I firmly believe that we can always find good valuation in any market (bull or bear), including when the market is overvalued. If we consider the stock market as a supermarket of stocks, a place to pick and choose good companies when priced right, it becomes a lot easier to make a decision to start a position or buy more of an existing stock. Good quality of stocks starts by examining their past, present and future. The future analysis is a forecast exercise (but not a mere guess). Although the future is unknown, we can leverage corporate guidance, their success rate in meeting their goals and institutional analysts that cover these companies for a living. Collectively, these metrics provide information for us to make an informed decision in understanding the risks and potential profit (if our goal is total return) or by evaluating the income and potential growth of that income if the goal is to partner with a business that will slowly replace our salary with dividends.

My last purchases were in April, so I invested the accumulated 3 months of capital into the following companies:

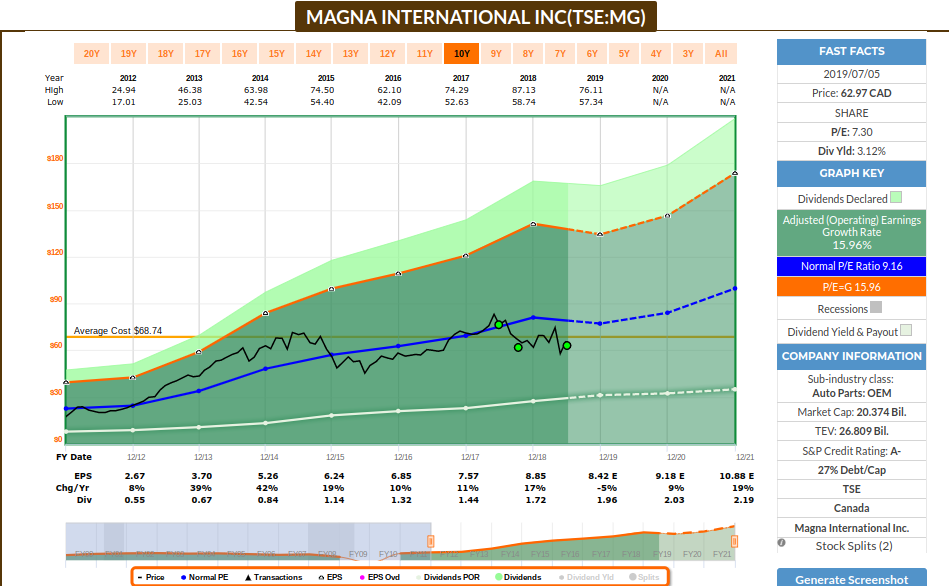

Magna International Inc (MG.TO): I believe MG.TO is undervalued considering its historical multiple and estimated earnings growth:

MG reported soft results last quarter and the sector is pessimistic on MG’s lower guidance. I believe that the recent drop, well below its typical multiples, present a good opportunity to add more of this dividend grower, while capturing a reasonable yield. Although recent guidance is for lower earnings in the short term, MG is still guiding to cumulative FCF of $6.5B from 201 to 2021, so MG is expected to continue to prioritize buying back shares and growing the dividend. Analysts expect MG to repurchase about 54MM shares in 2019/20 and spend $2.7B on its shareholder return program over this period. To me, now is the period to accumulate it, as it can remain overpriced for a long time, as seen in the graph above.

