This was a busy summer, and I finally got a chance to take a look at what stocks from my watchlist are trading at an attractive price. As I posted earlier, that’s the beauty of dividend growth investing, it keeps making money while we sleep, generating income that can be reinvested anytime. My last purchases were done in July, and since I typically save C$2,000 per month to buy Canadian companies and US$2,000 per month to buy US companies, I now have C$6,000 + US$6,000 for me to go shopping on the market of stocks.

Canadian Portfolio

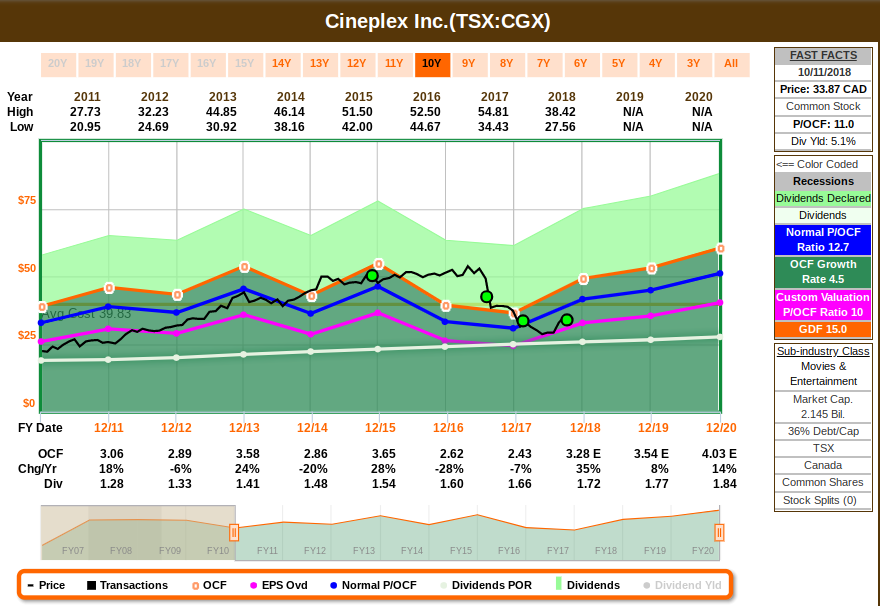

My first purchase is Cineplex (CGX.TO). I’m averaging down, to improve my average cost base. Cineplex has always traded at premium multiple, but as guidance has been lowered, business has been transforming to add other venues and competition is increasing, such valuation was no longer justified. Also, the past year was very weak in terms of movie releases, which affected their revenue. I believe they are better position now to grow, and both earnings and cash flow are estimated to grow. The graph below shows in blue their historical price to operating cash flow, while the graph in pink shows the valuation from back the days when growth was closer than what we have nowadays, aligned with current estimates as well:

Cineplex’s last quarter had strong results, and it shows that when there is quality content available, guest will come out to see. They remain on track to open new cinemas, new alternative programs (exploring niche markets), and growing other strategic areas, like the Cineplex store, which during the 2nd quarter CGX reported that registered users of the store increased by 40% and CGX recorded an 88% increase in device activations compared to the prior year period. On the media side, cinema media revenues increased 12.3% last quarter primarily due to an increase in show time advertising and digital plays base media revenue increased 9.9% due to an expanded client base which contributed to increased project installation revenue and advertising revenue. CGX continues to expand their Rec Room, and estimates to have a total of 9 locations of The Rec Room and 2 Palladiums in operation by the end of 2019. They are also on track to achieve the $25 million in annualized cost reductions by the end of this year, as previously communicated by CGX. The recent price decline is highly related to the unknown risks of their business transformation / expansion, but Cineplex has an excellent tracking record in execution, so I trust that management will continue to execute well and deliver these results. I purchased an additional 30 shares.

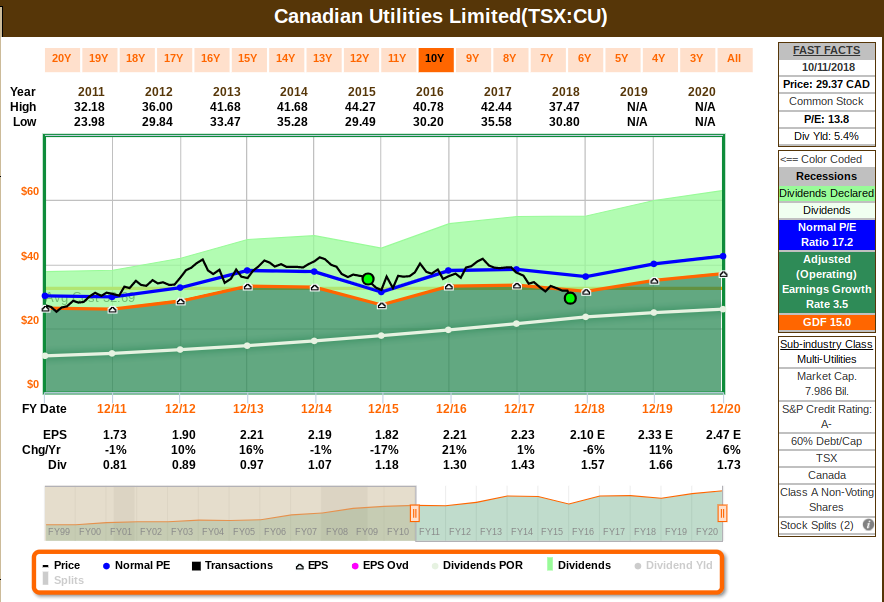

My second purchase is Canadian Utilities (CU.TO). I’m averaging down, as the company became cheaper due to interest rates increase. Earnings are estimated to continue to grow, which will eventually drive price up:

Growth is estimated to slow down, as the base growth in its core Alberta has moderated and the regulated rate is a headwind until CU deliver cost savings. Management also mentioned that dividend growth will slow down given the lower growth. These factors certainly contributed for the recent price decline. However, CU has a very good tracking record of dividend increases and a very strong balance sheet, which provides a good margin of safety. The potential acquisitions or new unregulated investments could provide further earnings growth and diversification to its asset base. Meanwhile, we get a juicy 5.4% dividend on this excellent credit rating company. I added another 34 shares.

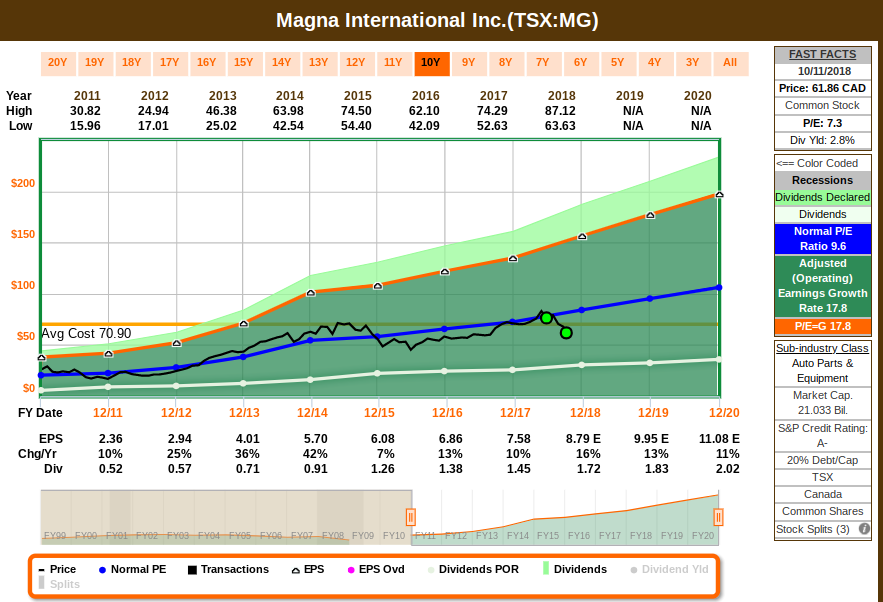

My third purchase is Magna International (MG.TO). I’m also averaging down, as I believe the company is cheaper due to NAFTA fears and lower guidance for 2018:

Although guidance is lower, MG has a strong balance sheet, has a guidance over $6 Billion of cumulative FCF from 2018 to 2020, and it’s estimated to continue to grow its dividends. The stock is trading at a low valuation and price hasn’t reflected the earnings and cash flow growth from recent years, adding further margin of safety. I’ve added 16 shares.

