Now that the Canadian DGI Portfolio for 2019 has been reviewed, it’s time to review the US DGI Portfolio. Moving forward, I will hold the US portfolio to a more stricter standard regarding dividend growth, because there are a lot of companies listed in the main US Exchanges with a very solid tracking record of earnings and dividend growth. So if dividend growth stalls for a few years and earnings are not improving, I will sell them and move to better opportunities.

Companies that no longer meet my goals for 2019:

The following companies on my US DGI Portfolio were removed for 2019:

Industrials:

DNB: Dun & Bradstreet announced last year that a definitive deal to go private via an investor group, so it will no longer be on my watchlist.

Consumer Discretionary:

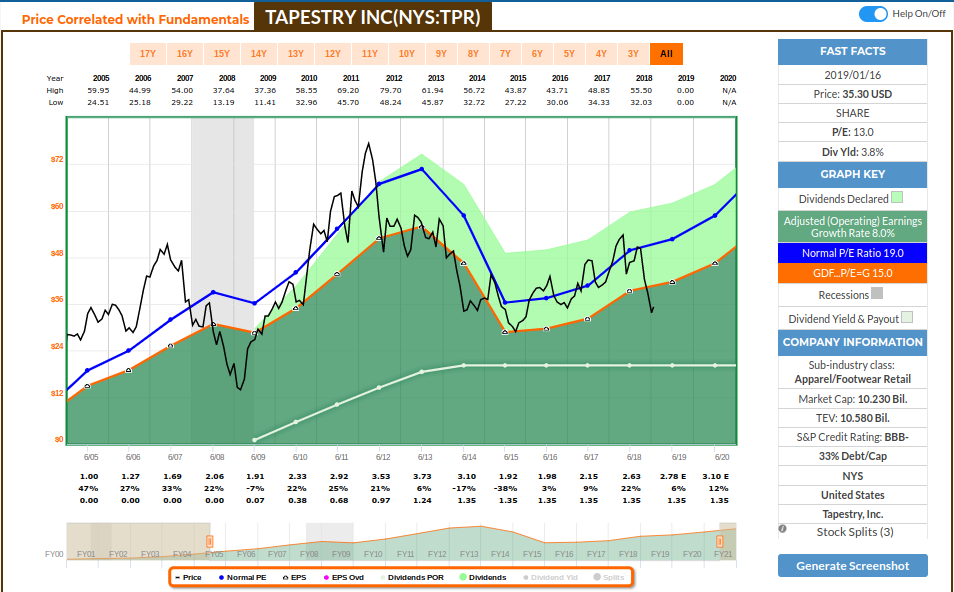

TPR: Tapestry hasn’t increased dividends since 2014, and the transformation from the Coach era has presented many challenges. I rather allocate capital to the companies that has shown their ability to continue to increase dividends.

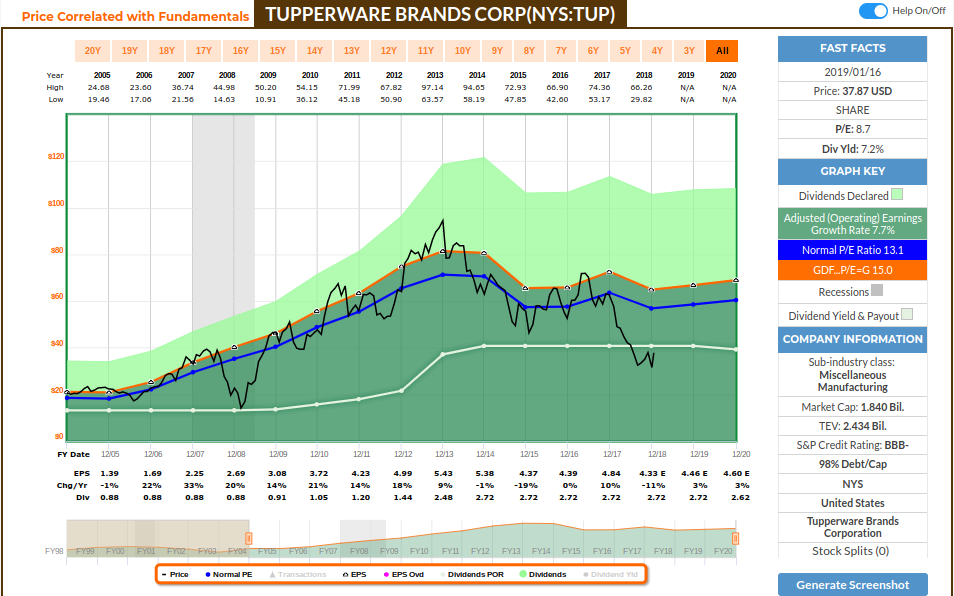

TUP: Tupperware also stopped growing dividends after 2014, and has been struggling to grow earnings and cash flow for some time.

Financials:

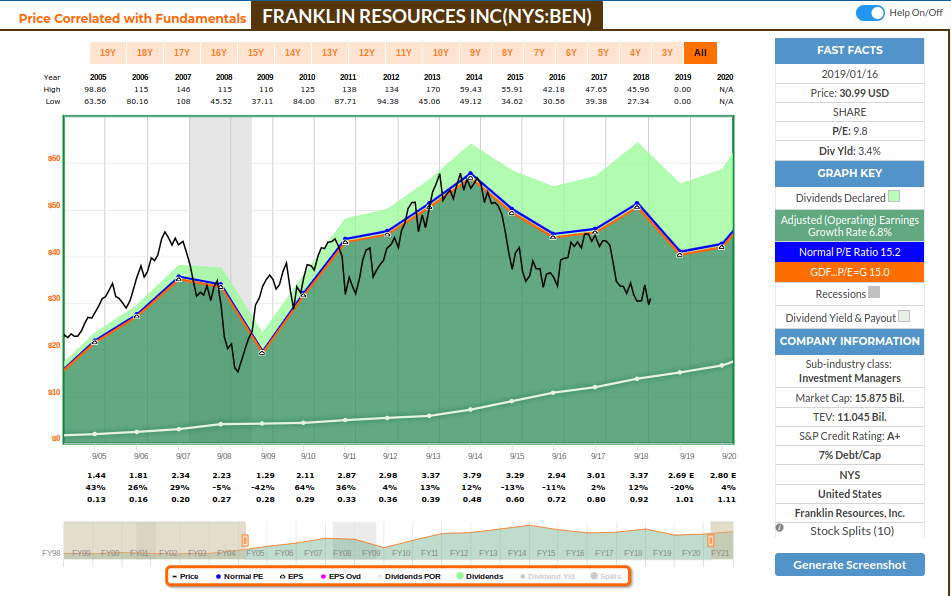

BEN: Ceasing the partnership with Franklin Resources was a difficult decision because they continue to grow dividends (and are estimated to continue to grow), but this is a tough industry that is changing, their operating performance and organic grow continues to deteriorate, revenue continues to drop and I want to hold my US portfolio to a more stricter standard given the number of companies on it. So considering that BEN hasn’t been able to make higher earnings since 2014, and that earnings are estimated to decline further this year, I decided to move on – the industry is changing, and we need to be aware that management needs to react and adapt quickly. ETFs are getting cheaper and more and more available to the mass, making BEN’s business model expensive and obsolete. Until they dominate their space again, I rather deploy capital to companies that continues to grow earnings and dividends (not just dividends) with all the recent changes and modernization. It’s important to note that BEN is a well managed company, their credit rating is excellent, and they go enough cash to take the time to handle these challenges and exceed again. But it’s been a business cycle since their last peak, so I think there are other opportunities without the industry risks that asset management are currently facing.

Technology:

DVMT: This is more of a cleanup item – I used to have EMC on my watchlist, and after Dell and EMC merged, they formed DVMT and they no longer pay a dividend, so I have removed them from my list.

.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.

Companies that I decided to partner with:

Besides deciding on the companies that no longer meet my goals, I also evaluate once a year which new companies I should partner with. In order to facilitate this process, I decided to further automate the screening process so it does most of the quality screening work for me, allowing me to evaluate further on a smaller list for the companies that was suggested through my initial automated quantitative analysis.