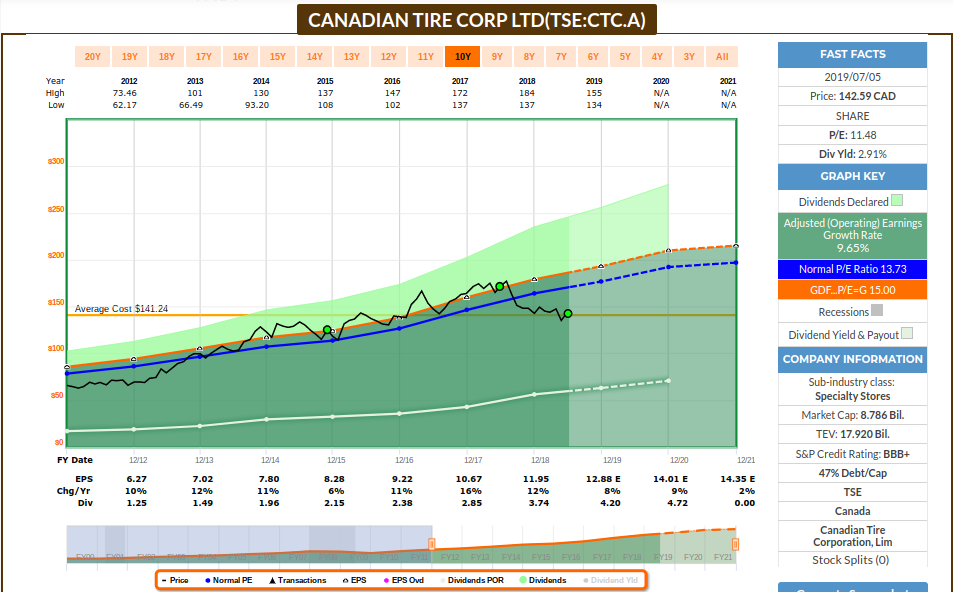

Canadian Tire Corp (CTC.A.TO): I believe CTC.A.TO is undervalued considering its historical multiple and estimated earnings growth:

I can’t stress enough how price does not equate to value. This is what Buffett means when famously quoted saying that price is what we pay, value is what we get. The graph below is a good example of Mr. Market ignoring that this business continues to grow earnings, cash flow and dividends – and that’s what makes it a great value opportunity. Sentiment has been negative due to the intense retail competition, but CTC.A seems to be doing all the right things to continue executing their strategy. Their business is also well diversified, with their financial services driving about 1/3 of pretax earnings.

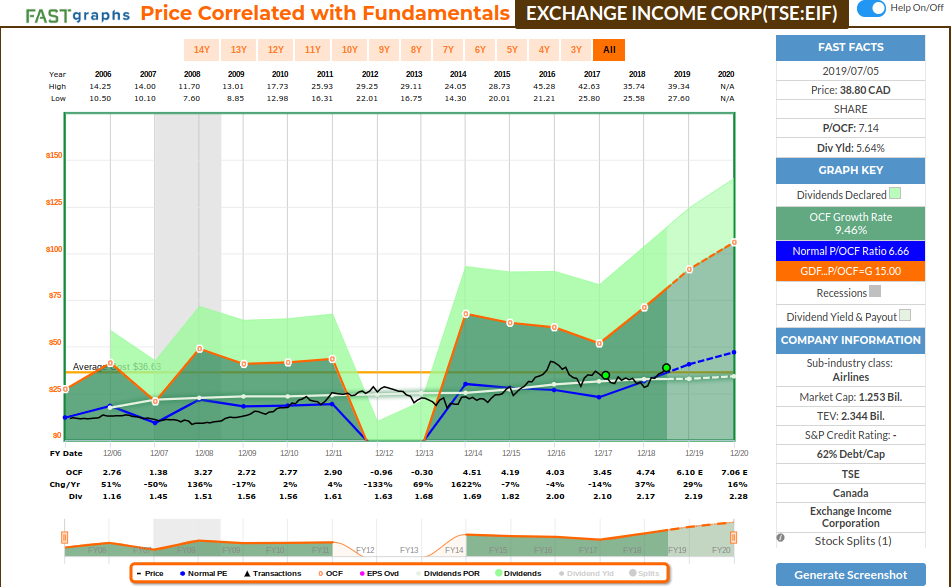

Exchange Income Corp (EIF.TO): I believe EIF.TO is fairly valued and estimated to growth:

EIF exceeded estimates on both revenue and earnings during last quarterly results, and since price tends to track their operating cash flow, I see it as a good opportunity to capture a great initial yield, with dividends estimated to grow as well. EIF is estimated to reap the fruits from the heavy investments done a few years ago, which should drive higher free cash flow. EIF has demonstrated to be a good capital allocator, being an acquisition oriented company focused on opportunities in the manufacturing and aeropspace & aviation segments. For those not familiar with EIF, the Aerospace & Aviation business segment provides scheduled airline service and emergency medical services to communities located in Manitoba, Ontario and Nunavut through Perimeter, Bearskin, Calm Air and Keewatin Airlines. Exchange Income Corp designs, modifies, maintains and operates custom-equipped maritime aircraft for customers internationally through PAL. Through Regional One, Exchange Income Corp supplies regional airline operators with focused after-market aircraft, engines and parts. The Manufacturing business segment makes various specialized and custom stainless steel products through Jasper Tank, Overlanders and Stainless; heavy duty pressure washing at Water Blast; telecommunication towers at WesTower; and precision parts and components used in the aerospace and defense sector at Ben Machine.

