The bull market continues strong, and a lot of companies are becoming very expensive. But even in a generally overvalued market there are reasonable valuations to be found. Therefore, it’s paramount to have an approach focused on value and quality.

A value investor does not validate their decision based on price movement. In fact, if price falls after they buy, and they are confident that their original decision was based on sound fundamental values, the intelligent reaction would be to buy more. Conversely, if price rises right after they buy, true value investors do not immediately pat themselves on the back and gloat about being right. It is only when earnings and dividends continue to advance that the true value investor believes that they’ve made the correct decision.

The value investing approach is the rational perspective of taking a long-term view. This is critically important, because it is all too common that undervalued common stock investments do not tend to perform well over the short run.

Common sense dictates that stocks only tend to become undervalued when they are simultaneously unpopular, at least temporarily. It is generally this unpopularity that creates the short-term discrepancy between fundamental value and stock price.

However, the greatest success derived from value investing happens when the company’s stock price is dropping even when the fundamentals of the company continue to remain strong.

Therefore, the key to implementing a profitable value investing transaction is to learn to focus on and trust the fundamentals supporting the business. In the same context, this further means adopting the conviction to not trust, and even the willingness to ignore poor short-term price action. Accomplished value investors understand that stock prices can lie, at least over the short run. But more importantly, accomplished value investors also understand that in the long run, fundamentals matter most.

Consequently, successful value investing requires a level of patience that unfortunately many short-term oriented investors do not possess. However, the rewards from investing in a truly undervalued stock can produce powerful long-term returns for the rational value investor who is capable of engaging in intelligent patience.

My last purchases were in April, so I invested the accumulated 3 months of capital into the following companies:

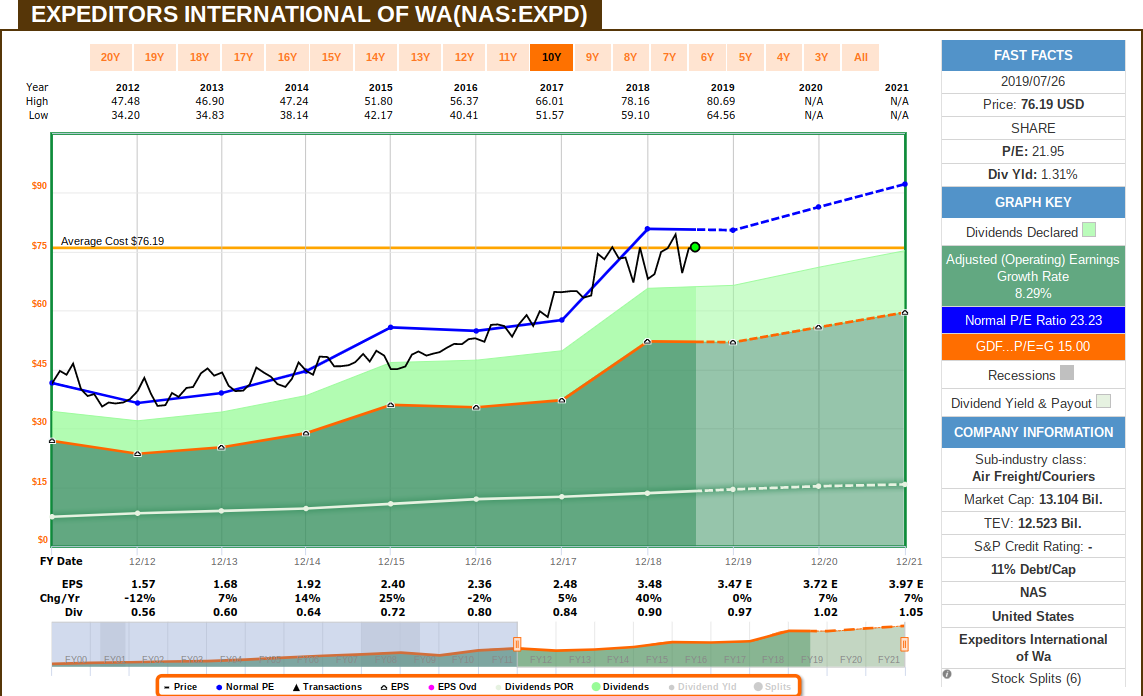

Expeditors International of Washington Inc. (EXPD):