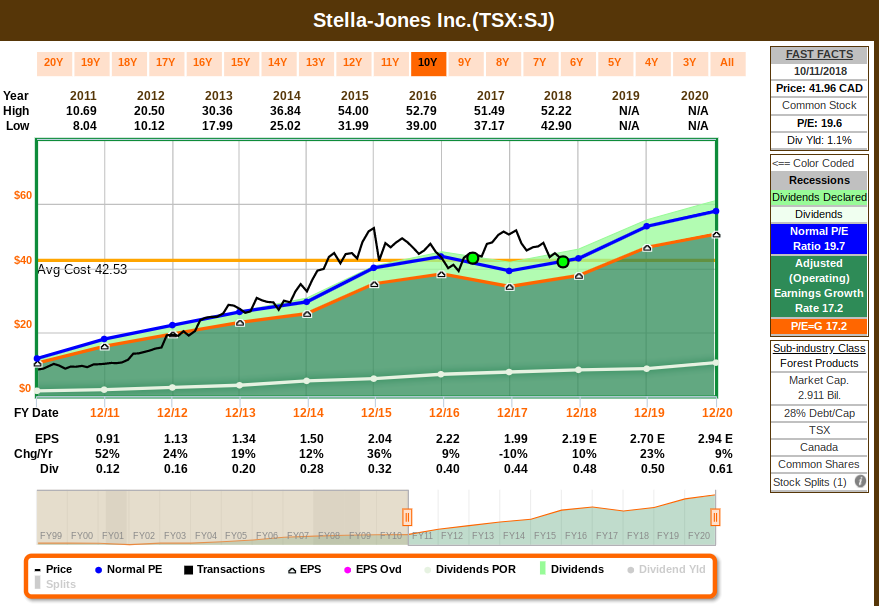

My forth purchase is Stella-Jones (SJ.TO). This company was overvalued and recently it came to a much better valuation – fueled by concerns of US housing slow down, and therefore, less demand for lumber.

SJ is on track to improve their operating margins on the second half of the year, although at a lower growth pace than the first half, given the current headwinds on US house slowdown concerns and increased railway tie costs. However, management has a solid tracking record on execution, and dividends, as well as operating cash flow and earnings are estimated to grow. I’ve added 24 shares.

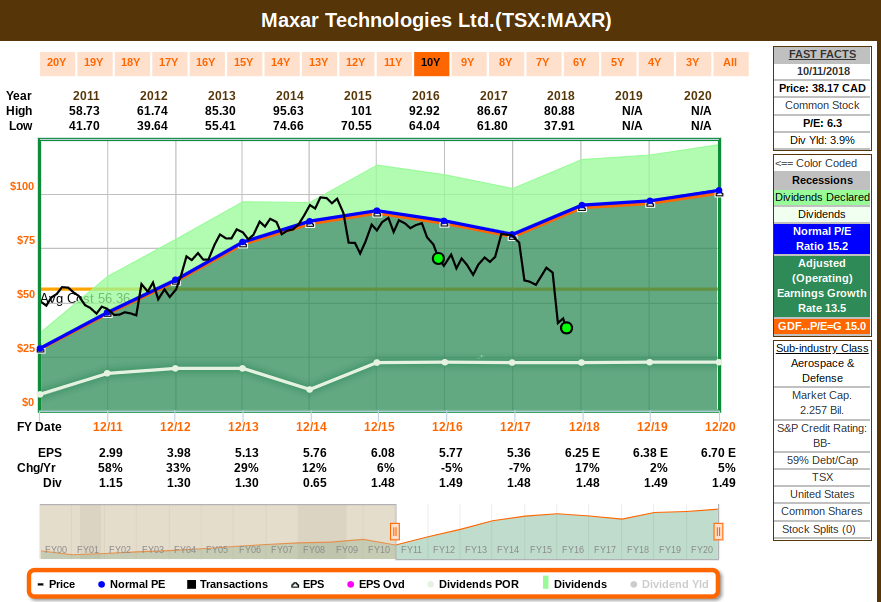

My fifth purchase is Maxar Technologies (MAXR.TO). I’m averaging down as price dropped a lot after Spruce Point Capital suggested that there will be no free cash flow after DGI acquisition, and that dividends are at risk of being cut or eliminated. The stock dropped sharply after the report, and MAXR responded to Spruce Point Capital that the report contains a number of inaccurate claims and misleading statements.