Remember that this process solely speaks to what to buy, but it doesn’t determine when to buy (which needs to take valuation into account). Let’s go through the “what” now, and I’ll later elaborate some of the “when”. I decided to partner with the following business:

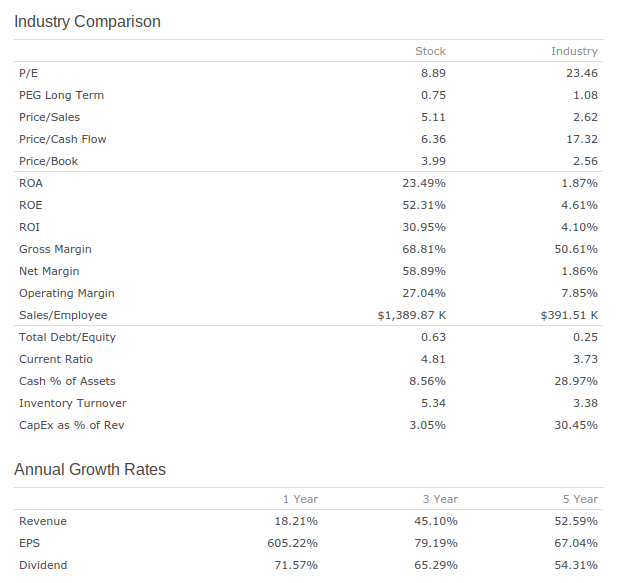

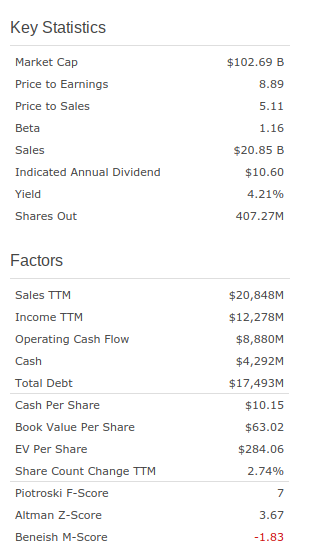

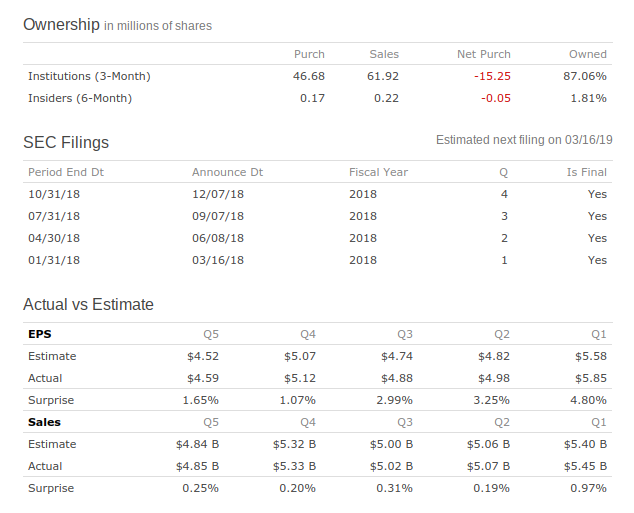

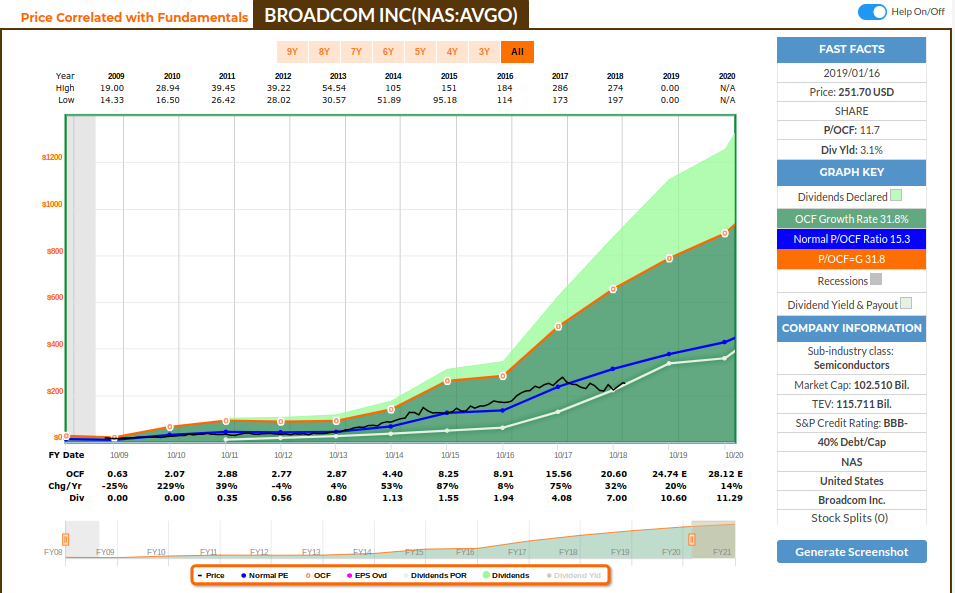

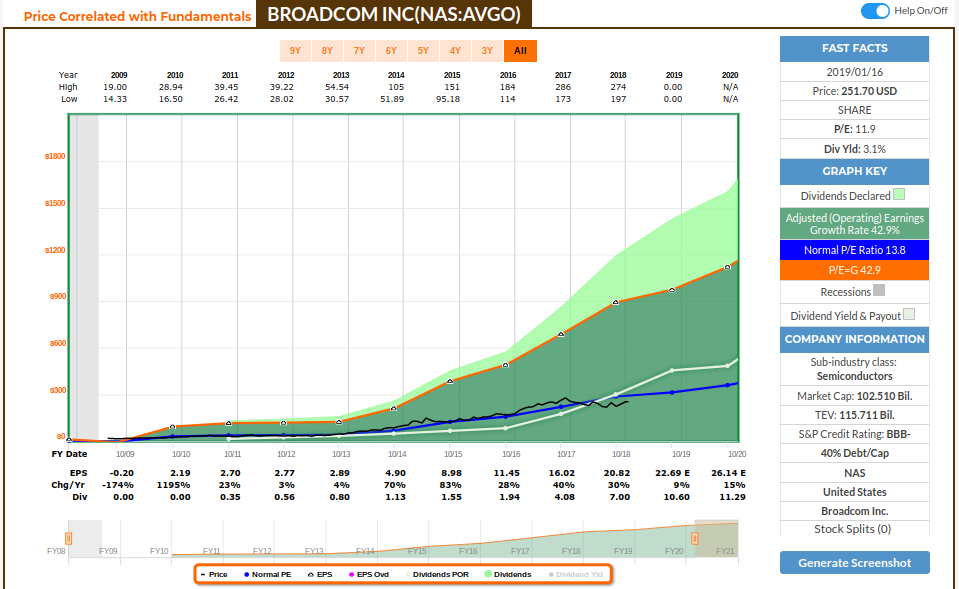

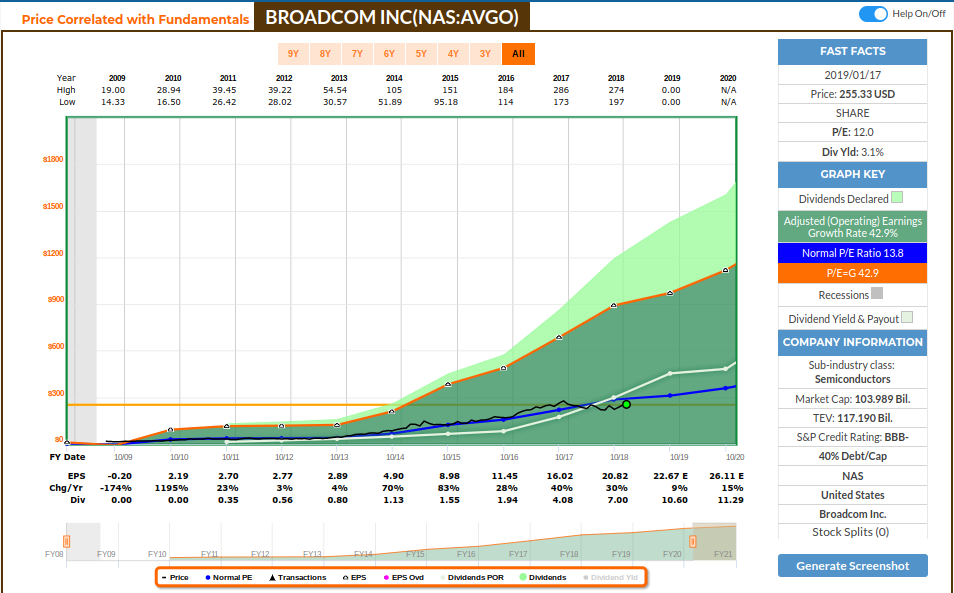

AVGO: Broadcom Inc. designs, develops, and supplies a range of semiconductor devices with a focus on complex digital and mixed signal complementary metal oxide semiconductor based devices and analog III-V based products worldwide. The company operates through four segments: Wired Infrastructure, Wireless Communications, Enterprise Storage, and Industrial & Other. The Wired Infrastructure segment provides set-top box system-on-chips (SoCs); cable, digital subscriber line, and passive optical networking central office/consumer premise equipment SoCs; Ethernet switching and routing application specific standard products; embedded processors and controllers; serializer/deserializer application specific integrated circuits; optical and copper, and physical layers; and fiber optic laser and receiver components. The Wireless Communications segment offers RF front end modules, filters, and power amplifiers; Wi-Fi, Bluetooth, and global positioning system/global navigation satellite system SoCs; and custom touch controllers. The Enterprise Storage segment provides serial attached small computer system interface, and redundant array of independent disks controllers and adapters; peripheral component interconnect express switches; fiber channel host bus adapters and switches; read channel based SoCs; custom flash controllers; and preamplifiers. The Industrial & Other segment offers optocouplers, industrial fiber optics, motion control encoders and subsystems, and light emitting diodes. The company’s products are used in various applications, including enterprise and data center networking, home connectivity, set-top boxes, broadband access, telecommunication equipment, smartphones and base stations, data center servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays. Broadcom Inc. is headquartered in San Jose, California..

Operating Cash flow:

Adjusted Operating Earnings:

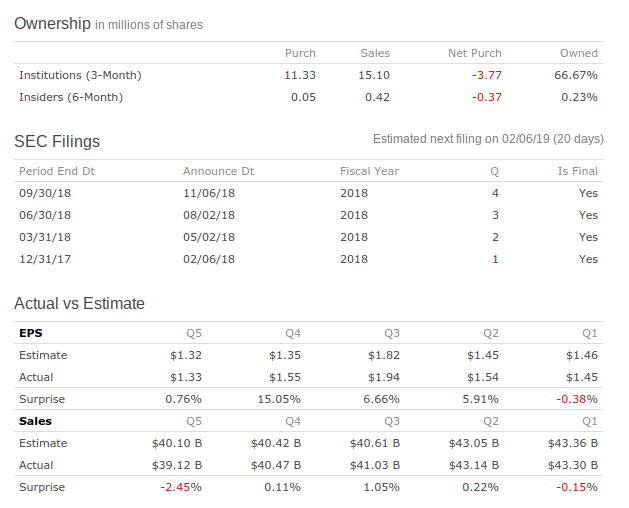

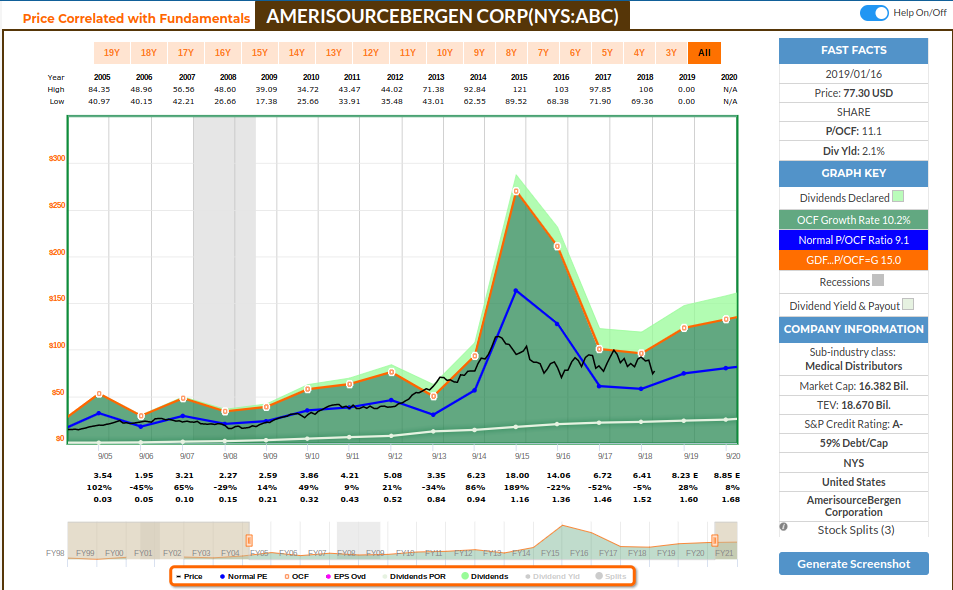

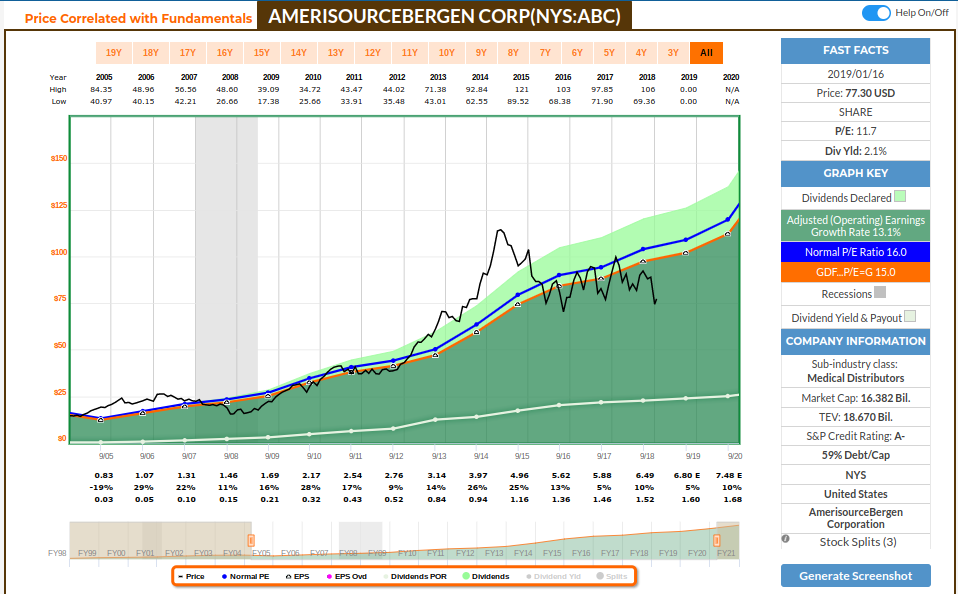

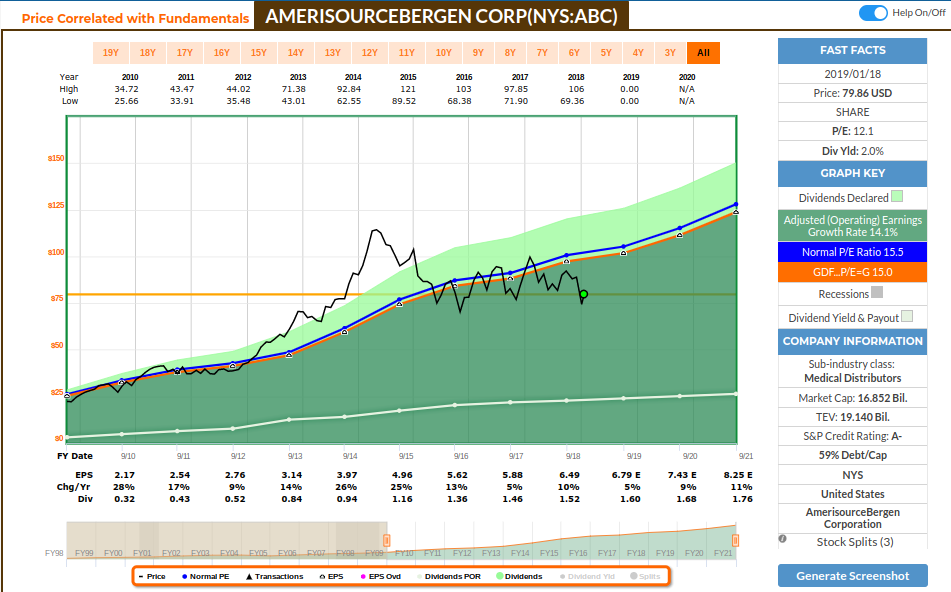

ABC: AmerisourceBergen Corporation sources and distributes pharmaceutical products in the United States and internationally. Its Pharmaceutical Distribution segment distributes brand-name and generic pharmaceuticals, over-the-counter healthcare products, home healthcare supplies and equipment, outsourced compounded sterile preparations, and related services to various healthcare providers, including acute care hospitals and health systems, independent and chain retail pharmacies, mail order pharmacies, medical clinics, long-term care and other alternate site pharmacies, and other customers. It also provides pharmacy management, staffing, and other consulting services; supply management software to retail and institutional healthcare providers; and packaging solutions to various institutional and retail healthcare providers. In addition, this segment distributes plasma and other blood products, injectable pharmaceuticals, vaccines, and other specialty products; provides other services primarily to physicians who specialize in various disease states, primarily oncology, as well as to other healthcare providers, including hospitals and dialysis clinics; and offers data analytics, outcomes research, and additional services for biotechnology and pharmaceutical manufacturers. The company’s Other segment provides integrated manufacturer services, such as clinical trial support, product post-approval, and commercialization support; offers specialty transportation and logistics services for the biopharmaceutical industry; and sells pharmaceuticals, vaccines, parasiticides, diagnostics, micro feed ingredients, and various other products to customers in both the companion animal and production animal markets, as well as provides demand-creating sales force services to manufacturers. AmerisourceBergen Corporation was founded in 1985 and is headquartered in Chesterbrook, Pennsylvania.

Operating Cash Flow:

Adjusted Operating Earnings:

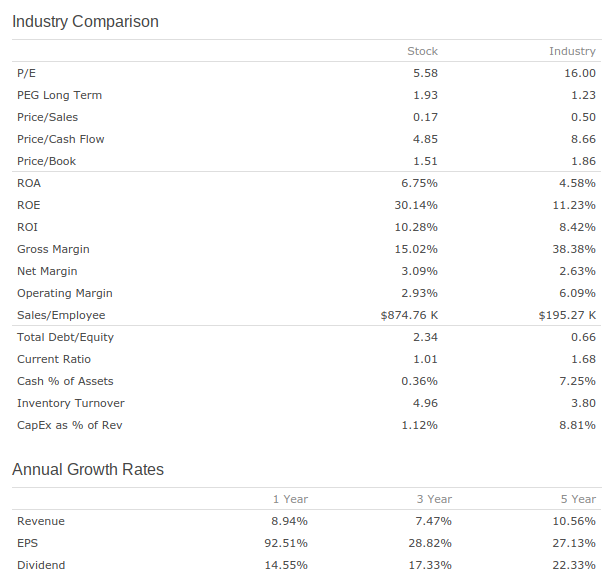

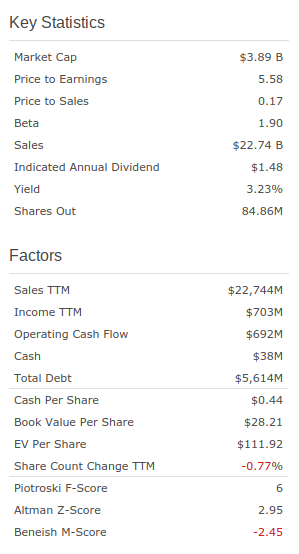

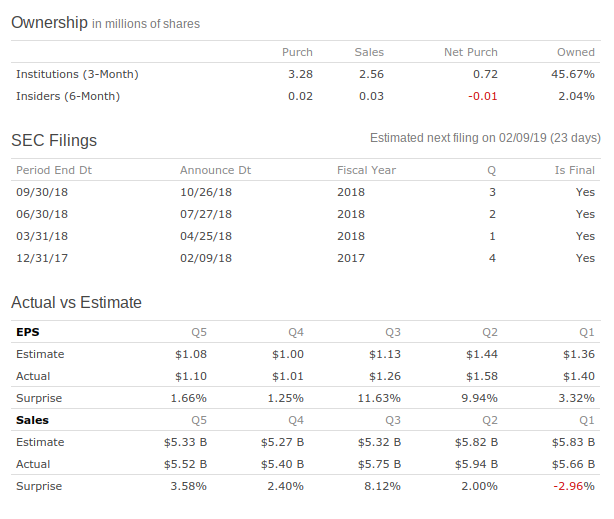

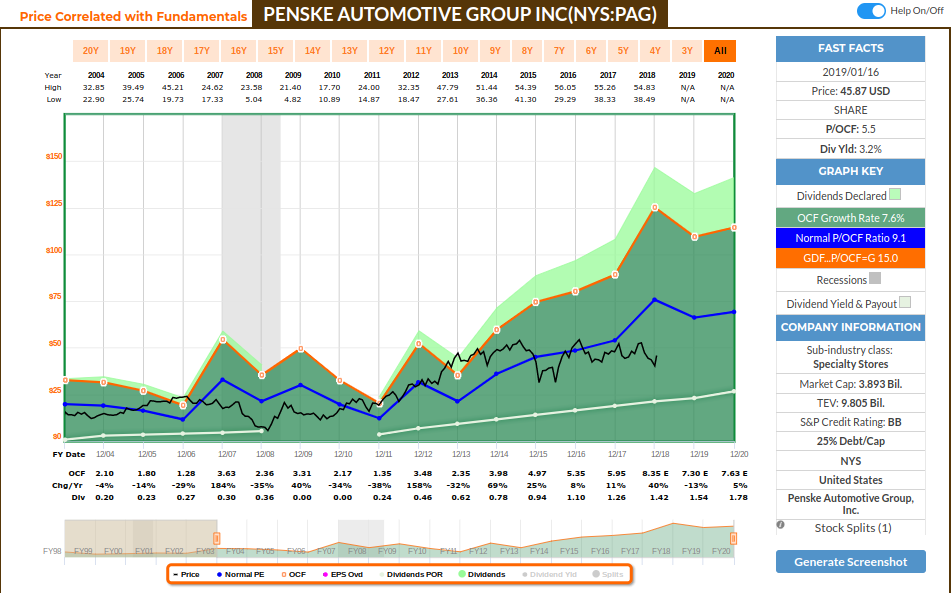

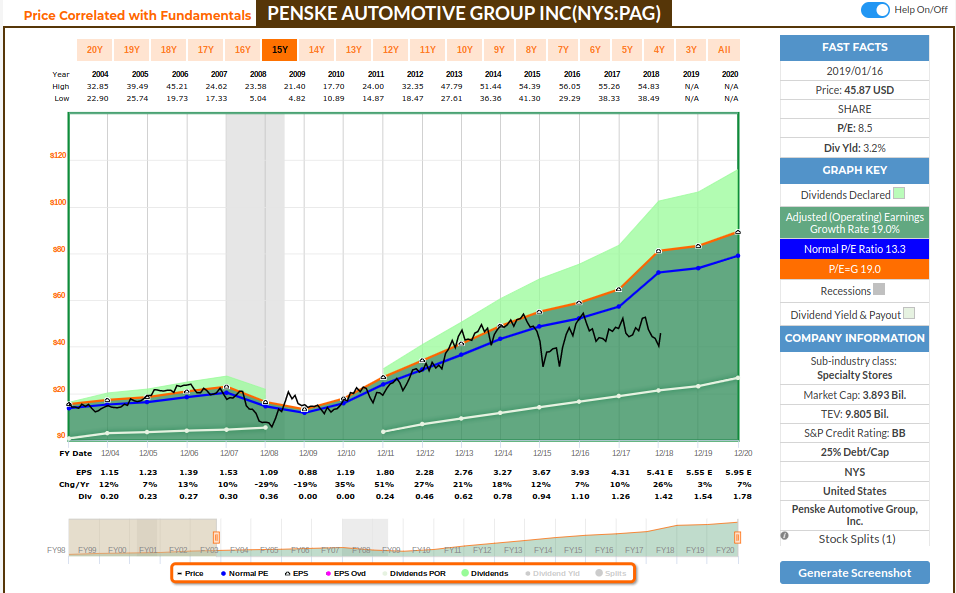

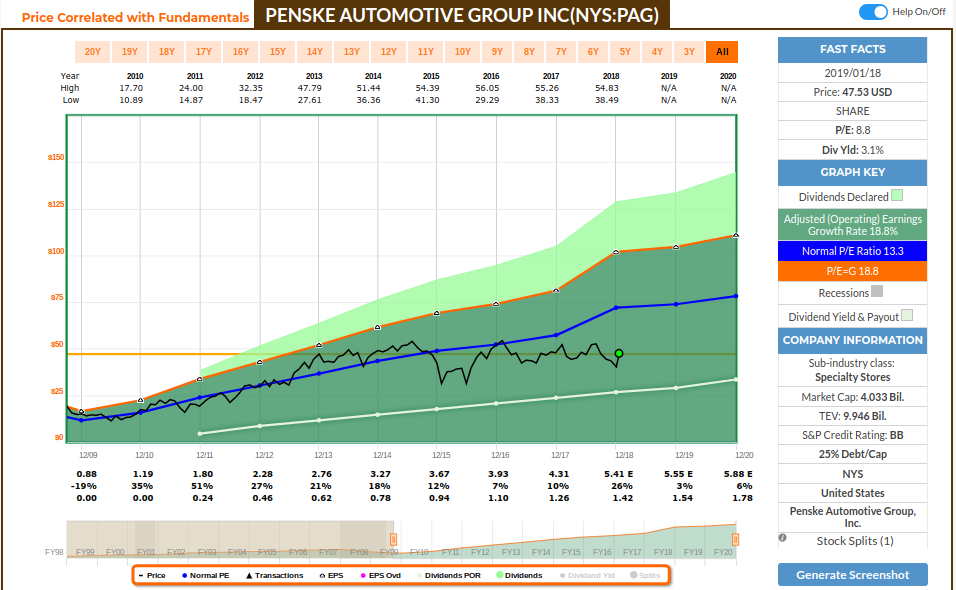

PAG: Penske Automotive Group, Inc. operates as a transportation services company. The company operates through four segments: Retail Automotive, Retail Commercial Truck, Other, and Non-Automotive Investments. It operates automotive and commercial truck dealerships principally in the United States, Canada, and Western Europe; and distributes commercial vehicles, diesel engines, gas engines, power systems, and related parts and services primarily in Australia and New Zealand. The company engages in the sale of new and used motor vehicles of approximately 40 brands; and provision of vehicle services and collision repair services. In addition, it is involved in the sale and placement of third-party finance and insurance products, third-party extended service and maintenance contracts, and replacement and aftermarket automotive products. Further, the company distributes commercial vehicles and parts to a network of approximately 70 dealership locations, including 8 company-owned retail commercial vehicle dealerships. As of December 31, 2017, it operated 343 automotive retail franchises, of which 155 franchises are located in the United States; and 188 franchises are located outside of the United States primarily in the United Kingdom. The company also operated 20 dealerships locations of heavy and medium duty trucks, offering primarily Freightliner and Western Star branded trucks, as well as a range of used trucks, and services and parts. Penske Automotive Group, Inc. is headquartered in Bloomfield Hills, Michigan.

Operating Cash Flow:

Adjusted Operating Earnings:

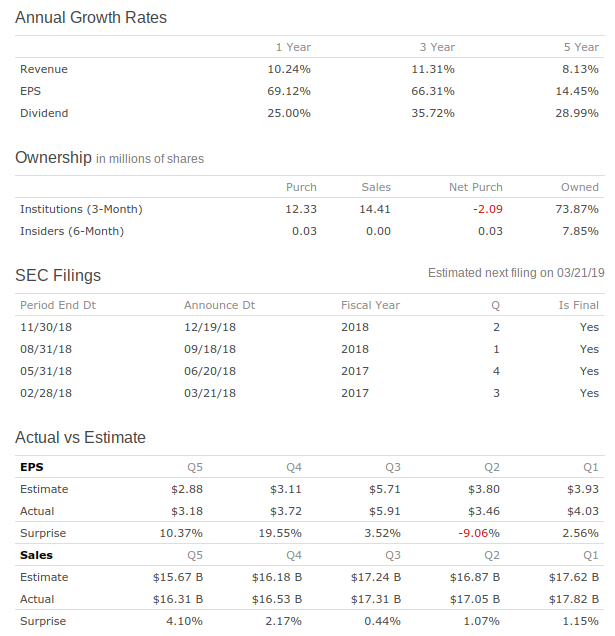

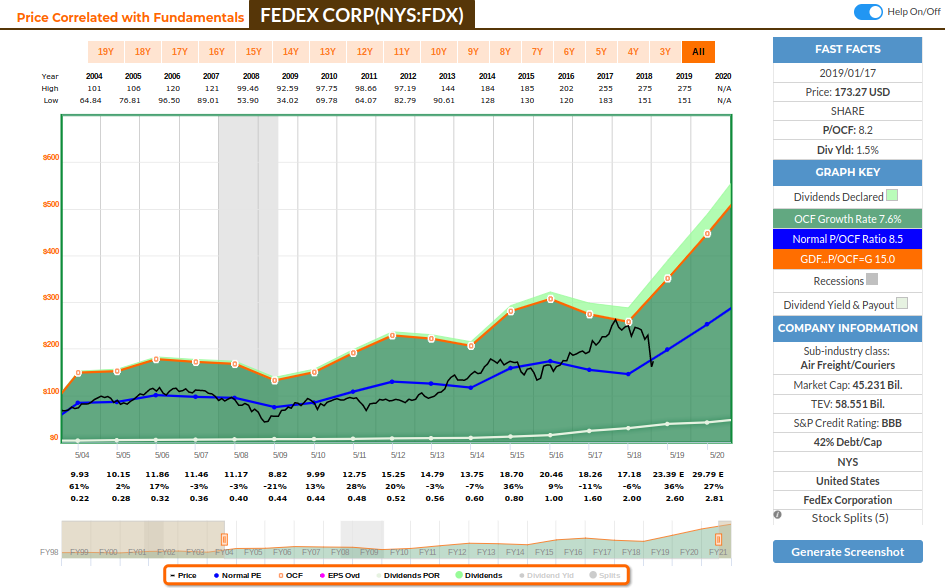

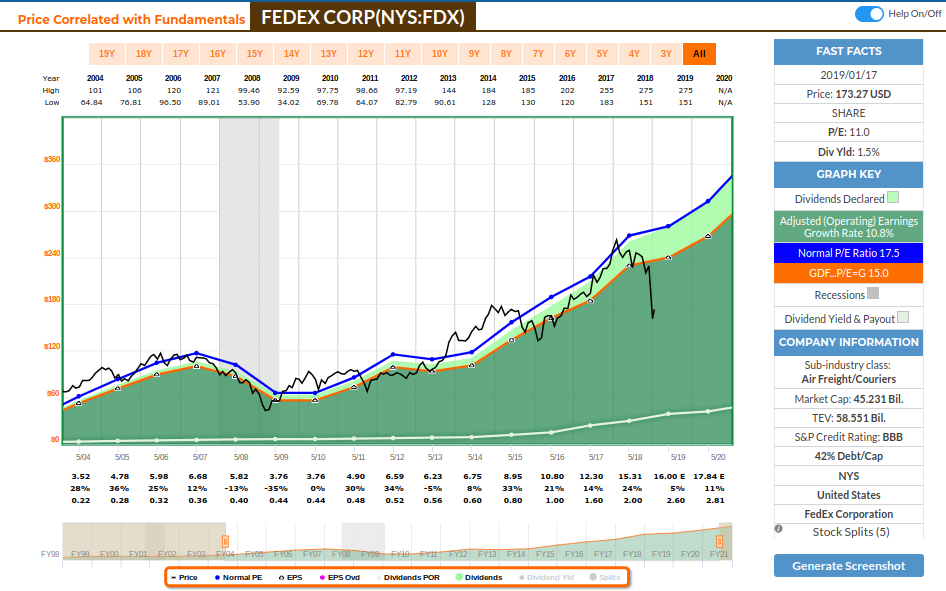

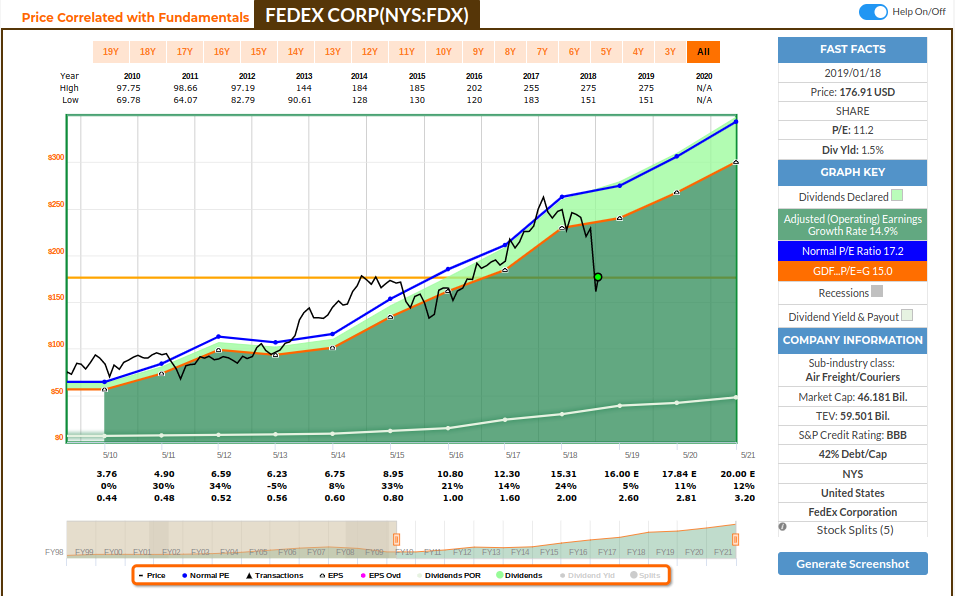

FDX: FedEx Corporation provides transportation, e-commerce, and business services worldwide. The company’s FedEx Express segment offers shipping services for delivery of packages and freight. Its FedEx Ground segment provides business and residential money-back guaranteed ground package delivery services; and consolidates and delivers low-weight and less time-sensitive business-to-consumer packages. The company’s FedEx Freight segment offers less-than-truckload and freight delivery services. As of May 31, 2018, it operated approximately 27,000 vehicles and 370 service centers. The company’s FedEx Services segment provides sales, marketing, information technology, communications, customer, technical support, billing and collection, and other back-office support services. It also offers FedEx Mobile, a suite of solutions to track packages, create shipping labels, view account-specific rate quotes, and access drop-off location information; FedEx Office, a suite of printing and shipping management solutions for copying and digital printing, professional finishing, document creation, direct mail, signs and graphics, computer rentals, Wi-Fi, and corporate print solutions; and packing services, supplies, and boxes, as well as FedEx Express and FedEx Ground shipping services. The company’s Corporate, Other and Eliminations segment offers international trade services in customs brokerage, and ocean and air freight forwarding services; cross-border enablement and technology solutions, and e-commerce transportation solutions; integrated supply chain management solutions; time-critical shipment services; critical inventory and service parts logistics, 3-D printing, and technology repair. This segment also provides international trade advisory services, including assistance with the customs-trade partnership against terrorism program; and publishes customs duty and tax information. FedEx Corporation was founded in 1971 and is headquartered in Memphis, Tennessee.

Operating Cash Flow:

Adjusted Operating Earnings:

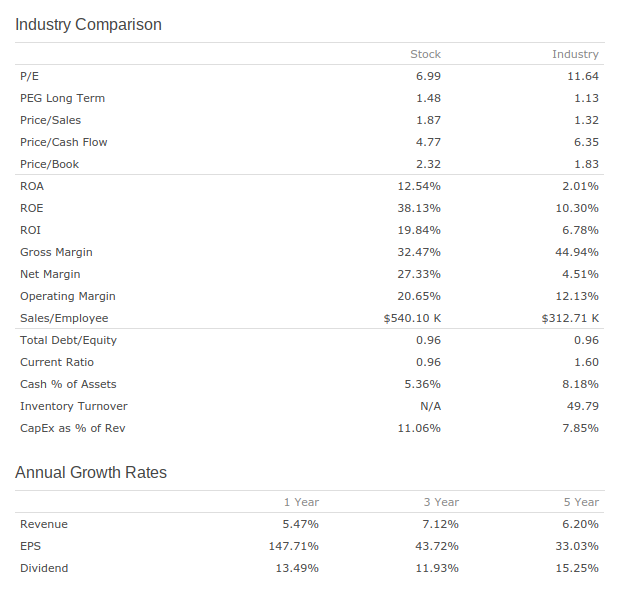

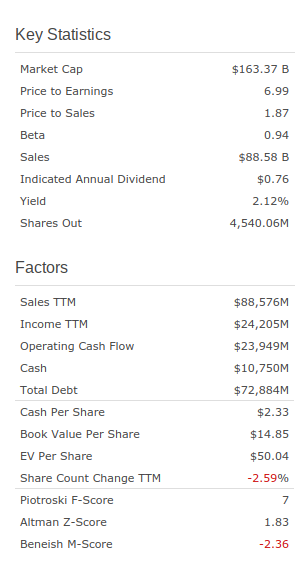

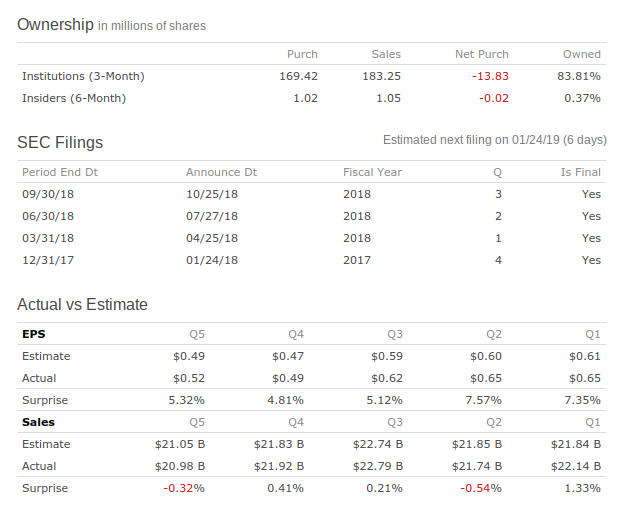

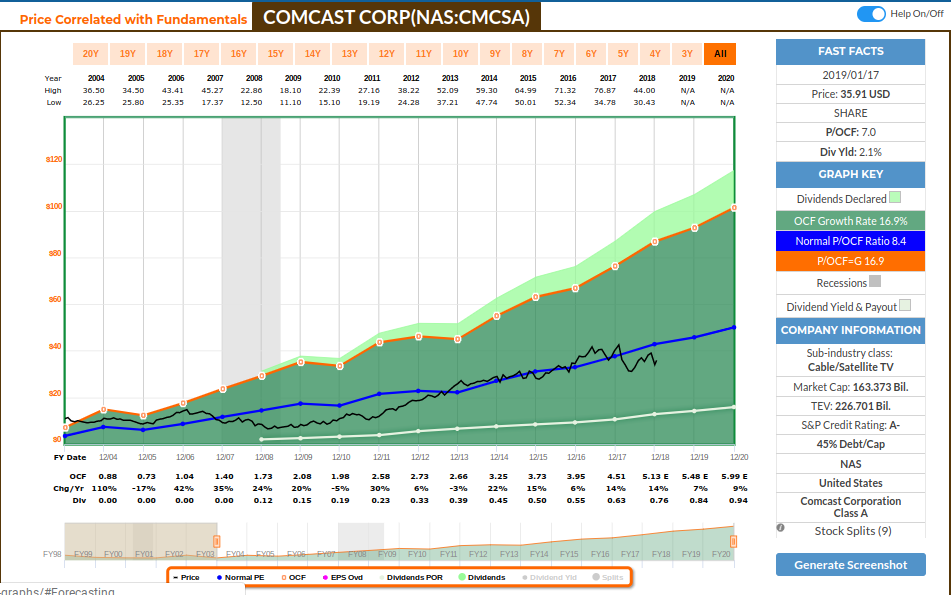

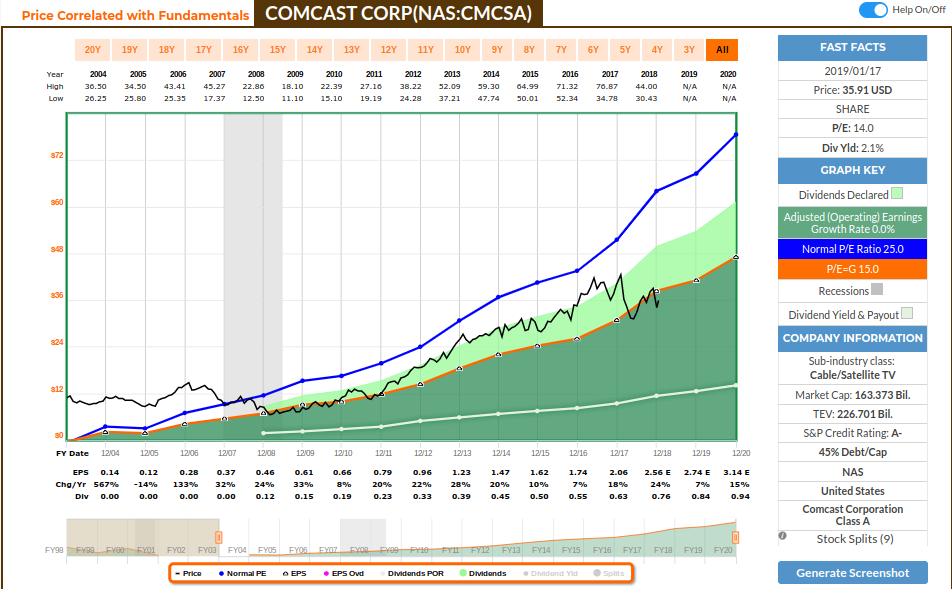

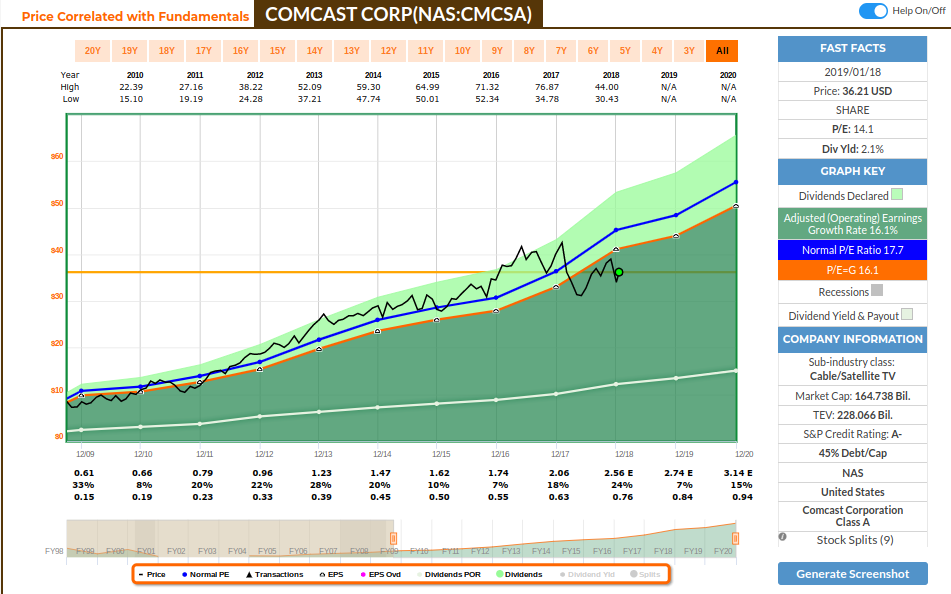

CMCSA: Comcast Corporation operates as a media and technology company worldwide. It operates through Cable Communications, Cable Networks, Broadcast Television, Filmed Entertainment, and Theme Parks segments. The Cable Communications segment offers video, high-speed Internet, and voice, as well as security and automation services to residential and business customers under the XFINITY brand. This segment also provides business services, such as Ethernet network services; and cellular backhaul services to mobile network operators. The Cable Networks segment operates national cable networks, which provide entertainment, news and information, and sports content; regional sports and news networks; international cable networks; and cable television studio production operations, as well as owns various digital properties, which include brand-aligned Websites. The Broadcast Television segment operates NBC and Telemundo broadcast networks, NBC and Telemundo local broadcast television stations, broadcast television studio production operations, and various digital properties. The Filmed Entertainment segment produces, acquires, markets, and