Those familiar with Expeditors might claim that it’s an IT Company, not a freight forward company. That’s because their global IT platform is seamless, integrated and uniform – their system operates exactly the same no matter where your office is in the world, in the 6 continents that they are present. Expeditors is one of top 10 global freight forwards, with a proven history of solid operating performance and dividend increase:

As a global forwarder, the company contracts with airlines and ocean carriers for cargo space, and then fills that capacity with customers’ freight. A sizable customs brokerage operation (including warehousing and distribution services) complements air and ocean services, along with multimodal and final-mile delivery services in North America (Transcon). I like Expeditors better than other freight forwards because they have delivered solid results by organic growth only, instead of growing by acquisition like their peers. Their focus in heavy investing in IT infrastructure, aligned with their unique corporate culture, makes Expeditors a solid business that will continue to grow. Their corporate culture is built in a way that IT is strategic for the business, and their sales staff are considered company owners, since their salary is below the industry average and peers, but bonuses are tied to branch net revenue growth and operating profit, providing a strong driver to continue to grow. FY19 results are estimated to be flat due to tariffs (a lot of restocking was done last year, driving exceptional earnings growth), but earnings growth, and more importantly, net revenue, should resume previous level soon as freight demand will continue.

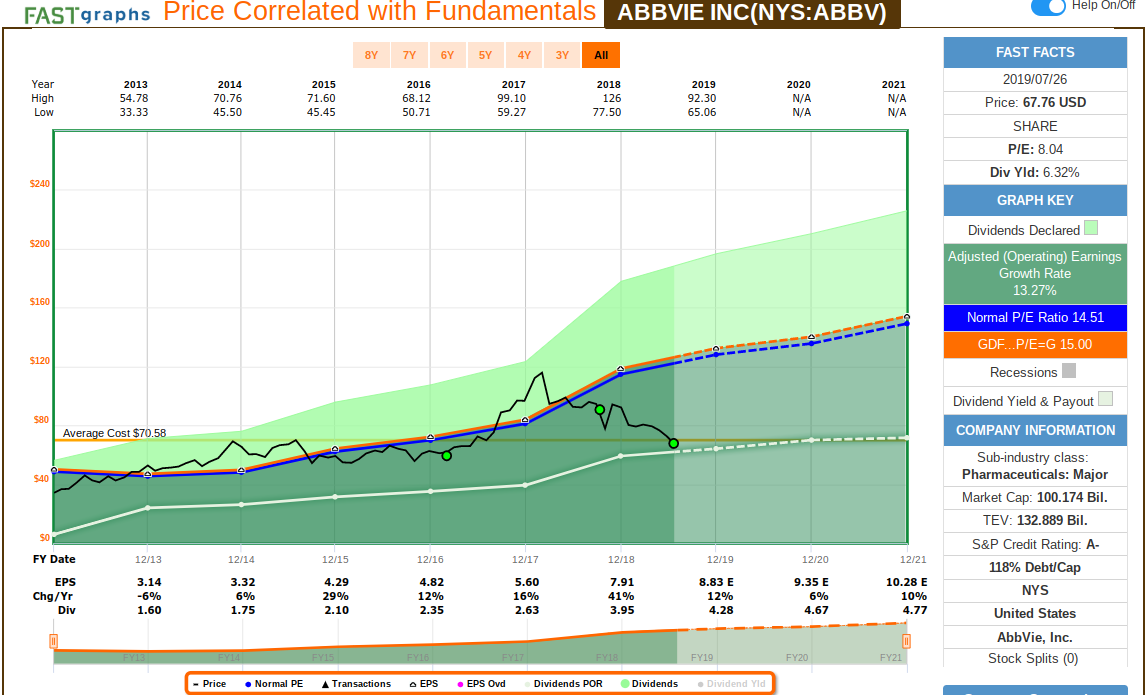

AbbVie Inc (ABBV):

ABBV has an excellent proven record, and the recent reaction from the market on their latest acquisition presents a great opportunity to partner with a solid business.