Spruce Point is a trader famous to short companies in big volumes, it’s not one of the institutional firms officially covering MAXR. So anything written there should be taken as the trader’s opinion. Second, he did the same thing with NCR in 2015. He compared the adjusted earnings results with the GAAP results. In 2015, stock price dropped a lot because of those “investigative” finds. GAAP results were lower due to acquisitions and other one-time expenses at the time – very similar to MAXR now. After a few quarters, both GAAP earnings and adjusted earnings increased for NCR, and so did the stock price. When partnering with a business, we buy the earnings potential. I’m expecting earnings to increase as the acquisition of DigiGlobe expands scale in satellite imagery, diversifies revenue (adds recurring data services) and increases exposure to US government programs. On Maxar’s recent Investors Presentation, they mentioned businesses opportunities that are starting to close on their 3 main areas: On the Imagery side, MAXR won the US Gov’t EnhancedView contract 2019 option-year exercise, Global EGD DARPA Geospatial Cloud Analytics program and the Expansion of International Government Direct Access Programs, estimated for 2019. On the Services side, MAXR won the Janus Geography ($920M 10-year IDIQ contract award), and it’s on track for its Cloud application development and Radar data analytics. On the Space System side, MAXR won the Telesat LEO communications constellation design contract (with TAS), the USAF next-generation secure satellite communications architecture, and it’s currently closing the Canadian Surface Combat ship program (~$1B) and Canadarm 3 for lunar-orbit gateway (~$1B), and it’s on track for the Telesat LEO communications constellation production (~$1.5B/$3B total) and Government and commercial LEO Earth observation constellations (~$500M). The integration of the DigitalGlobe acquisition is also on track, expecting $60-120 million cost and revenue run-rate synergies by end of 2019. MAXR has a high debt, but ample liquidity as it has $600M undrawn bank revolver line of credit (as of June 30, 2018), no material debt repayments required until 2020 and MAXR expects to achieve full-year 2018 adjusted cash flow targets driven by working capital improvements and the securitization of orbital receivables in the second half of the year. I’ve added 26 shares.

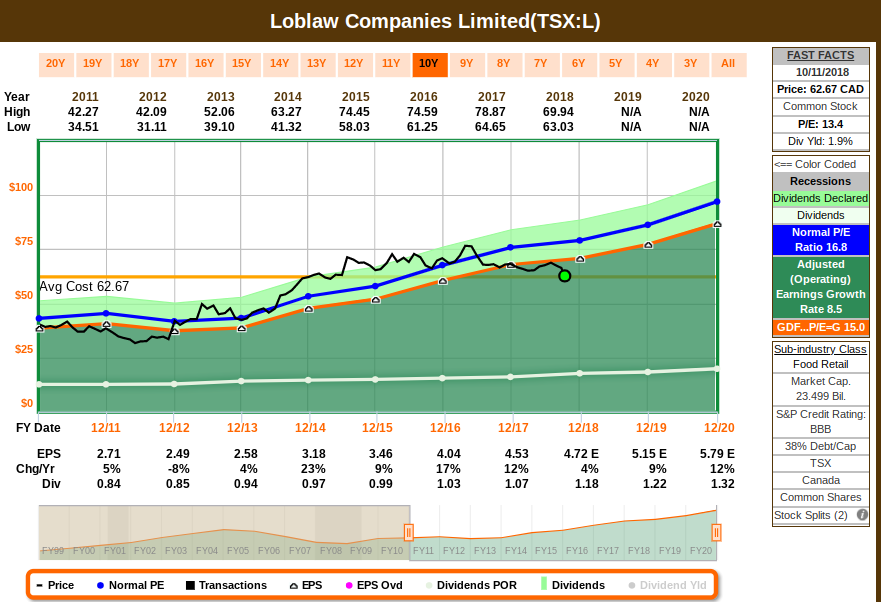

My sixth purchase for the Canadian Portfolio was Loblaw Companies (L.TO), to add more weight on the consumer staples sector. Loblaw has showing steady operating performance, but price has dropped recently, making it more attractive:

Loblaw has a good tracking record on earnings and cash flow growth, and it demonstrated great execution on Shoppers integration. It’s trading at a better valuation than its peers and its stable and reliable free cash flow should fund future dividend increases and share buybacks. Loblaw is the largest food retailer in Canada, with operations in every province and it booked over $45 Billion in sales. Loblaw also features the top 2 private-label brands in Canada (President Choice and No-Name), which should help it continue driving traffic into stores and compete with new entrants. However, management stated that there is a strong possibility of an accelerating retail price inflation in the market, due to incremental set of costs that have begun to impact them now like transportation and the costs that are going to impact them in the future like the impact of tariff (new Canadian tariffs were imposed on $16.6 billion of US imports). That helped to make valuation more attractive – as I believe that management will continue to deliver in this challenging environment, I bought 16 shares.

