Every year I do an annual review of the companies that I’m invested on. You can find the review for my Canadian portfolio here. This post is to review the companies on my US portfolio for 2018. As I mentioned before, this review is not based on stock price performance. Instead, I evaluate the business’s operating results, their cash flow and potential impact to dividend to ensure that it still meets my quality criteria. If the business has changed to a point that it no longer meet my goals, then I sell and “cease the partnership”, which means that this company won’t be on my watchlist for a few years at least, until they improve results and meet my goals again.

For the US portfolio, the following companies are no longer on my list:

Companies that no longer exist / meet my needs:

BCR: C.R.Bard Inc (BCR) was acquired by Becton Dickinson and Co (BDX), so BCR stock no longer exists. BDX was already on my watchlist.

BCR wasn’t purchased for the portfolio that I’m tracking on this website.

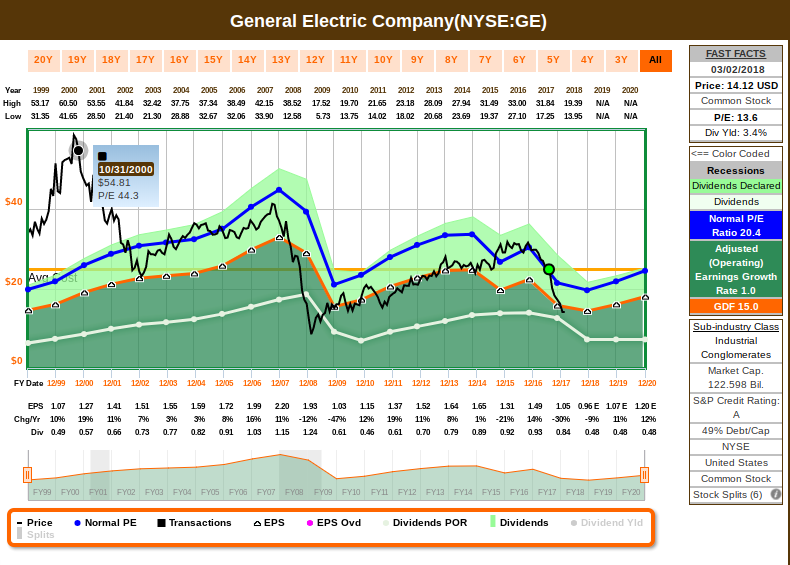

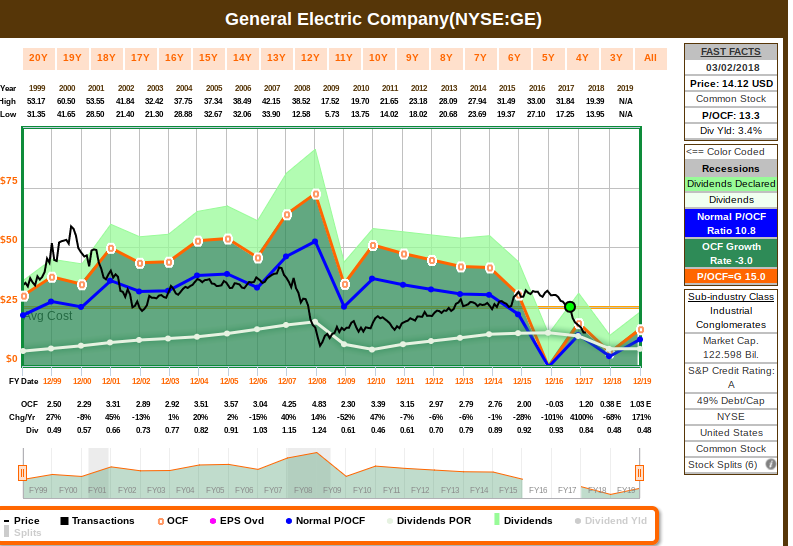

GE: GE reduced their dividend payment during 2 business cycle period, so it no longer meet my goals for dividend growth. Since divesting GE Financial and the methodologies used pre-2008 era, earnings haven’t been at par with how the company used to perform, and the recent findings are concerning – management seems to be doing the right things to strength cash flow, but I think that transformation / fix will take time and cash can be better deployed somewhere else. Like many companies that got hit hard in 2008, I expected a slow but steady recovery. GE never recovered to previous levels and the future estimates are not attractive for my goals.