Market sentiment has been very negative with the fact that Humira drug has been driving a lot of the growth for ABBV, and that should slow down with the increasing competition. However, the market is not considering the new pipeline of drugs being built, and the fact that Allergan acquisition will bring a strong cash flow and diversification form a product that it’s known to not be dominant anymore. In my opinion, management is doing the right things by diversifying to other avenues. ABBV’s strong cash flows from its current product portfolio will fund ongoing discovery and development of the next generation of drugs. The large cash flows create an economy of scale that enables AbbVie to fund the average $800 million required for a new drug. ABBV’s R&D has created a database of intellectual insights that should help increase the odds of successful drug development. I believe the current valuation provides a decent margin of safety considering the growth that the new pipeline of products will bring.

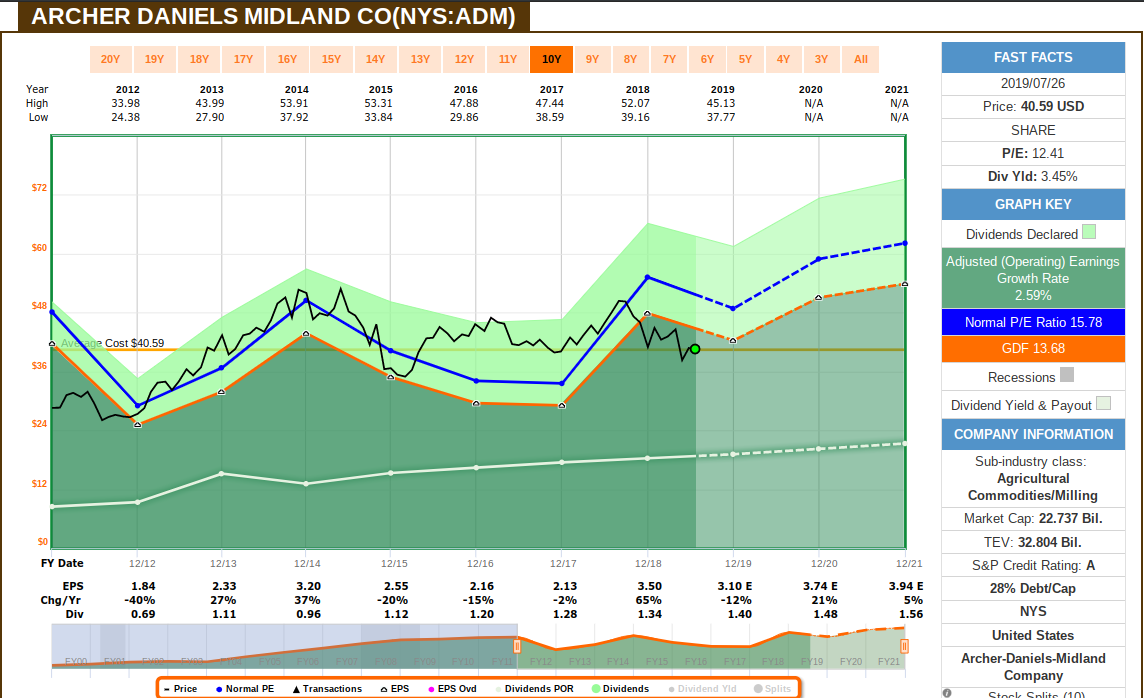

Archer-Daniels-Midland Co (ADM):

ADM is very cyclical, so I think now is a good opportunity to start / add more of their shares:

ADM is one of the few companies tied to commodity prices that is on my list. Typically any company heavily exposed to commodity prices will have a history of erratic earnings and it’s very capital intense, making it difficult to evaluate if the swings are due to their natural cycle or a sign of a bigger distress. However, ADM’s excellent credit rating, low debt to market cap and impeccable history of growing dividends for 25 consecutive years so far gives me the confidence to partner with them and tag along on their operating performance. Their business model is to purchase crops from farmers and then transports, stores, and/or processes the crops before selling them to food, feed, and energy buyers. Soybeans and corn are their biggest market. ADM expanded its flavors and specialty ingredients business primarily through acquisitions, having acquired Wild Flavors in 2014. ADM also expanded their nutrition business with the early 2019 Neovia acquisition. These acquisitions should drive growth help with margin. Their latest results were weak, but I think it’s important to see year over year results, as sales results will oscillate wildly due to weather and commodity prices. So adding when the stock is priced below its typical multiples is a good entry point, as well as a good opportunity to capture a higher yield, that is estimated to continue growing regardless of their cyclicality.