distributes filmed entertainment under the Universal Pictures, Illumination, Focus Features, and DreamWorks Animation names. This segment also develops, produces, and licenses stage plays; and distributes filmed entertainment produced by third parties. The Theme Parks segment operates Universal theme parks in Orlando, Florida, as well as in Hollywood, California; and Osaka, Japan. The company also owns the Philadelphia Flyers, as well as the Wells Fargo Center arena in Philadelphia, Pennsylvania; and operates arena management-related businesses, as well as provides wireless phone services. Comcast Corporation was founded in 1963 and is headquartered in Philadelphia, Pennsylvania.

Operating Cash Flow:

Adjusted Operating Earnings:

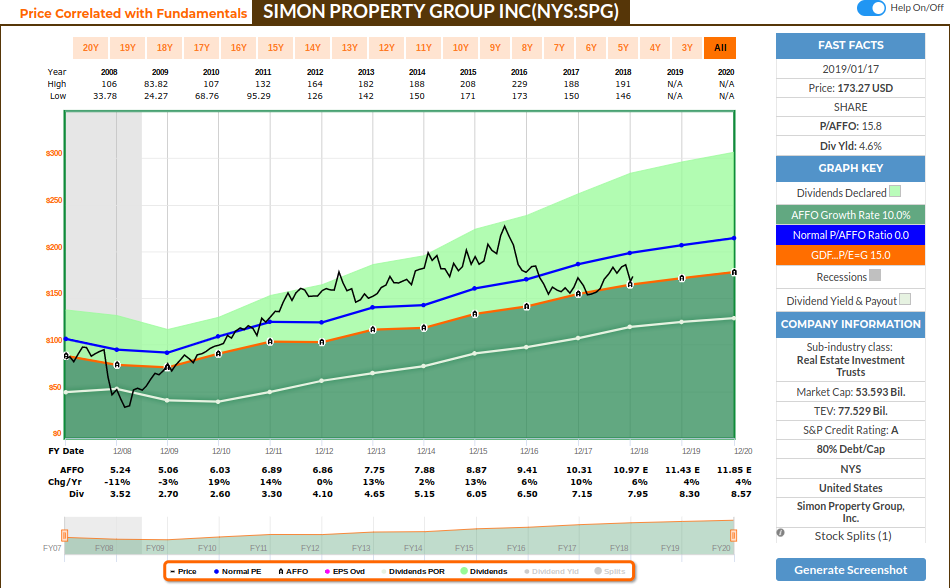

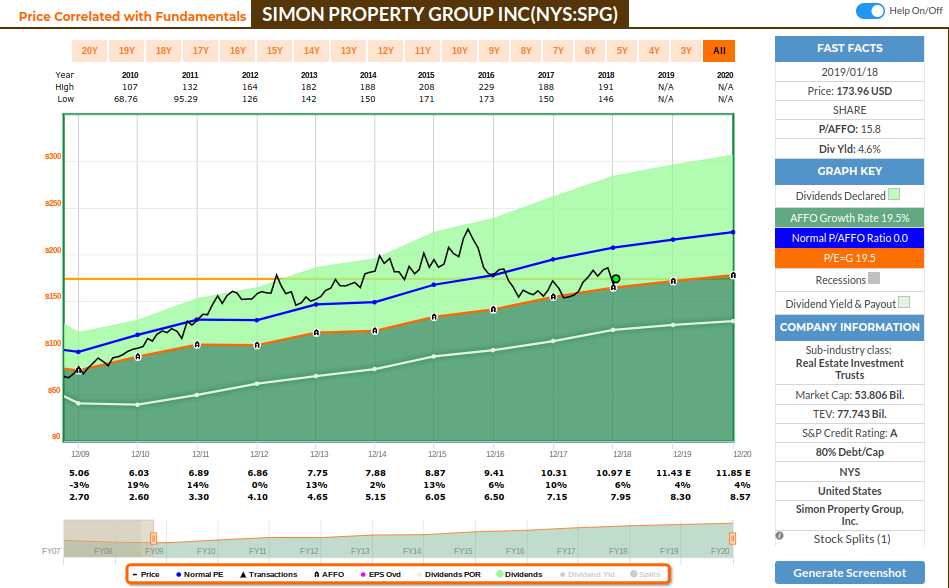

SPG: Simon Property Group, Inc. is an American commercial real estate company, the largest retail real estate investment trust (REIT), and the largest shopping mall operator in the US. The company operates five retail real estate platforms: regional malls, premium outlet centers, The Mills, community/lifestyle centers and international properties. It owns or has an interest in more than 325[4] properties comprising approximately 241,000,000 square feet (22,400,000 m2) of gross leasable area in North America and Asia. The company is headquartered in Indianapolis, Indiana.