US Portfolio

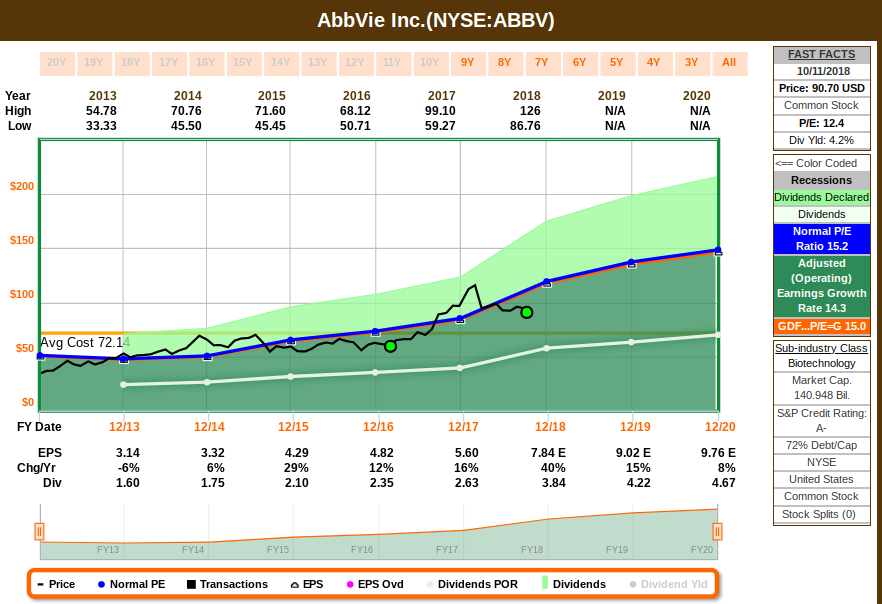

My first purchase on the US side was AbbVie Inc. (ABBV). The stock was a bit overvalued, but price came down to a better valuation recently.

Earnings, cash flow and dividends are estimated to continue to grow. Most of ABBV performance is due to Humira (about 65% of ABBV’s revenue), which is facing increased competition, but ABBV has made deals with several large potential competitors to delay sales of Humira biosimilars till 2023. ABBV’s next biggest drug by revenue is Imbruvica, which is expect to grow to $3.4B in sales from $2.6B in 2017. Hepatitis C treatment is also a large area, especially with the Aug. 2017 FDA approval of Mavyret. I’ve added 11 shares.

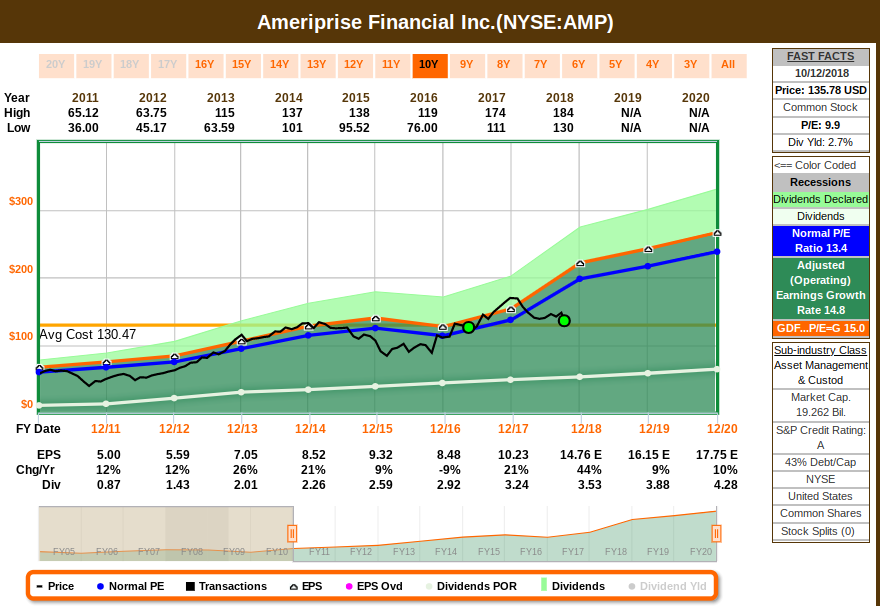

My second purchase on the US side was Ameriprise Financial (AMP). The stock is undervalued again, and given how earnings, dividends and cash flow are estimated to grow, I think it’s a decent opportunity.

Ameriprise is a diversified financial services company that spun off from American Express in 2005, and it provides insurance, annuities, wealth management, and asset management services. They continue their transformation to place more emphasis on asset and wealth management operations, driven by Columbia Threadneedle Investments, the firm’s global asset-management business. By positioning itself as a one-stop shop for the baby boomers, offering advice in financial planning, fund investment, and insurance purchase, the firm makes it that much harder for the boomers to switch to another provider. I’ve added 7 shares.

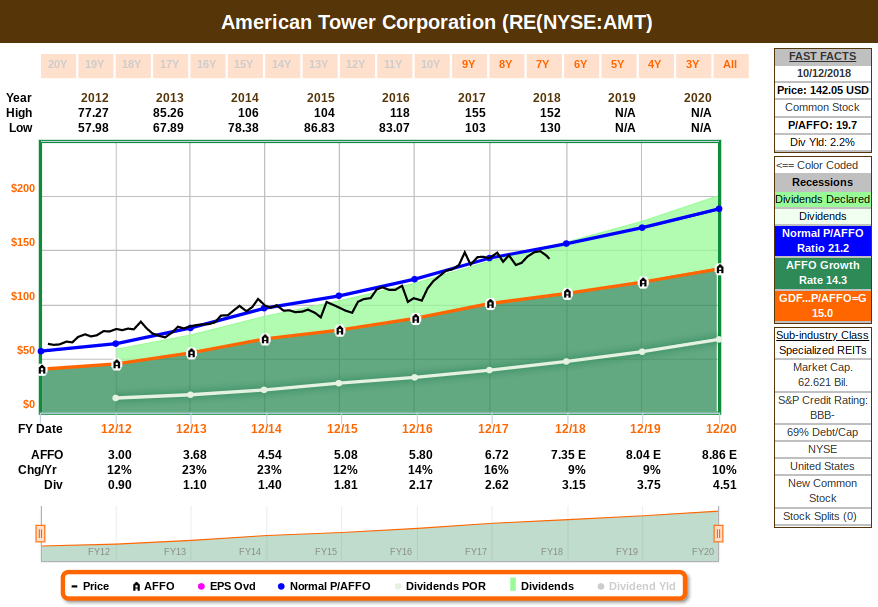

My third purchase on the US side was American Tower Corporation (AMT).

AMT operates the largest independent portfolio of wireless communications and broadcast towers in North America. Free cash flow, earnings, adjusted funds from operations and dividends are estimated to continue to grow, as demand for mobile won’t slow down. AMT is expanding internationally and there is a healthy organic growth in North America. I’ve bought 7 shares.

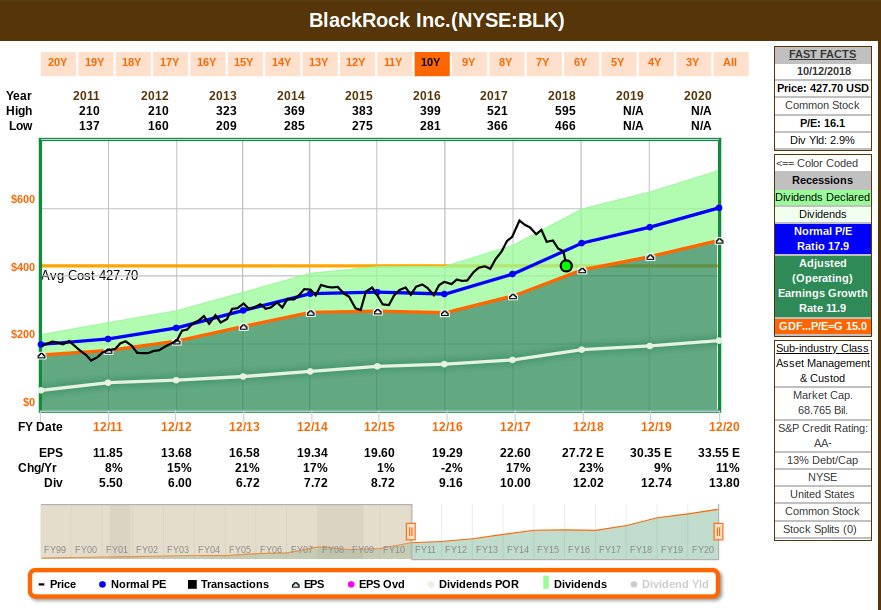

My forth purchase was BlackRock Inc (BLK). The stock was overvalued, but has recently dropped to a much better valuation. Earnings and dividends are estimated to grow, which I believe to be another good opportunity:

BlackRock is the largest asset manager in the world, with $6.3 trillion in total AUM at the end of June 2018 and clients in more than 100 countries, generating solid organic growth with its operations with its iShares platform, which is the leading domestic and global provider of ETFs. This has allowed BLK to ride a secular trend toward passively managed products that began more than two decades ago, helping the company maintain average annual organic growth of 4%-5% the past several years despite the increased size and scale of its operations. Like most asset managing companies at this moment, they are trading at a discount, which puts the quality companies at an advantage to be purchased at a much better valuation. I’ve purchased 3 shares.