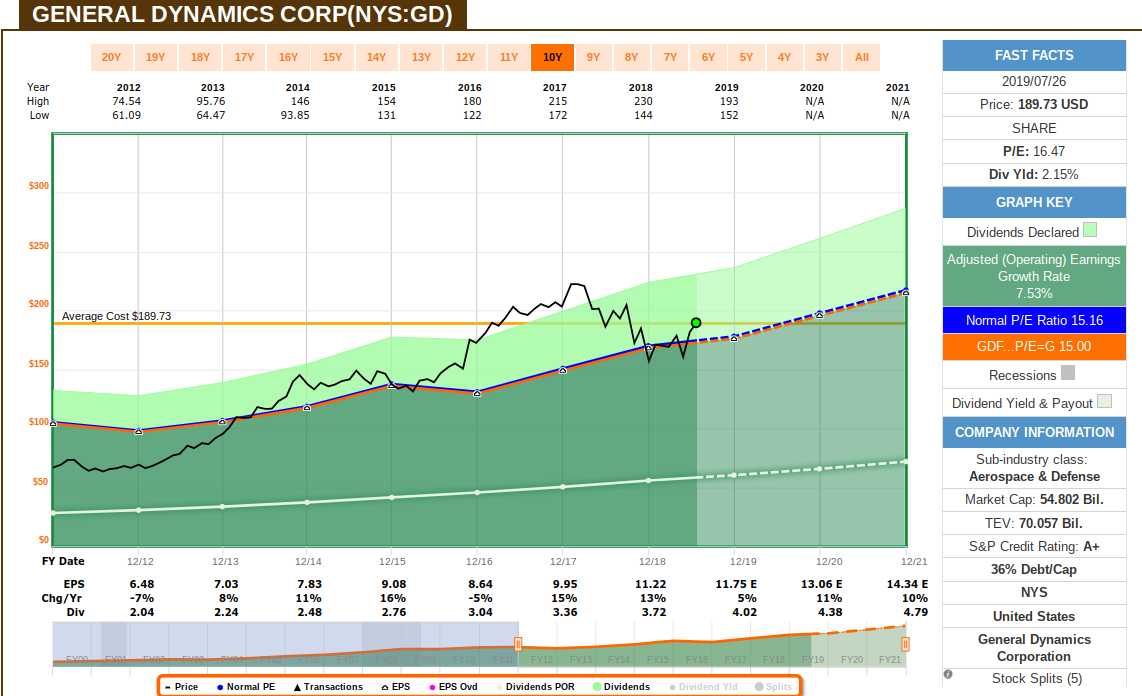

General Dynamics Corp (GD):

GD is a well diversified business in the Defence and Aerospace sector, it’s fairly valued and estimated to grow:

Since they acquired CSRA, GD became the 2nd largest IT contractors for the U.S government. Every 5 segments that GD operates on are estimated grow: The aeropspace segment, which operates the Gulfstream business jets, continues to be leader in the high-end business jet market and estimated to grow; Their combat systems segment, based on ground vehicles business, is estimated to grow driven by international expansion and higher US defense budget, vastly allocated for US army vehicle modernization program; Their marine systems segment is estimated growth on expansion of the Columbia program and larger US Navy ships; And their IT segment is being transformed post CSRA acquisition, having a business for regular / lower-end IT services and a higher-end / mission-critical business for strategic and critical defense missions. GD results reported on last quarter exceeded estimates on both revenue and earning.