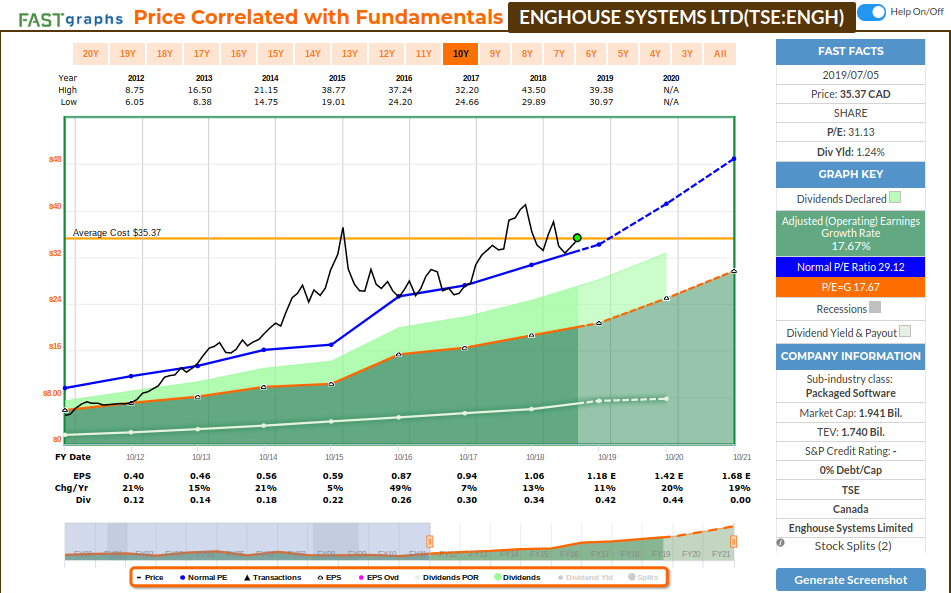

Enghouse Systems Ltd (ENGH.TO): I believe ENGH.TO is fairly valued and estimated to growth:

I have been waiting on the opportunity to start ENGH on this portfolio since 2016 (and to add more of my own personal portfolio when I started 21 years ago), as ENGH tends to be very expensive since 2012. ENGH exceeded estimates on both earnings and revenue when reported last month, and they also announced the Vidyo acquisition in mid-May and Espial acquisition near the end of May. Management expects these acquisitions on an annualized basis to add $70 million to $75 million in revenue, after being negatively adjusted for the purchase price accounting on deferred revenue and other items (revenue for next quarter will not reflect the purchase price accounting adjustment, but will only include revenue recognized from the date of acquisition rather than the full quarter; management believes that results will be EBITDA positive before restructuring costs for next quarter and improved further in Q4). So this is well aligned with ENGH acquisition strategy and their focus to capital deployment on this fiscal year. They also disclosed that ENGH closed the quarter with $205.5 million in cash position and equivalent (compared to $193.9 million last fiscal year), so they might do other acquisitions this year and in the future.

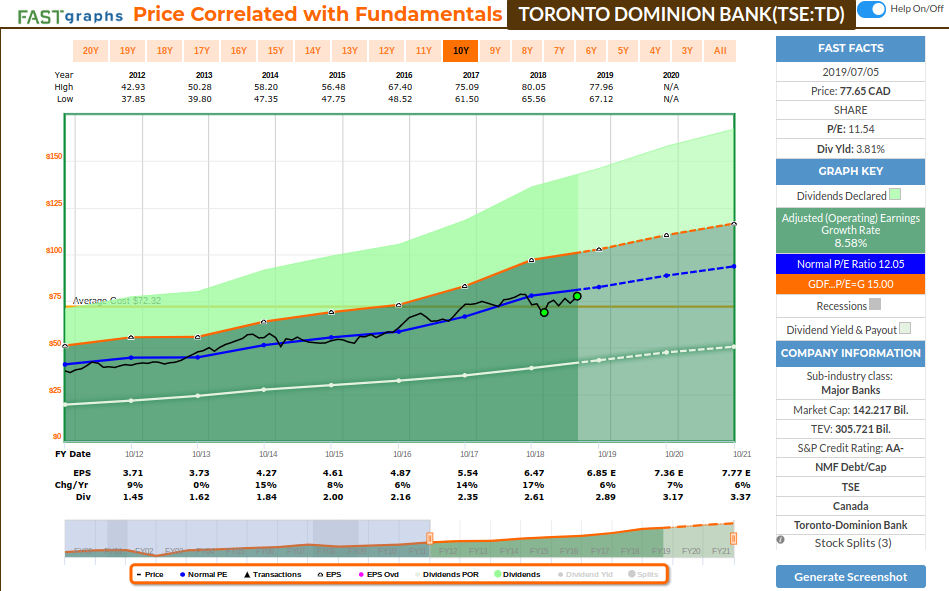

Toronto Dominion Bank (TD.TO): I believe TD.TO continues to be undervalued and estimated to grow:

TD derives approximately 60% of its revenue from Canada, 35% from the United States, and the rest from other countries. TD Ameritrade should be able to increase earnings at double digits over the medium term, providing a boost to TD’s overall growth. TD reported strong results last quarter, with the US side driving a lot of growth. Earnings and dividends are estimated to continue to grow, and the current price, a reaction of the weak 1st quarter due to capital markets swing at end of last year, presents an opportunity to lock a good yield fueled by a solid dividend that will continue to grow.

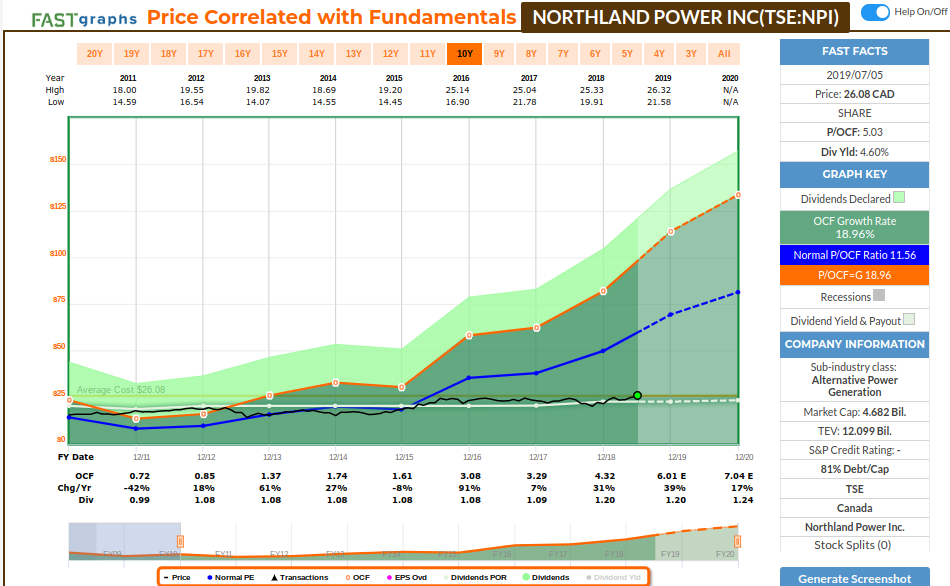

Northland Power Inc (NPI.TO): I believe NPI.TO is fairly valued and estimated to grow:

NPI was added this year to my watchlist, and they reported solid results last month. Management has EBITDA guidance of $920MM to $1,010MM for this fiscal year and AFFO/share guidance of $1.65 to $1.95. NPI is in the process of a major expansion with the recent completion of the ~$4.2B Gemini and ~$1.8B Nordsee One offshore wind projects, and the financed and in-construction ~$1.7B DeBu offshore wind project (management reported last month that DeBu is on budget and scheduled to reach Commercial Operation status in Q4/19). NPI was also awarded 300 MW of capacity in the recent Taiwan FIT procurement program and 744 MW under Taiwan’s offshore wind auction process. NPI is also adding new medium-term growth projects such as the recently announced La Lucha solar project in Mexico.

