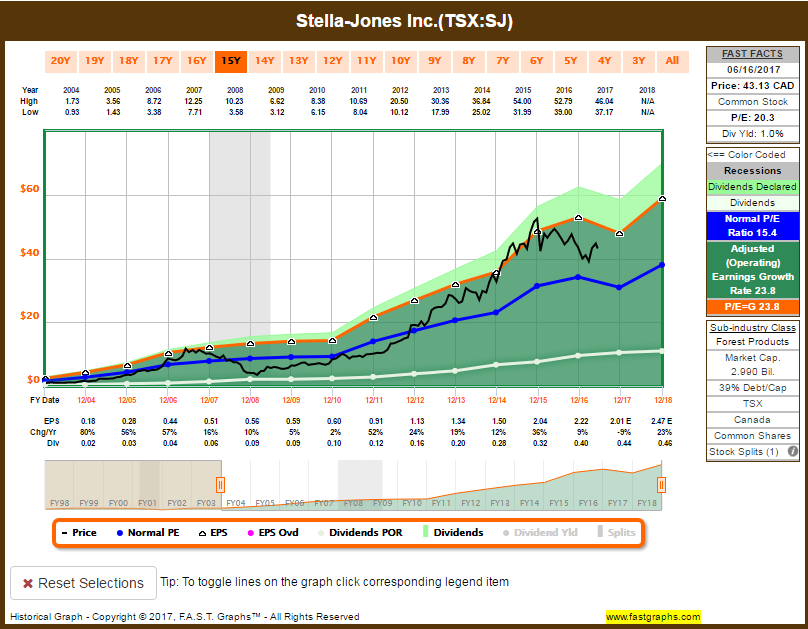

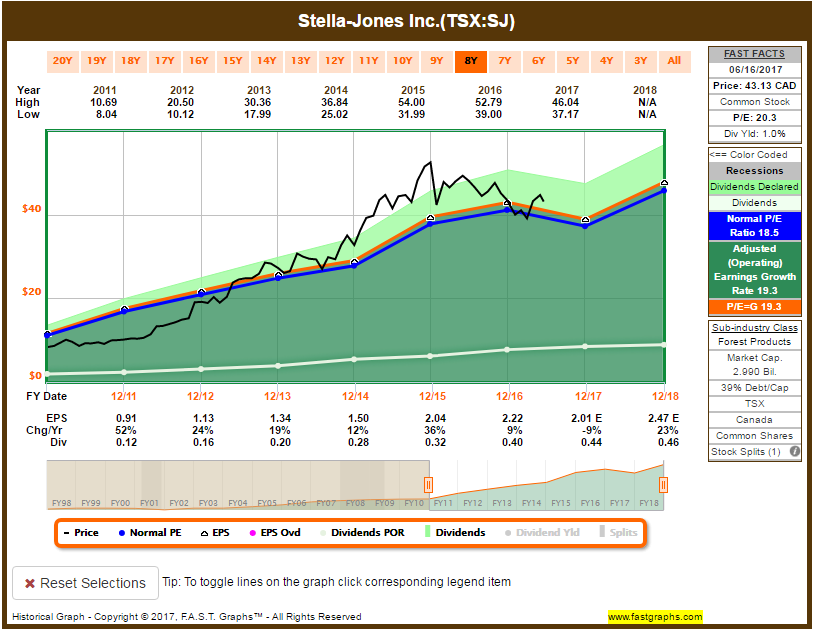

For this month, on the Canadian portfolio, I decided to add SJ as valuation gets more attractive. It’s still track to evaluate it, since has long periods of undervaluation and overvaluation.

Earnings have been at a higher rate lately, so I will use that as one of justification for the higher multiples. The other justification is the expectation of high growth for FY18. Although earnings are estimated to decline this year, the estimate for next year is promissing, and considering an earnings growth rate curve of 19%, current price is aligned with that, suggesting a fair valuation:

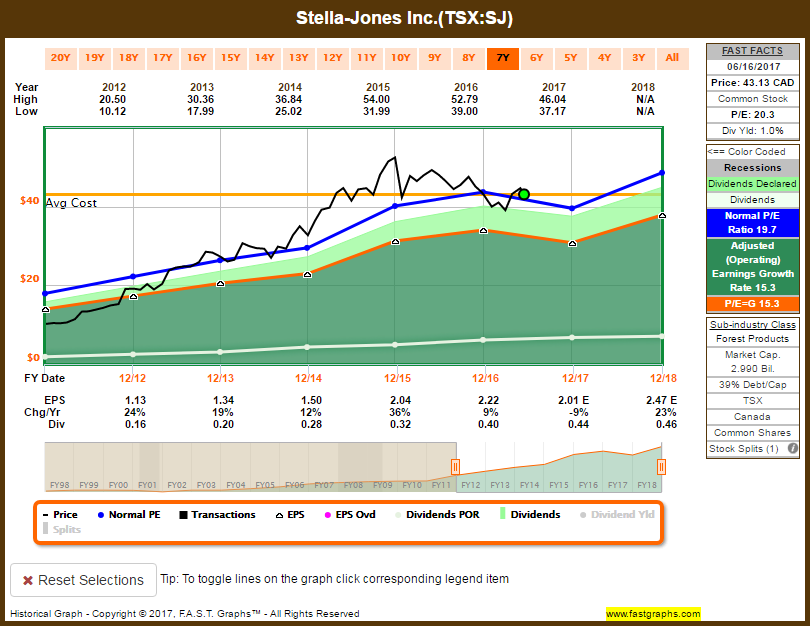

Considering an earnings growth rate graph of 15%, for increased margin of safety, the investment looks less attractive, suggesting that little total return would be achieved by then; however, dividends would continue to grow, and considering that as a worst-case scenario, I think the risk is justified to me; earnings would have to decline substantially to trade at those levels – a possibility, but not a high probability at this point:

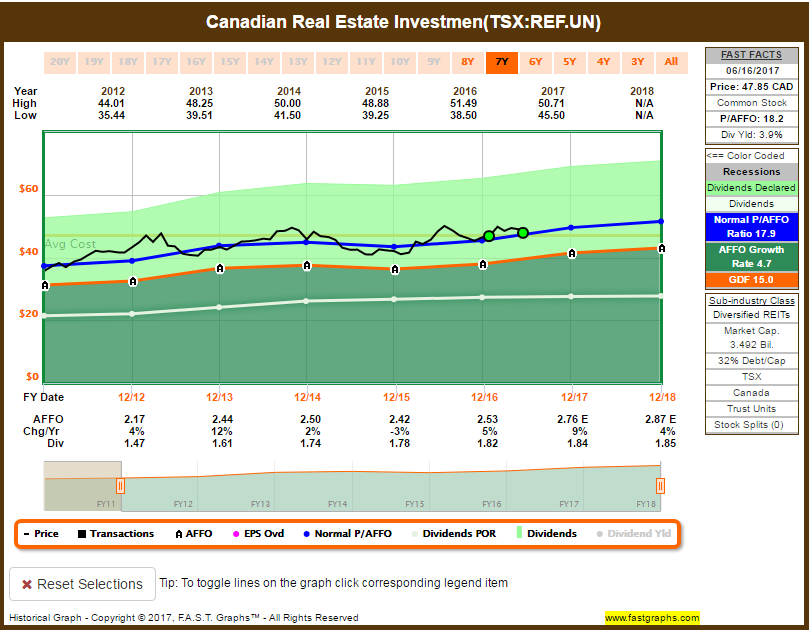

In order to diversify my exposure to REITs, I decided to add more to REF.UN, since valuation is attractive again considering their estimates for increasing AFFO:

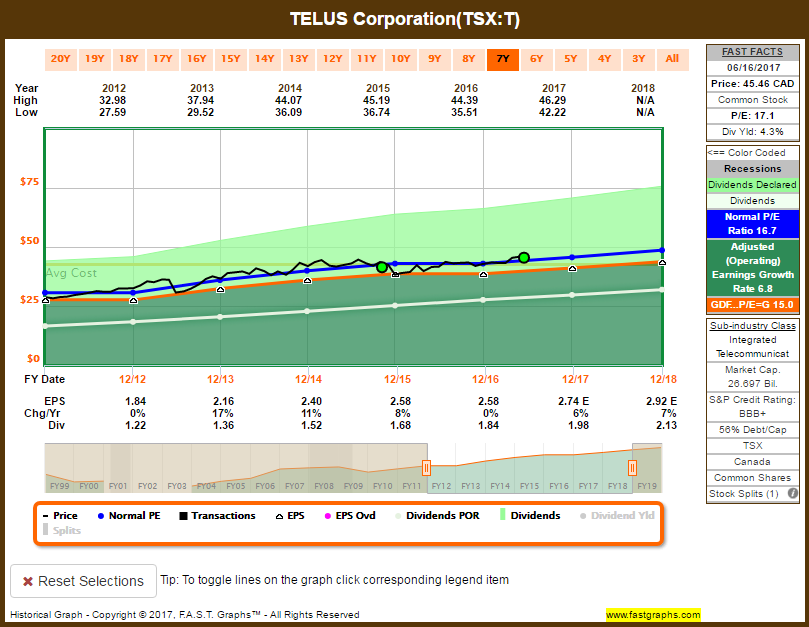

Also, to improve the sector weight distribution of this portfolio, I’ve added more T. Still waiting for Rogers valuation to come down.

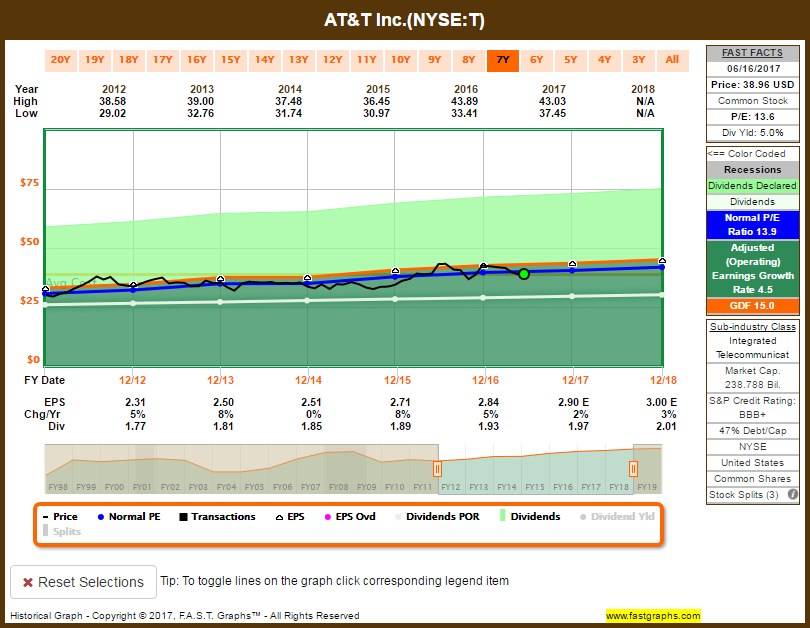

On the US portfolio, I’m diversifying my telecom exposure by adding T:

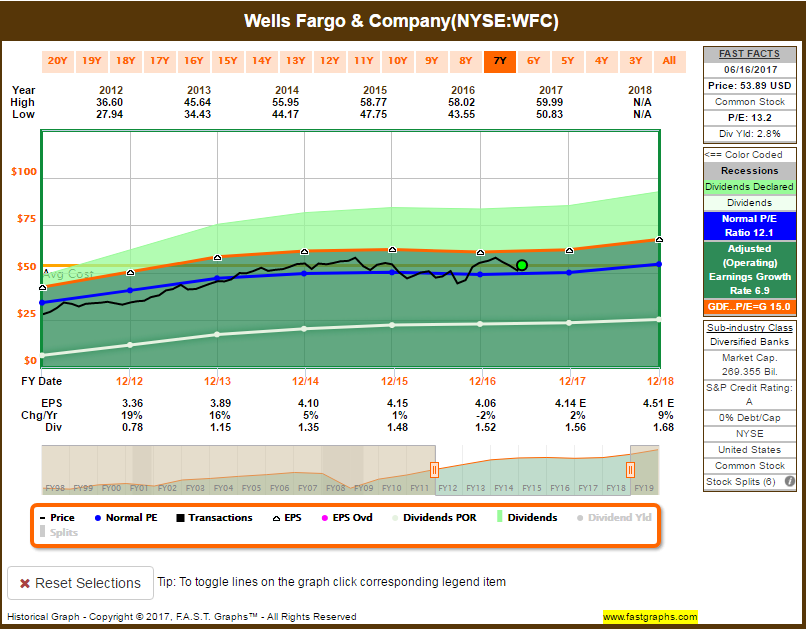

And also adding WFC, to continue improving the weight distribution per sector allocation: