Enbridge and its group of companies belong to the Oil & Gas Transportation subsector subsector, and this sector is more of a utility and service operation, where performance is very stable. That’s because of its continuous flow and measurable revenue stream for future forecast. EPS continues to be a decent measure for quality, but not for valuation – and that’s why P/E or payout ratio from earnings is misleading to measure these kind of businesses. EPS is not a good valuation metric for midstream companies due to high non-cash depreciation expenses, such as the capital intensity of building and maintaining all of its pipelines and terminals. Look how DD&A metric (depreciation, depletion and amortization expenses) impact earnings. Hence a better valuation metric for midstream companies are cash flow, precisely available cash flow from operations (ACFFO). It measures how much net cash the company is bringing in, minus any preferred dividends and maintenance capital. Therefore, it is a solid measure of how much cash flow the company has remaining to pay its dividend and to invest in growth projects.

Before diving into earnings and dividend tracking record for Enbridge, I thought it’s important to differentiate ENB (Enbridge Inc) from ENF (Enbridge Income Fund Holdings Inc), which is one of the group companies from Enbridge.

Enbridge is a North American leader in energy delivery, transmission and distribution. Enbridge operates the world’s longest crude oil and liquids transportation system across Canada and the U.S., and has a significant and growing involvement in natural gas and renewable energy. Major business segments include Liquids Pipelines, Gas Distribution, Gas Pipelines and Processing, Energy Services and Green Power and Transmission. This year Enbridge completed the merge with Spectra Energy corp, which enhances Enbridge’s growth platform, provide diversification benefits and extend the company’s 10%-12% dividend per share CAGR through 2024 (prior 2019), including a 15% raise in 2017, without a material change in payout ratio. Spectra Energy is a leading pipeline and midstream company in the United States and Canada with natural gas, NGL, and crude operations including transportation, storage, gathering and processing, and distribution and their major business segments are Spectra Energy Partners (U.S. Transmission, Liquids), Gas Distribution, Western Canada Transmission & Processing and Field Services.

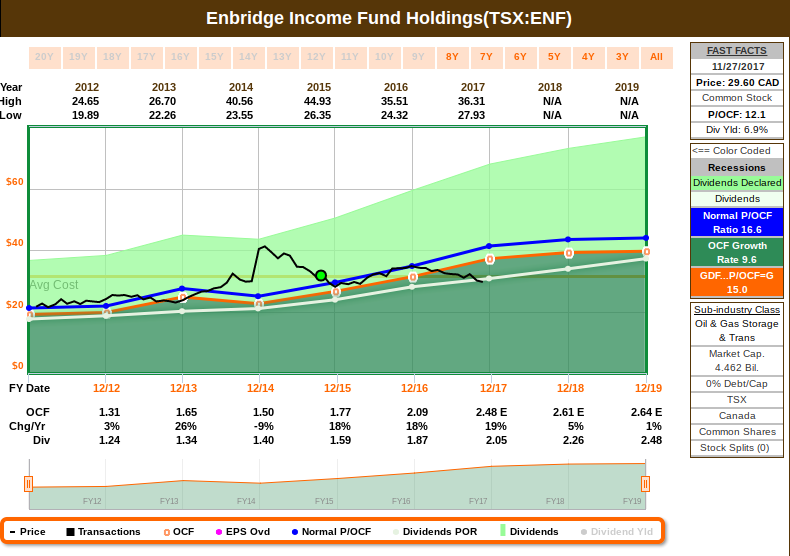

Enbridge Income Fund’s business objective is to pay out a high proportion of available cash in the form of dividends to shareholders. It’s business is limited to its 56.6% ownership in the Fund’s issued and outstanding trust units, representing a 13.1% economic interest in the overall Fund. Enbridge holds the remainder of the Fund Units, 100% of the Preferred Units issued by Enbridge Commercial Trust (ECT), 100% of the class A, C, and D units of Enbridge Income Partners LP and and 19.9% of ENF, resulting in a 90% economic interest in the Fund. This is achieved by having a structure with portfolios of low-risk energy infrastructure assets in North America that consistently generate strong and predictable cash flows, with assets that are underpinned by strong, long-term commercial arrangements that serve to reduce volume risk and commodity price exposure. Since the fund is structured to receive cash flow through ownership interest in the Fund Group and pass that in form of dividends to ENF shareholders, the best valuation metric for ENF is Adjusted Funds From Operations (AFFO).

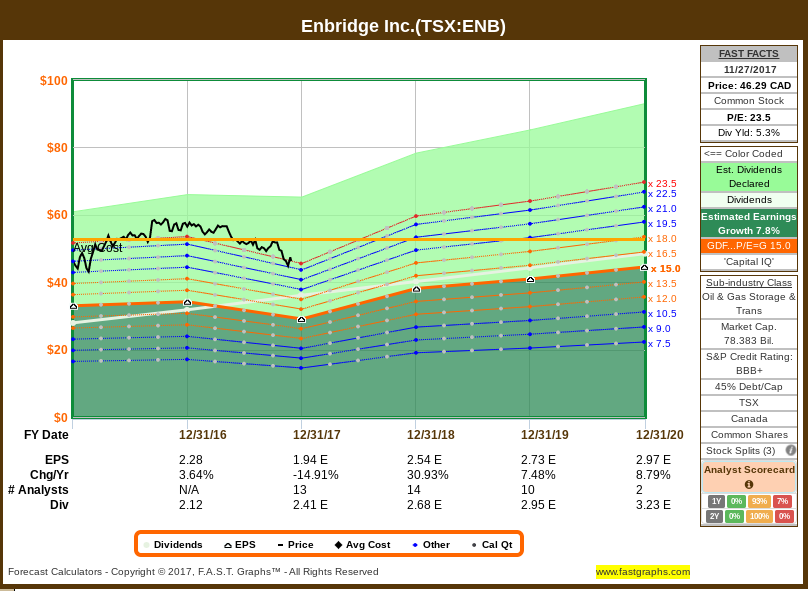

From a quality perspective, ENB continues to increase earnings and dividends in any market conditions, delivering impressive dividend growth and total returns to shareholders:

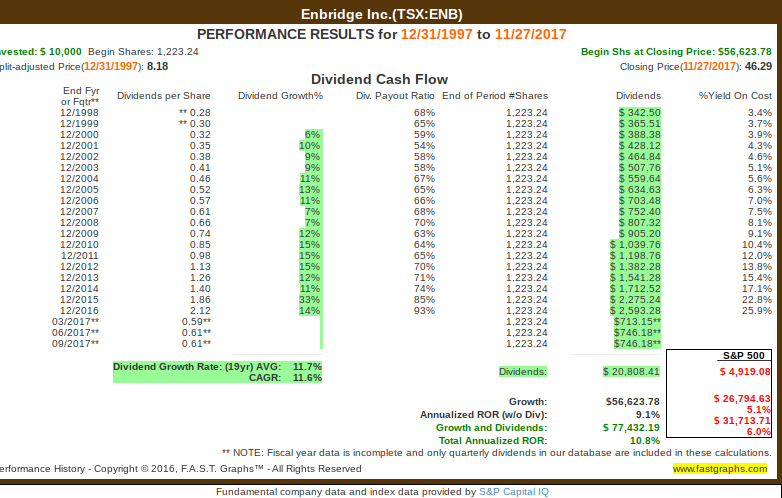

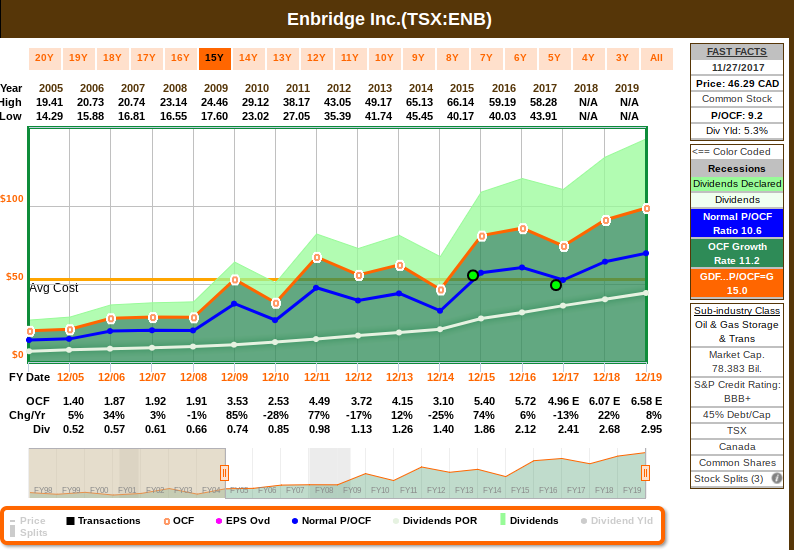

That said, we can notice that ENB’s price follow cash flow closely, and I rather use that as a valuation metric when making decisions to add more:

So why the poor performance lately? Enbridge’s $26B secured capital program of projects in execution combined with another $48 billion of projects under development is expected to translate into 12% to 14% ACFFO CAGR through 2019 and support DPS growth of 15% in 2017 and 10% to 12% from 2018 through 2024. These are impressive numbers. However, the market is nervous with results last quarter below consensus and therefore, regarding funding, with this negative sentiment amplified with the recent ENF’s rating one-step downgrade by Moody’s. Management has always been very clear about maintaining investment grade status, so the speculation is that dividend growth might slow down (or further equity raise might be required) in order to be able to keep a good investment rating. Also, management specifically redirect all questions related to this topic to Investor’s Day (coming up Dec 12 in NY and Dec 13 in Toronto), increasing the nervous sentiment.

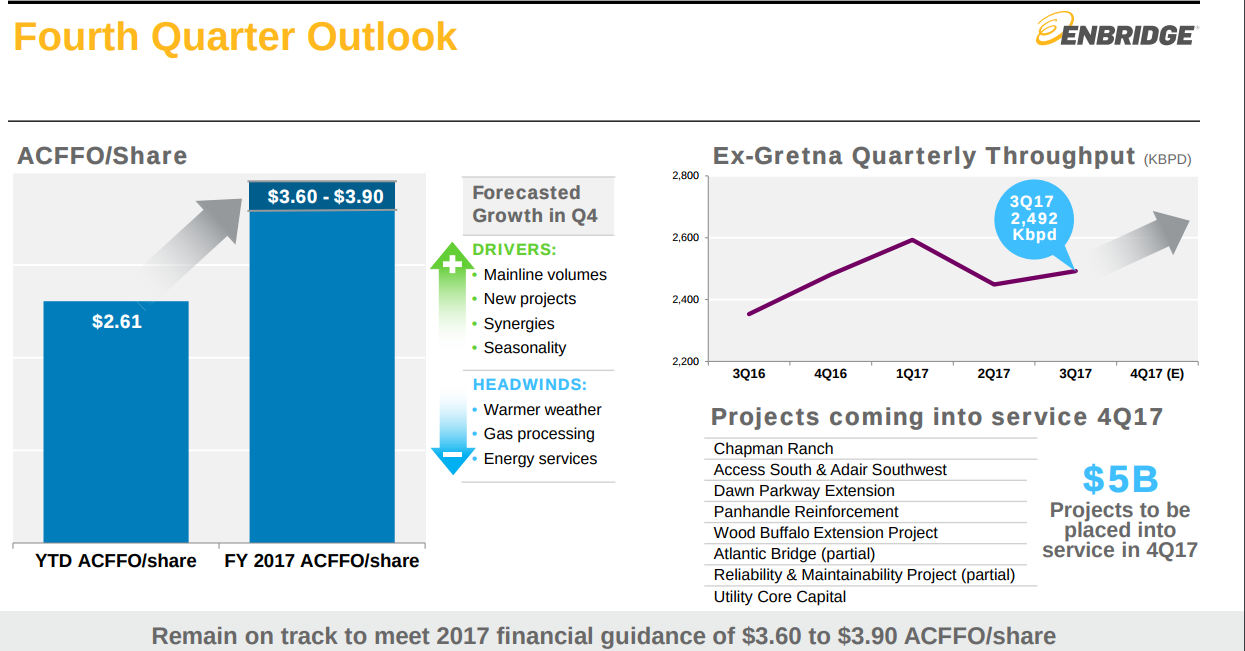

So I see the recent price drop as an opportunity to add further, which I have done last month, and might add more after the outcome for Investor’s Day become known. Enbridge continues to make progress on L3R, and 2017 guidance was reaffirmed, with the management continuing to expect $3.60-$3.90 of ACFFO/shar – although market conseus estimates a drop in earnings this year. This bring the current price aligned with fair valuation and in a position for excellent growth, given the raising estimates for earnings and cash flow for next year and 2 years after.