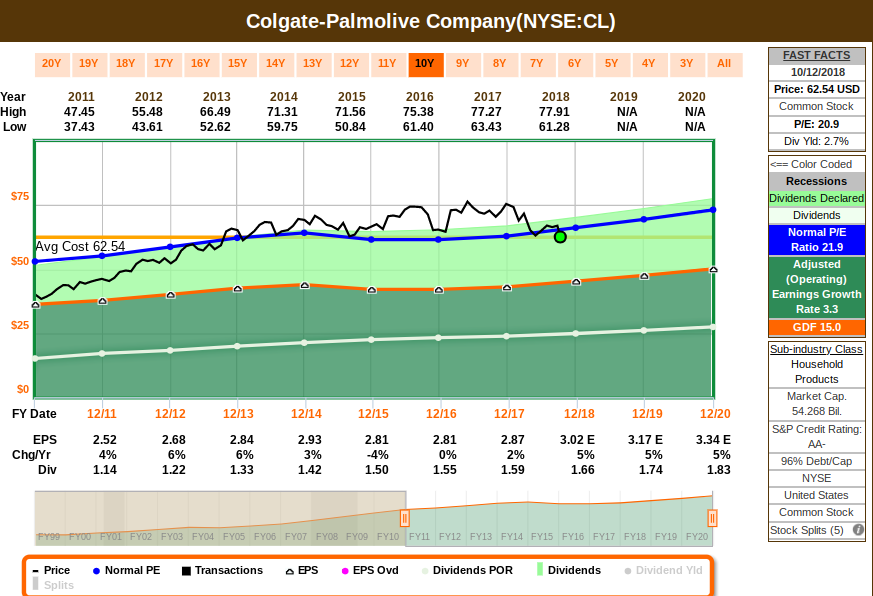

My fifth purchase was Colgate-Palmolive (CL). Fantastic household products’s company trading at a good valuation now.

Sales are estimated to grow modestly this year and improve a bit next year, but both at low numbers. Emerging markets continue to drive most of their performance, and overall, margin are estimated to remain at decent double-digits. CL is a very reliable dividend grower, which is one of the primary reasons for my decision to partner with them. I’ve purchased 16 shares.

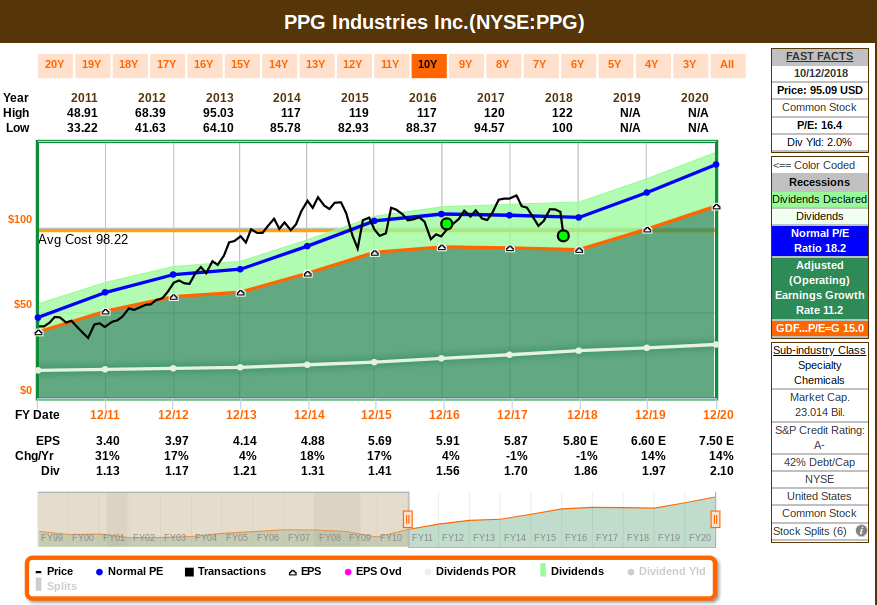

My last purchase for this month was PPG Indutries, as the stock became fairly valued again:

PPG shares dropped as management warned of lower guidance (about 6% to 9% below street consensus) due to significant raw material cost inflation and somewhat weaker-than-expected demand in certain segments. In my opinion this is temporary, as specialty coatings (used in aerospace sector), composes about 60% of the company’s coating business and it allows PPG to pass the raw material cost increase to customers. However, the other 40% is on a more commoditized market, that requires PPG to remain competitive in price. PPG is subject to market cyclicality on housing, construction and automotive sector, so I try to take advantage of opportunities like the current lower prices, because the quality factors in this business remain strong. I’ve added another 11 shares.

