Wix: a cloud-based web development platform that allows users to create their own web and mobile sites and add e-commerce functionality. Remaining Competition is fragmented, with a number of companies overlapping with certain functions and features. These could include Content Management Systems (WordPress, Joomla! and Drupal), ecommerce software vendors (eBay, Kijiji) and payment processors (Paypal, Authorize.net).

Shopify stock price has a lot of room to grow, considering that it’s a cloud / platform growth company, it’s been enjoying strong revenue momentum, and that’s how the market has been priced the stock. However, once revenue growth starts to slow down the market might question if the current premium over peers is still justified. Given the strong guidance for FY18, I believe we’ll still see new highs for FY18. Shopify will report their next quarterly results on February 15th, 2018.