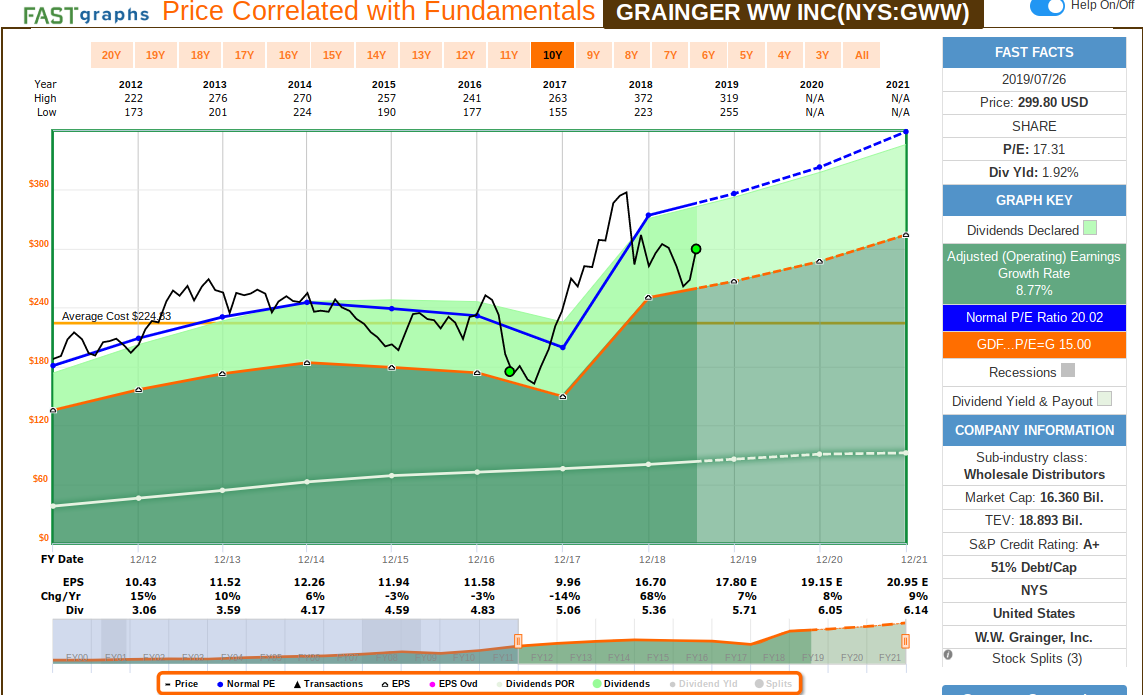

Grainger (W.W.) Inc (GWW):

GWW is finally fairly priced again and estimated to grow:

We can see that after GWW became on track for a huge earnings increase, vastly driven by the exceptional margin reductions in 2016 and 2017, share prices got overvalued and only recently came to a better multiple. We can see that GWW was trading at a higher multiple when it was supported by a strong operating results, but as the earnings level dropped, share prices followed a range close to 15-multiple earnings, which is the valuation that we see at the moment, and which is aligned with the future estimated growth rate. The niche that GWW operates is very fragmented, and operating margins drive a lot of the valuation (management’s current guidance assumes estimates operating margins growth from 12.2% to 13% for this fiscal year). Nevertheless, despite some swings on earnings, dividends continue to increase and supported by strong cash flow, which is my primary objective. GWW sentiment has been pressured since their biggest competitor is Amazon Business, but GWW continues to dominate an area that Amazon doesn’t have a presence, which is distribution to large enterprises. Last quarter results were shy of expectations, management maintained its full-year guidance, which projects sales to grow 4% to 8.5%, adjusted operating margin to grow from 12.2% to 13%, and EPS ranging between $17.10 to $18.70.