On the next post I’ll cover my purchases to my US portfolio.

Happy Investing!!

First timer coming on the website. I like your recommendations on Magna & Canadian Tire, those two are behemoths.

However I’ve seen the recent acquisition of Party City made my CTC.A, I’ve been kinda concerned on the board’s decision on that. What do you think on why they made that choice.

Also, I’ve seen on your watchlist that you recommend ENB & IPL. What are you thoughts on investing in Husky & Encana. I’ve been thinking on investing in Alberta’s crude industry and profiting from them but it’s a bit frighting since despite they have loads of cash, they are at their all time lows.

Again thanks for the help!

Hi Fahad, and welcome!

My consideration on the board for their decisions (for any stock that I own) is that I trust that management understands their business better than I do. With that said, I have a great deal of respect for this management team and personally trust that they have valid reasons for making their decisions. If I didn’t like the management, I would be interested in investing in the company.

For CTC, they are acquiring Party City Canada, which operates differently than the Party City Holdco which involves the US. In Canada, their business are healthier than in US (10% revenue and 40% EBITDA CAGR from 2015 to 2018), and they generate $140MM in sales and $18MM in EBITDA across 65 stores in 7 provinces. CTC management has the intention to double Party City Canada sales and almost triple EBITDA by 2021. There’s less competition in Canada and CTC expects to leverage their asset base to accomplish this: Party City Canada products will be rolled out in the 504 CTC stores nationwide and available on CTC website, and CTC expects to leverage their Triangle program on top of that. CTC has entered a 10-year supply deal with Party City Holdco, as they are the world’s largest designer, manufacturer, and distributor of party supplies and costumes. So time will tell how that execution will take place. CTC management has a good tracking record of execution, so I think this is a good opportunity to diversify their business further – really important if retail is slowing down, since their other business contributed significantly for their top line.

Husky and Encana are not on my list, as they don’t meet my quality criteria – cash flow is too erratic for my liking, so I get exposure to these sectors via other names on my list. This sector is very capital intensive and I think companies like SU and IMO, as well as ENB, IPL, PPL, and KEY provide a good exposure to these sectors with a reliable dividend growth.

I am up 9% with EIF since july 15, keep up the great work!

Rod, thanks for update, how do you reconcile “NPI.TO is fairly valued” with your fastGraph showing way undervalued on an OCF basis vs historical?

Hi John,

My approach was based on the fact that OCF have been growing at a rate higher than the stock price. So since NPI operates at a typical rate Price to OCF of 11.4 for the last 10 years, and OCF has been growing at a rate of 13.3% for the same period, I expect stock price to appreciate in the long term, as it hasn’t kept up with the operating growth of that business. However, it’s important to note that the graph looks somewhat skewed, because although price has only appreciated at an annualized rate of 7.8% for this period, ROR with dividends reinvested is 11.5% (but still less than their OCF growth rate).

Rod

Hello Rod,

What are you thoughts about Russel Metals Inc TSE:RUS please?

Thank you!

Hi Joe,

I don’t know how to evaluate a company like RUS, as their exposure to steel makes earnings and cash flow to behave very erractically. I believe there are better opportunities for cash deployment.

Rod

Hi Rodd,

Thank you very much for your insight.

RUS seems like a good skier who’s skiing uphill…

Thank you for being a beacon for intelligent investing!

Joe

Thank you for the kind words!

Would love to hear your thoughts on CIBC, AQN and a cheap rest, BPY.

Thanks!

Reit**

Hi Matt,

These companies are not on my list, so I don’t have up to date information on their operating results. However, the graphs below suggest that they are both fairly valued and estimated to grow. I don’t have estimated data on BPY, and I participate on that via BAM.A, which owns 51% of BPY. BAM.A is fairly valued and estimated to grow.

Rod