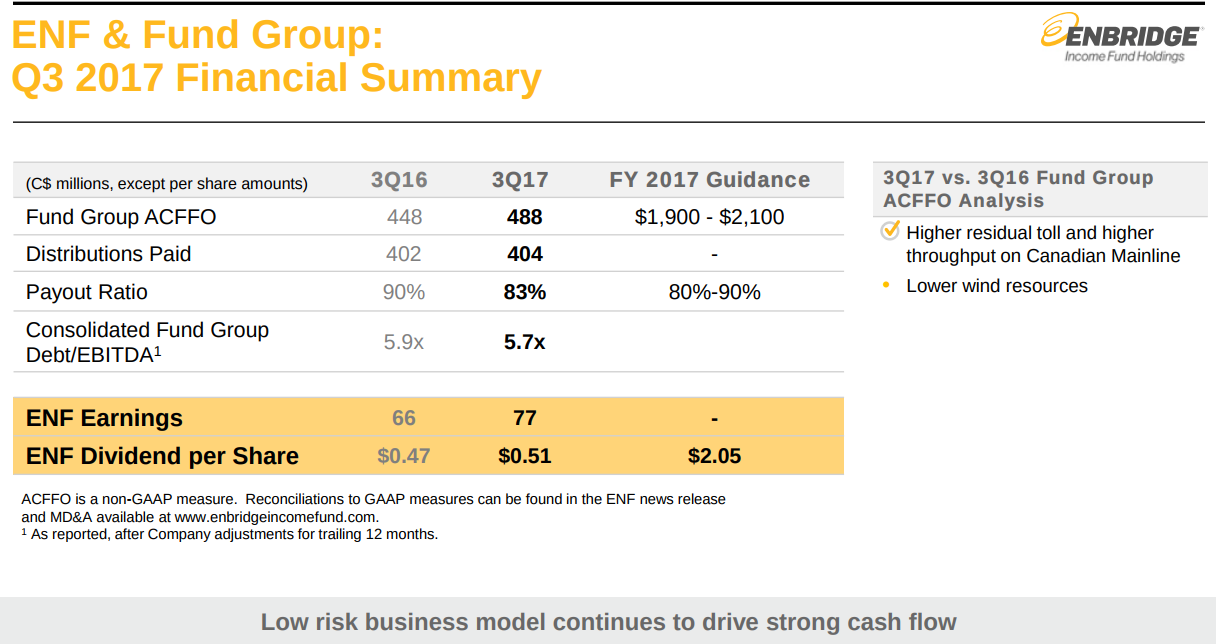

For ENF, the shares were further affected after Moody’s downgrade, but they always demonstrated resiliency given its low risk. For example, on the previous earnings call, ENF identified that it had another $5 billion-$6 billion of assets it could monetize. At $2.6 billion since the Spectra merger announcement, monetizations to date have already exceeded its initial $2 billion goal, indicative of the strength of the market for asset sales.

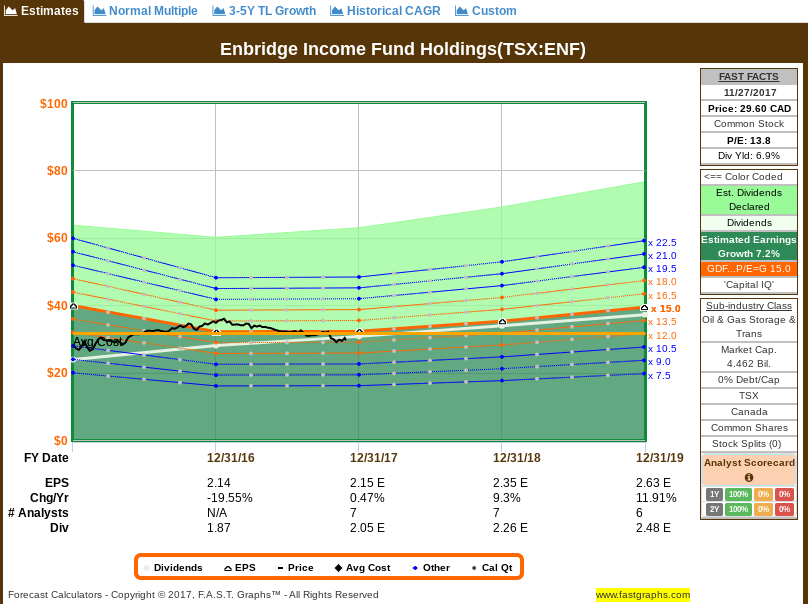

ENF results last quarter also came lighter than expected, due to higher power costs and foreign exchange rate, but cash flow is estimated to grow this year (and next year and the year after), considering that the Canadian portion of L3R is set to be approved and that the Wood Buffalo extension pipeline is expected to be placed into service by year-end. Management also reaffirmed 2017 guidance of $1.9 billion- $2.1 billion which was above street consensus estimates of $1.82 billion:

I believe both stocks (ENB and ENF) presents a great entry opportunity to own a business with a steady record on dividend, earnings and cash flow growth – not only looking at past growth, but also at future estimates, and corporate guidance:

I will also compare how much these numbers will change after Investor’s Day – nevertheless, it’s a great business to own at a great price right now.