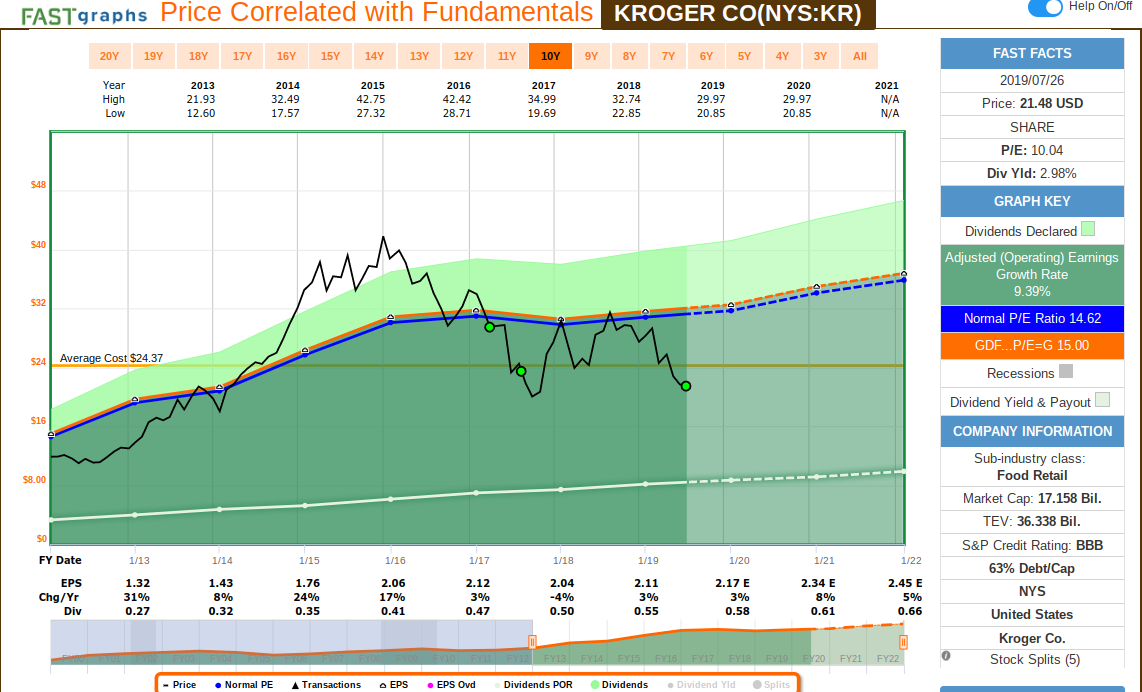

Kroger Co. (KR):

KR is very undervalued, and estimated to grow:

KR lower prices have been fueled by Walmart and Amazon expansion to the segment that KR operates on, but price is trading at a multiples that makes KR being a bargain. KR is a very well managed business and management is reacting and adapting to the changing landscape of the supermarket business. They can leverage their local market scale to offer competitive pricing and build presence; partnership with other strategic business adds further leveraging. Their customer data set is one of the best in the retail market, allowing them to target promotions, inform its assortment, and sell marketing insights (96% of sales are tied to their loyalty card). One of KR’s most competitive advantage is their own brand products, which grew 3.3% and unit share reached 28.9% share in the quarter. The focus on shifting the mix to Simple Truth and premium brands such as Private Selection led to double-digit gains in the quarter in those brands. KR’s digital sales grew 42% in the first quarter, and coverage area expanded to 93% of their customers in the first quarter (full coverage US-wide expected by end of the year). So to me, shares have been declining not because the business is underperforming, or struggling to operate, or without guidance. This is a business that is retransforming (from 100% brick-and-mortar with no digital sales dollars from 2014 to a 2018 annual run rate of about $5 billion, which will trend toward a $9 billion digital sales run rate in the future) and investing in the strategic areas to ensure they remain competitive.

Management maintained guidance of 2% to 2.25% identical sales growth (excluding fuel) and adjusted diluted EPS of $2.15 to $2.25. Management recently increased dividends by 14%, which is supported by their strong cash flow: management expects free cash flow of about $6.5 billion for the three-year period from 2018 to 2020. The average free cash flow per year is expected to be around $2.2 billion. For comparison purposes, Kroger generated free cash flow of $1.2 billion in fiscal 2018 and about $500 million in both fiscal 2016 and fiscal 2017. A company of this caliber trading at such lower multiples present a great opportunity in my opinion.

Happy Investing!