As side note, I’d like to stretch the importance of buying companies at a sound valuation. No one could predict that GE would have the performance that we see in the graph above. But it’s very clear that in 1999 and 2000 GE was trading at a very high valuation. Purchasing a stock with valuation in mind helps to increase the margin of safety, as the company’s intrinsic value would have to fall drastically below present values – if it posses good quality metrics, it’s unlikely to happen. Unlikely doesn’t mean impossible, and with GE, it did happen. But that’s why a diversified equity portfolio is paramount to mitigate risks – this same methodology worked for all other companies that continue to do well. There will always be failures, but the winners will far outweight the losers, bringing anyone’s portfolio to a very rewarding total return if one can consistently invest keeping quality and valuation in mind.

A decision can only be made with the information available at the moment. We don’t know how that will turn out, since there’s a forecast component involved. But applying these methodologies consistently across the whole portfolio will always yield a robust portfolio in the long run.

The primary determinant of high quality is superior financial strength. Financially strong companies possess the staying power and resources to weather the occasional bad storms that will inevitably occur. Every business will on occasion face challenges and difficulties. Meeting those challenges requires a strong balance sheet and an adaptive and competent management team to guide the company across troubled waters.

Regarding safety considerations, cash flows are more relevant than earnings. Because when it comes to the survival of a business, cash flow is king. As it relates to safety, a business surviving as an ongoing concern is the last line of defense. At this point, I’m not very confident in GE’s cash flow, given that dividends were reduced and estimates were lowered. In my opinion, they are in a fragile situation, and I’d consider them again once cash flow returns to more robust levels again:

For the portfolio that I’m tracking on this website, GE was sold for 41.2% loss, at $14.62. I had 40 shares, so It provided $584.8 of proceeds.

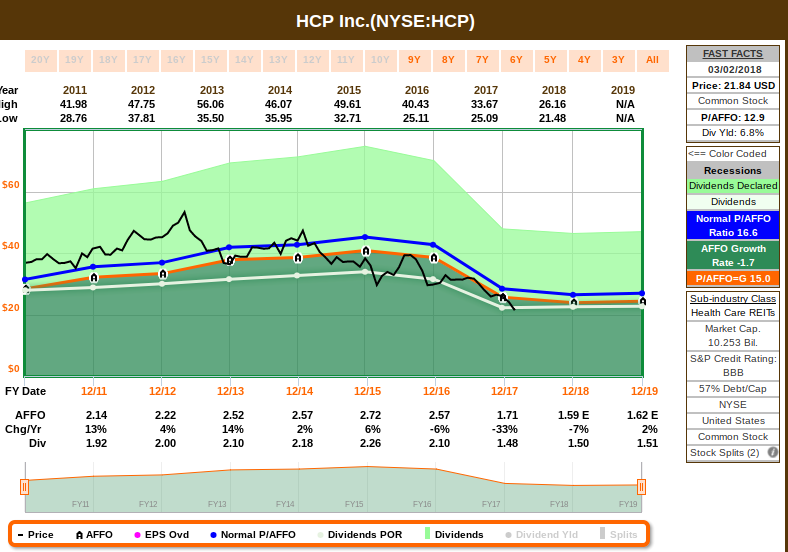

HCP: HCP management disappointed me on how Manorcare was handled, and I don’t have the confidence that they are prepared to handle similar challenges. Changes in the industry and laws such as Medicaid and Medicare programs forced HCP’s business model to change significantly, and now I will need a few year of steady earnings growth and management to prove that they could efficiently transform and implement their new business model before I partner with them again:

HCP wasn’t purchased for the portfolio that I’m tracking on this website.

.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.-.

Companies that I decided to partner with:

Besides deciding on the companies that no longer meet my goals, I also evaluate once a year which new companies I should partner with. Remember that this process solely speaks to what to buy, but it doesn’t determine when to buy (which needs to take valuation into account). Let’s go through the “what” now, and I’ll later elaborate some of the “when”. I decided to partner with the following business:

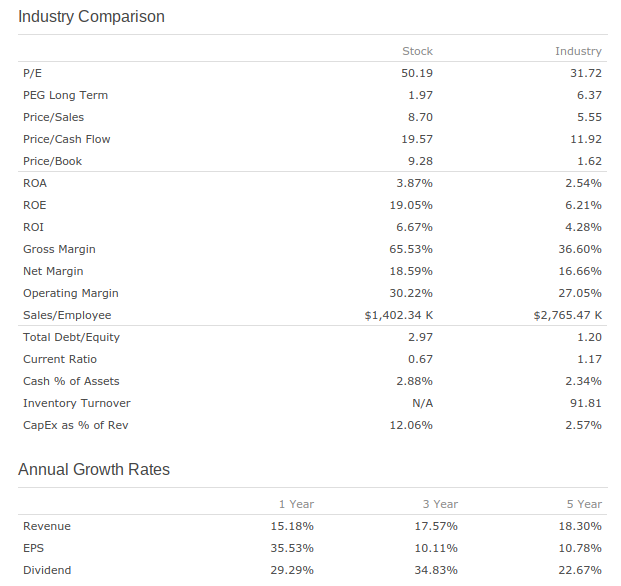

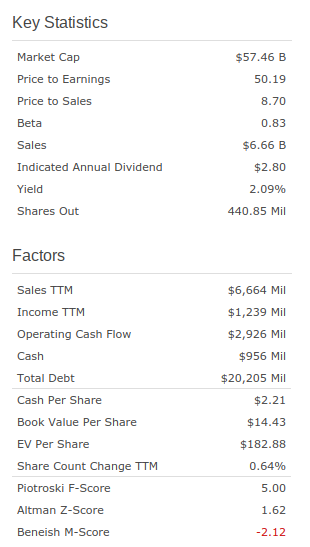

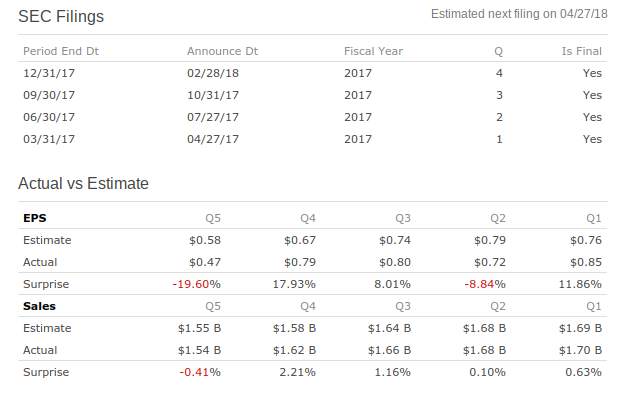

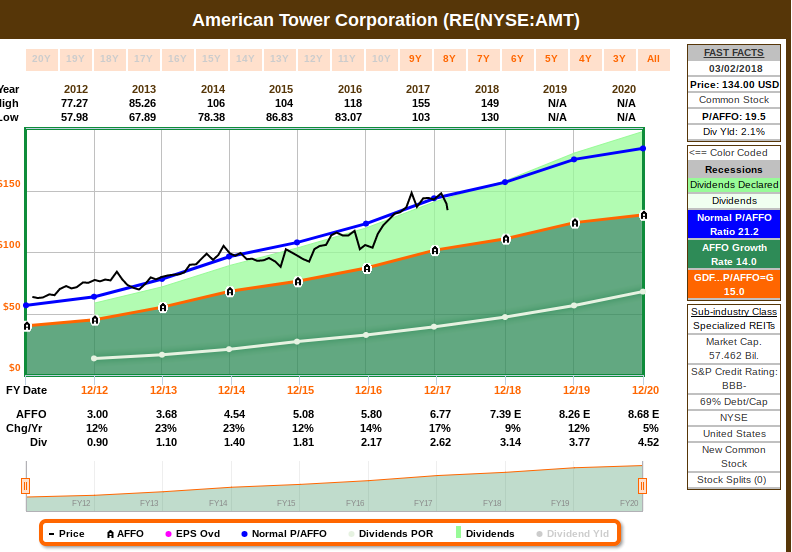

AMR: American Tower is one of the largest global REITs, is a leading independent owner, operator and developer of multitenant communications real estate with a portfolio of over 150,000 communications sites, and currently structured as a Real Estate Income Trust. Founded in 1995, American Tower includes approximately 40,000 towers in the United States and more than 109,000 towers internationally. AMR’s tower portfolio consists of their owned portfolio and those that they operate pursuant to long-term lease arrangements. Their portfolio also includes 800+ Distributed Antenna System (DAS) networks that AMR operates in malls, casinos, other in-building applications and select outdoor environments.

The companies that I bought this month:

The proceeds from selling the companies that no longer meet my goals ($584.8) plus reinvesting the dividends from 2017 ($706.48) plus using the typical amount dedicated for this portfolio ($2,000), it gives me a total of $3,291.28 to be invested this month.

I’ve decided to purchase the following companies using this cash – I chose 3 companies to start new positions, so I’ll be allocating $1,097.09 for each company.

On the next post I’ll elaborate the details of my automated screening process.

Happy Investing!