I hope these purchases gave some ideas on what to buy next, but more importantly, why it’s being purchased. My goals when investing are oriented towards safety, income, and consistency. Hence such diversification in all those stocks – by holding different quality business, it helps to ensure the income growth on the portfolio overall, even if a few companies don’t raise their dividends on a given year, or even if they cut or eliminates their dividend, as it happened before.

A few people asked for my thoughts on the recent correction. I don’t look at the overall market but rather individual, high quality, attractively valued businesses. Instead of worrying about a market correction, I try to focus on the business I am investing in, what I believe its current intrinsic value is, and most importantly what I expect future intrinsic value to become. We can’t control price fluctuations, but we can control the quality of the companies we purchase. The higher the quality, the more confident I am that the company will bounce back on any price drops. And also why investing is for the long term. Price doesn’t reflect the changes in fundamentals, as companies report only 4 times a year. A business cycle lasts 5 to 7 years. So patience and discipline are required. Meanwhile, let time and the compound growth do its magic.

Happy Investing!

Nice Post !

Thanks for sharing !!

Thanks for answering my questions.

I’m with TD DI and recently started following your portfolio for my TFSA and RRSP. I got them to make US accounts of both too.

How do I receive dividends? Is it deposited directly into my bank account, or my investment account?

Are there any transaction or other fees with DRIP? Is it advisable to ask them to set up DRIP for me?

Hi TR,

Dividends will be paid in cash on your investment account. You will notice that your cash portion of your portfolio will start to grow slowly. I use that cash, plus the cash that I save at every paycheck, to buy more shares. If you want them on your bank account, you need to initiate a withdraw request.

There are no fees with DRIP. However, I don’t like DRIP, because it always buys the stocks, regardless if it’s fairly valued or expensive. Buying more shares of a given company only makes financial sense when it’s fairly valued or undervalued. Also, you don’t want a position to become overweight. For this reason, I decide every month on how I’m investing the cash from dividends. It’s more work than having a DRIP setup, but I think it provides a better reward in the long term.

Please let me know if you have any questions.

Thanks!

I just put in a buy order for GIL based on your suggestion in the Canadian Trading model. I noticed it is also on your investing portfolio. I am thinking of keeping it as an investment rather than a trading stock. Was $41 a good price for investing, or just for trading?

Hi TR,

As an investment, I like GIL: it meets my quality criteria for earnings and dividend growth, and it’s estimated to continue to grow. It’s currently fairly valued, so $41 was a good entry price considering the present information. GIL is also on the trading model, but it follows rules targeted to short term performance, so it was bought (and it will be sold) for reasons not related to long term investing focused on growth of dividends and positive total return. You can see below how GIL is estimated to grow and how it’s presently fairly valued compared to its estimated future growth:

That’s a good point about DRIP. But if I am investing $1000 at a time in any stock and the transaction fee is $10, I am wondering if DRIP makes financial sense regardless of not being fairly valued.

I haven’t read Benjamin Graham’s book so maybe that would be a good start.

For the US stock that you purchase in the RRSP, do you use a US RRSP?

Yes – my brokerage account (with Interactive Brokers) allows a US and a Canadian side for my investments. The US side allows dividends to settle in US$ and I only need to do the currency conversion once.

I understand these are for long term investment and not for trading, but have you ever had to sell the stocks in your DGI portfolio because of how it was priced?

Hi TR,

There scenarios that I typically sell are described on this link (on tab “When to sell”). On the annual review I go through that exercise.

Pricing is not a reason to sell for me – simply because I’m after the dividends. I won’t buy an overvalued company, but I won’t sell either (provided fundamentals are still in check) because dividends can be deployed to buy other businesses that are fairly priced. However, many people has the approach to sell when it’s overvalued, and that’s fine too, since total return from that point will likely be lower (due to the current overvaluation), and the full capital can be deployed elsewhere. Nothing wrong with that approach, but I don’t typically do it to not disrupt the cash flow stream.