Adjusted Funds From Operations:

The companies that I bought this month:

The companies from my watchlist should be purchased when price is attractive, which is a process taking valuation (not price alone) into account. The watchlist speaks to “what” to buy. The valuation process speaks to “when” to buy.

For this month, I purchased the following companies. My last purchase was in October, and I typically save $2,000 per month, so that allowed me to save $6,000. Plus, I will be reinvesting the dividends from 2018 ($1,203.23), which will give me a total of $7,203.23 to be invested this month.

I chose 6 companies to start new positions, so I’ll be allocating $1,200.54 for each company. The investing performance spreadsheet has been updated accordingly, including the information related to the companies that increased dividends this year so far.

The US portfolio is not as diversified as the Canadian one, so I want to broad the exposure to other companies, which has a reasonable initial yield, but more importantly, which is estimated to grow that dividend, earnings and cash flow at a higher pace than the market in general, so that these gains can compound overtime.

I’ve added positions / initiated new positions on the following stocks, allocating the amount specified above:

Broadcom Inc: Broadcom is a growth company that has a decent yield and is scheduled to continue to grow that dividend at a high pace. Broadcom continues to be well positioned in a growing market (high-end smartphones), as a third of their sales come from the RF filters, a critical component to ensure that premium smartphones with LTE enabled (such as Apple’s iPhone) operate efficiently in a congested wireless network. 4G and 5G LTE is growing, so this is estimated to grow further as these components remain critical and require to evolve. Broadcom also leads the network segment with several product, growing by acquisition of several innovative companies. As a serial acquirer, Broadcom has mastered the process of purchasing semiconductor companies with best-of-breed products at attractive valuations, trimming non-core product lines to streamline the business, and ultimately driving nice cost synergies.

AmerisourceBergen: AmericesourceBergen is estimated to continue to grow earnings and dividends, so the recent price decline, partially by recent mixed results regarding distribution operations, presents a great opportunity. They just finished the integration of Rite Aid and are well position to continue to grow, as AmerisourceBergen is one of three large pharmaceutical

distributors and is the main supplier to large pharmacy outlets Walgreens and Express Scripts’ mail order pharmacy. AmericesourceBergen has a highly integrated strategic agreement with Walgreens where it supplies all of the retail pharmacy’s drug inventory, including generics. This last aspect is key: supplying higher-margin generic drugs to one of the biggest generic drug retailers outlets is a major positive for profits, capital efficiency, and invested capital returns.

Penske Automtive: I like how Penske Automative earnings have been growing lately (and estimated to continue to grow) and the stock hasn’t gone anywhere in the last 3 years. As a buyer, I want lower prices while the company continues to post higher operating performance. Dealerships are stable businesses, as they profit from car sales, parts and services. Penske has moved into heavy-truck distribution in Australia and New Zealand, truck dealers in the U.S., and used-vehicle stores in the U.S. and U.K. It’s important to notice that Penske Automotive can have very erratic earnings, as dealership businesses are cyclical, but the company mitigates this risk by selling highly profitable repair and warranty services, which allow dealers to enjoy mid- to high-single-digit gross margins on new vehicles and 100% gross margins on financing and insurance. Even if auto-sale slows down, I think that entering now has a decent margin of safety with a reasonable dividend that has been increased for years, and it’s estimated to continue to increase.

FedEx Corp: FedEx became very undervalued due to the recent concerns on global trading and political interference. Their business is capital intensive (they have one of the world’s largest airlines), and the recent slowdown in Europe after acquiring TNT isn’t helping their results on that front. However, they have few competitors and their massive size prevents new companies to attempt to compete; It’s only a matter of time to reap the fruits from acquiring TNT, and during its nearly five-decade history, FedEx has weathered multiple economic cycles and oil supply crises. While short-term results may suffer, Fedex continues to grow earnings and dividends and solidify their presence. Looking forward, FedEx sees strength in the U.S. and expects overall growth to be positive but slower than in recent periods. Even with a slower growth, they are presently undervalued, so I think a position now represents a good opportunity on what I expect their future intrinsic value to be.

Comcast Corp: Comcast is a solid core cable business company, an area that will continue to grow as the world relies more and more on the Internet. Comcast will be launching a new streaming service next year, adding competition to Netflix and in the short future, Disney+. The biggest players on the cable network space are AT&T, Verizon and Comcast, so a portfolio with these 3 players provide good coverage and diversification. Comcast has leveraged its network advantage to enter the business services market, beginning with small businesses a decade ago and then steadily increasing the size and complexity of the customers it can serve. Comcast has invested about $7.5 billion of incremental capital into its network over the past 10 years to reach this market, creating a business that generates more than $7 billion in annual revenue and continues to grow at a double-digit pace while delivering better margins than residential services. Comcast believes that the business services

opportunity in its footprint equals about $40 billion in annual revenue and that it has gained about 40% small business share, 10% medium business share, and less than 5% large enterprise share. Comcast’s acquired Sky, which should drive further growth: Sky is the U.K.’s largest pay television operator, with 13 million retail subscribers, equal to about 45% of the households and more than twice the number of cable customers in the country. Sky is also the dominant pay television provider in Italy, Germany, and Austria, although the pay television markets in these countries are less developed. Sky has also

launched service offerings in Spain and Switzerland, and it’s following the same strategy in these markets as it has in the U.K., building proprietary content. Comcast strong position as business, associated with estimated earnings and dividends to grow, while price has recently declined provide another good opportunity for the long term.

Simon Property Group : Simon Property Group, the largest mall real estate investment trust and second-largest U.S. REIT, manages one of the top retail portfolios in the US. It owns and operates Class A traditional regional malls and premium

outlets in markets with dense populations and high incomes; these malls frequently have domestic or international tourist appeal. The high-quality properties will continue to provide consumers with unique shopping experiences that are hard to replicate elsewhere, even though online retailers continue to pressure brick-and-mortar retailers. Their results continue to impress, with growing retail sales, and an occupancy rate of 95.5%, and funds from operations and NOI continue to grow. Simon’s properties are strategically located in areas with high disposable income, and it’s tailored for both consumers and retailers. REITs are a great way to have exposure to real estate without the drawbacks of managing one ourselves, and it’s a great contributor for dividend growth and higher portfolio income. I believe Simon Properties is fairly valued considered their future growth and present valuation, while providing a reasonable dividend that is estimated to continue to grow.

Other companies on my watchlist are fairly valued or undervalued. However, the companies mentioned above are positioned for a decent growth of earnings and dividends, and since reliability of income growth is paramount to a DGI portfolio, I’m diversifying my US portfolio further before adding to existing positions.

Happy Investing!

Hi Rod,

Do you plan to continue posting your purchases and list of fairly valued/undervalued companies?

Yes! I’ve just been very busy with some other projects, but I will post soon.

Thanks. I look forward to it. Your analysis and process is very helpful for new investors like myself.

Thank you for all the details. I definitely have a lot more to learn. Not sure if the charts I was looking at was giving the right information, because it showed PE increasing over the years.

Hi Rod, you always talk about how price follows earnings. I am interested in investing in Pepsico, which you have purchased and recommended in the past. I was looking at the PE noticed that the price keeps going up but not the earnings. Are there other things that I am clearly not taking into account? I am new to analysis.

https://www.macrotrends.net/stocks/charts/PEP/pepsico/pe-ratio

No, their operating earnings keep growing:

Their P/E ratio hasn’t changed much, hence so we see a trend of price following earnings. It was a bit overvalued a few years ago, but it’s coming to a more reasonable valuation now. Earnings and dividends are estimated to continue to grow.

This is just an initial analysis regarding valuation. You should take into account analysts estimates, how many analysts are covering the company (the more you have, the better is the consensus), how that compares to corporate guidance, and what is the analyst scorecard (it tells how well they understand and predict operating results for that business). Earnings calls have good insight on where they are with their strategy, strengths and weaknesses. Lastly, different timeframes help to plot a more reasonable multiple aligned to past operating growth and future (estimated) growth. I typically like 10 year time frame (8 years past plus 2 forecast). It covers about 2 business cycles. It’s not guaranteed, because forecast is unknown (it’s based on the information that we have today), but it adds enough components to help us make an informed decision regarding what the intrinsic value of the business is today and what is estimated to be in the future. When you buy a stock, you buy the earnings potential for that business. Hence it takes time to know if you made a good decision buying today, and why investing is for long term. Pepsi is a great quality company that is presently fairly valued and estimated to grow, in my opinion.